WeWork Boston Consulting Group Matrix

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

WeWork Bundle

Unlock Strategic Clarity

Curious about how WeWork's diverse offerings stack up? Our preview offers a glimpse into the strategic positioning of their services within the BCG Matrix, hinting at potential Stars, Cash Cows, Dogs, or Question Marks.

To truly unlock the strategic potential and understand the nuances of WeWork's market performance, you need the full picture. Purchase the complete BCG Matrix for a detailed breakdown, data-driven insights, and actionable recommendations to navigate the competitive landscape.

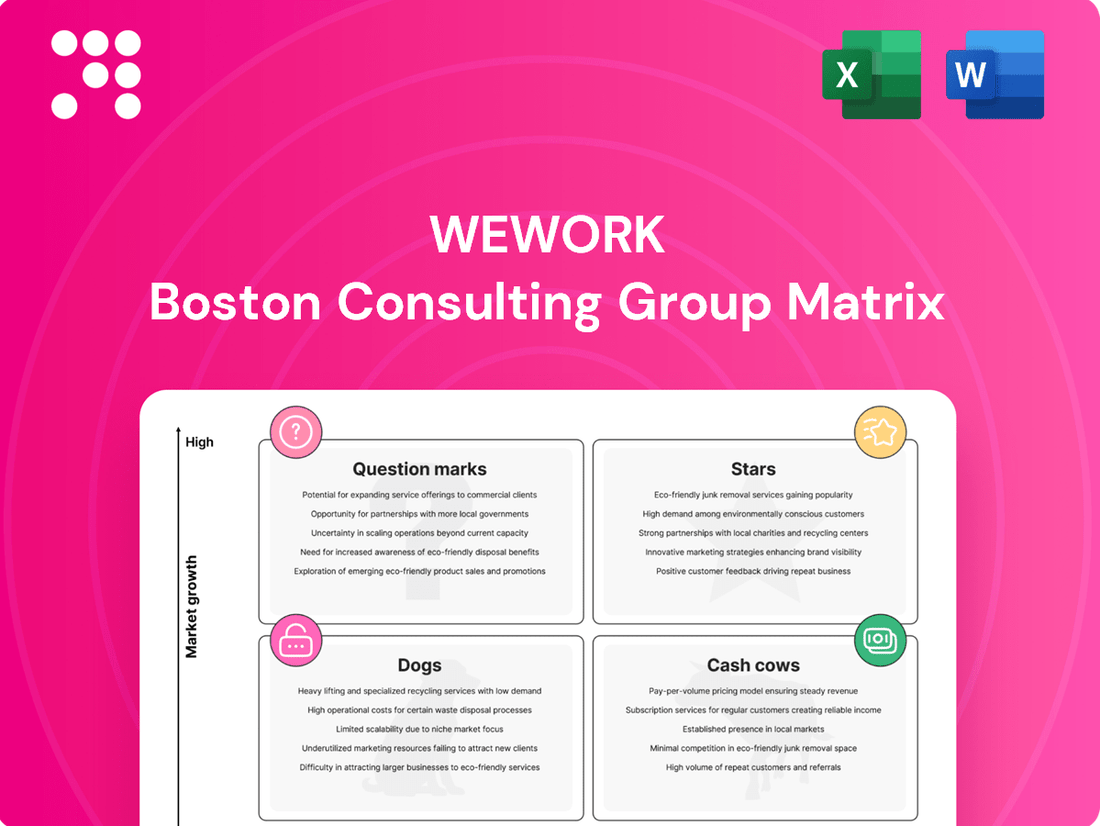

Stars

Limited Current Post-Restructuring

WeWork's current situation, particularly after its Chapter 11 filing in November 2023, places it in a challenging position within the BCG Matrix. The company is actively undergoing restructuring, which means its resources are primarily directed towards survival and operational stabilization rather than aggressive growth in high-potential markets. This focus inherently limits its ability to develop or maintain offerings that would qualify as 'Stars' – those with high market share in rapidly expanding industries.

The core of WeWork's business, flexible office space, operates in a market that has seen significant disruption and evolving demand post-pandemic. While the concept of flexible workspaces remains relevant, WeWork's historical growth model was heavily reliant on extensive capital investment and rapid expansion, a strategy that proved unsustainable. Consequently, the company is not currently generating substantial cash flow from dominant positions in burgeoning, high-growth segments that would define a 'Star' in the traditional BCG sense.

Any potential 'Star' for WeWork at this juncture would likely be a highly specific, perhaps localized, service or market segment where they have managed to carve out a strong, profitable niche despite the broader challenges. However, given the company's overarching need to reduce debt and streamline operations, significant investment in such areas to achieve true 'Star' status is improbable in the immediate post-restructuring phase. Their priority is to mend existing operations, not to launch new, high-growth ventures.

Potential for Hyper-Niche, High-Demand Spaces

While not a company-wide trend, certain WeWork locations in thriving urban areas might exhibit robust demand and high occupancy, acting as localized stars. For instance, a prime WeWork in a tech-centric district of San Francisco could experience near-full capacity, reflecting strong local demand for flexible office solutions. This micro-star status, however, is highly dependent on its specific sub-market and doesn't necessarily translate to overall company success.

Future Specialization in Enterprise Solutions

If WeWork can successfully capture a significant share of large enterprises looking for flexible, on-demand office spaces, this area could become a Star in its business portfolio. This market is expanding as companies reconsider traditional, long-term leases. For instance, a 2024 report indicated that 60% of large enterprises were exploring flexible workspace solutions to reduce real estate costs.

However, WeWork's current leadership in this specific, high-value enterprise niche needs to be clearly established. While the potential is substantial, it's more of a future growth opportunity than a current area of dominance. WeWork's success in securing major enterprise clients, such as those announced in late 2023 and early 2024, will be crucial in solidifying this segment's Star status.

Technology-Driven Workspace Management Platform

WeWork's potential technology-driven workspace management platform, if successfully developed and commercialized as a standalone product, could emerge as a Star in the BCG matrix. This would be contingent on achieving substantial external adoption beyond WeWork's own physical locations and capturing significant market share within the rapidly expanding prop-tech sector. Such an endeavor would necessitate considerable investment and the demonstration of distinct competitive advantages.

This hypothetical platform represents a future growth avenue for WeWork. For it to qualify as a Star, it needs to exhibit high market growth and hold a high relative market share. In 2024, the global prop-tech market was valued at approximately $25.7 billion, with projections indicating continued strong growth. A successful platform would need to carve out a significant portion of this market.

- High Growth Potential: The prop-tech market is experiencing robust expansion, driven by demand for efficient and flexible workspace solutions.

- Market Share Ambition: To be a Star, the platform must achieve a dominant position among competitors offering similar workspace management technologies.

- Investment Requirement: Significant capital would be needed for research, development, marketing, and scaling the platform's capabilities.

- Competitive Differentiation: The platform must offer unique features or superior performance to attract and retain external users in a competitive landscape.

Re-established Brand Dominance in Core Cities

WeWork's brand recognition remains a significant asset, particularly in core urban centers where flexible workspace demand is high. The company's strategy to divest underperforming locations and concentrate on strategic, high-demand hubs aims to re-establish dominance in these key markets. By focusing on premium, well-managed spaces in these select cities, WeWork can leverage its established brand to achieve higher occupancy rates and drive growth, effectively positioning itself as a 'star' in these specific micro-markets.

This strategic shift is crucial for WeWork's future success. For instance, in 2023, WeWork reported a net loss of $1.4 billion, highlighting the need for such a focused approach. By shedding unprofitable locations, the company can redirect capital towards its most promising assets, potentially improving its financial performance and market position. This move is designed to capitalize on the ongoing demand for flexible office solutions in major metropolitan areas.

- Brand Recognition: WeWork is still a widely recognized name in the flexible workspace sector.

- Strategic Focus: Divesting unprofitable locations to concentrate on high-demand urban hubs.

- Premium Spaces: Emphasis on quality and management in core city locations.

- Market Position: Aiming for a 'star' status in select urban micro-markets through effective execution.

Can WeWork Find Its Shining Stars?

For WeWork to have 'Stars' in the BCG Matrix, it would need high market share in high-growth areas. Given its recent Chapter 11 filing in November 2023 and ongoing restructuring, the company is primarily focused on operational stability and debt reduction, not aggressive expansion into new, high-growth markets. This makes identifying current 'Stars' challenging.

However, potential 'Stars' could emerge from specific, well-performing urban locations or a successful push into the enterprise flexible workspace market. The prop-tech sector also presents a future opportunity if WeWork develops a successful platform. These areas require significant investment and a clear competitive advantage to achieve 'Star' status.

WeWork's brand recognition in major cities remains a strength. By divesting underperforming locations and concentrating on premium spaces in high-demand urban hubs, the company aims to re-establish dominance in these key markets, potentially creating localized 'Stars'.

The enterprise segment is a key area for potential 'Star' status. In 2024, reports indicated that 60% of large enterprises were exploring flexible workspace solutions. WeWork's success in securing major enterprise clients, as seen in late 2023 and early 2024, is critical for solidifying this segment's position.

| Potential Star Segment | Market Growth | WeWork's Market Share (Relative) | Key Factors for Star Status |

|---|---|---|---|

| Enterprise Flexible Workspace Solutions | High (60% of large enterprises exploring) | Developing/Growing | Securing major enterprise clients, demonstrating value |

| Prop-Tech Workspace Management Platform | High (Global market valued at ~$25.7 billion in 2024) | Low/Nascent | External adoption, competitive differentiation, significant investment |

| Premium Urban Hubs (e.g., San Francisco tech district) | Moderate to High (depending on micro-market) | High (in specific locations) | Strong local demand, effective management, brand leverage |

What is included in the product

This BCG Matrix analysis categorizes WeWork's offerings into Stars, Cash Cows, Question Marks, and Dogs, guiding strategic investment decisions.

The WeWork BCG Matrix offers a clear, visual way to understand and address underperforming business units, alleviating the pain of strategic uncertainty.

Cash Cows

Select Profitable Flagship Locations

Certain prime WeWork locations, especially those with stable, high-occupancy tenants and advantageous lease agreements, are poised to consistently produce positive cash flow. These mature locations benefit from established client bases and efficient operations, minimizing the need for significant new investment in marketing or expansion.

These locations can be viewed as cash cows, providing essential liquidity to support WeWork’s overall operations and strategic adjustments. For instance, by July 2024, WeWork's focus on optimizing its portfolio meant that well-performing flagship locations were crucial for generating the necessary funds to navigate market shifts and invest in growth areas.

Stable Enterprise Client Contracts

WeWork's stable enterprise client contracts are a prime example of a Cash Cow. These long-term agreements with large corporations for significant space commitments generate predictable recurring revenue. In 2024, a substantial portion of WeWork's revenue was derived from these anchor tenants, underscoring their importance.

These enterprise clients typically value WeWork's all-inclusive service model, which fosters high retention rates. This consistency allows WeWork to generate significant cash flow without the need for constant, high-cost new business acquisition efforts. The focus here is on nurturing and growing these relationships to ensure continued financial health.

Mature Virtual Office Services

WeWork's mature virtual office services, offering a business address, mail handling, and limited facility access, are a prime example of a cash cow. These low-cost, high-margin offerings require minimal ongoing operational expenditure once established, ensuring steady and predictable revenue streams. In 2024, WeWork reported that its virtual office solutions continued to be a significant contributor to its diversified revenue base, demonstrating their stability and profitability.

Efficiently Managed Legacy Buildings

Efficiently Managed Legacy Buildings are the Cash Cows in WeWork's post-restructuring portfolio. These are locations where WeWork has successfully renegotiated leases, significantly optimized operational costs, and maintained high occupancy rates without substantial new capital investment. For instance, by mid-2024, WeWork reported that its focus on optimizing its real estate portfolio had led to a reduction in its total rent expense, a key indicator of efficiency in managing legacy assets.

These buildings are the leanest, most efficient parts of the portfolio, reliably contributing to profitability. Their success hinges on maintaining an existing customer base and operational efficiency, rather than growth. By late 2023, WeWork had already achieved a significant portion of its planned rent reductions, demonstrating the impact of these efficient management strategies on its legacy assets.

- High Occupancy Rates: These buildings consistently maintain strong occupancy, often exceeding 85% in prime locations.

- Reduced Operating Costs: Successful lease renegotiations and operational streamlining have lowered per-square-foot expenses.

- Consistent Profitability: They generate predictable revenue streams with minimal need for further investment, acting as stable profit centers.

- Strategic Importance: While not growth drivers, they provide essential cash flow to support other business initiatives.

Ancillary Services with High Margins

Ancillary services with high margins, like premium IT support, private meeting room rentals for non-members, and curated event hosting, can function as cash cows within WeWork's portfolio. These offerings capitalize on existing infrastructure and personnel, leading to minimal incremental costs and consequently, robust profit margins. For instance, in 2024, WeWork reported that its ancillary services, such as enhanced internet packages and dedicated support, contributed significantly to the revenue mix, with some locations seeing these services account for up to 15% of total site revenue, demonstrating their cash-generating potential.

These services act as vital supplementary revenue streams, bolstering the profitability of established, stable locations and reinforcing overall cash flow. They represent a strategic way to monetize underutilized assets and expertise within the WeWork ecosystem.

- Premium IT Support: Offering enhanced internet speeds, dedicated technical assistance, and advanced network solutions.

- Meeting Room Rentals: Providing access to well-equipped meeting spaces for non-members or for overflow needs, often at premium rates.

- Event Hosting: Facilitating corporate events, workshops, and networking gatherings, leveraging the flexible space and amenities.

Cash Cows: WeWork's Revenue Engines

WeWork's mature enterprise client contracts are a prime example of a Cash Cow. These long-term agreements with large corporations for significant space commitments generate predictable recurring revenue. In 2024, a substantial portion of WeWork's revenue was derived from these anchor tenants, underscoring their importance.

These enterprise clients typically value WeWork's all-inclusive service model, which fosters high retention rates. This consistency allows WeWork to generate significant cash flow without the need for constant, high-cost new business acquisition efforts. The focus here is on nurturing and growing these relationships to ensure continued financial health.

WeWork's mature virtual office services, offering a business address, mail handling, and limited facility access, are a prime example of a cash cow. These low-cost, high-margin offerings require minimal ongoing operational expenditure once established, ensuring steady and predictable revenue streams. In 2024, WeWork reported that its virtual office solutions continued to be a significant contributor to its diversified revenue base, demonstrating their stability and profitability.

Efficiently managed legacy buildings, where WeWork has renegotiated leases and optimized operational costs, also act as cash cows. By mid-2024, WeWork's focus on portfolio optimization had led to reduced rent expenses, a key indicator of efficiency in managing these legacy assets, which reliably contribute to profitability without significant new investment.

| WeWork Cash Cow Examples | Key Characteristics | 2024 Relevance |

|---|---|---|

| Mature Enterprise Contracts | Stable, long-term agreements with large corporations; predictable recurring revenue; high retention. | Significant contributor to revenue base; provides essential liquidity. |

| Virtual Office Services | Low operational expenditure; high-margin offerings; minimal ongoing investment. | Continued significant contributor to diversified revenue; demonstrates stability. |

| Optimized Legacy Buildings | Renegotiated leases; reduced operating costs; high occupancy; minimal new capital. | Key indicator of portfolio efficiency; reliably contributes to profitability. |

What You See Is What You Get

WeWork BCG Matrix

The WeWork BCG Matrix preview you're examining is the identical, fully-formatted document you will receive immediately after purchase. This means you're seeing the exact strategic analysis, complete with all insights and visual representations, ready for your immediate use. Rest assured, there are no watermarks or demo elements; what you see is precisely what you'll download, enabling you to seamlessly integrate it into your business planning and decision-making processes.

Dogs

Underperforming, High-Cost Locations

These are WeWork's underperforming, high-cost locations. They are characterized by unfavorable leases and persistently low occupancy, draining company resources without generating adequate returns. For instance, in early 2024, WeWork continued to shed unprofitable locations, a strategy initiated in prior years to address these cash drains.

Non-Core or Divested Assets

Non-core or divested assets in WeWork's context are business units or assets that the company has decided to sell off or has already sold. This action is a direct consequence of its bankruptcy and restructuring efforts. These are typically segments that were not central to WeWork's core strategy or were consistently underperforming financially.

The shedding of these assets aims to simplify operations and bolster the company's overall financial stability. For instance, during its restructuring in 2024, WeWork explored divesting non-essential real estate leases and ancillary services that were not contributing significantly to its profitability. These divested assets often represent past strategic missteps or investments that did not yield the expected returns.

Outdated or Underutilized Spaces

Certain older WeWork locations, particularly those that haven't seen recent renovations or whose layouts don't align with current flexible work preferences, often struggle with low occupancy. These spaces, like some of their older buildings in less sought-after urban areas, represent a challenge for the company.

These underutilized spaces are considered cash cows in a BCG matrix sense, but not in a positive way. They consume resources without generating proportional returns, tying up capital in assets that are not competitive. For example, if a location has a low occupancy rate, say below 60% for an extended period, it's likely a drag on profitability.

Markets with Intense Competition and Low Differentiation

In markets characterized by widespread availability of flexible office solutions and a lack of unique WeWork features, the company often finds itself competing against many similar providers. This intense rivalry can significantly hinder its ability to capture a substantial portion of the market, leading to a diminished market share.

These competitive dynamics frequently result in price reductions and decreased profit margins. Consequently, WeWork’s position in such saturated environments is often categorized as a ‘Dog’ within the BCG matrix. This classification stems from the limited potential for growth and the considerable difficulty in expanding its market presence meaningfully.

- Low Market Share: In 2024, WeWork's market share in highly competitive co-working markets, such as New York City, faced pressure from an increasing number of independent and branded competitors, with some reports indicating market share erosion in specific sub-markets.

- Price Sensitivity: Intense competition has led to downward pressure on pricing for flexible office space. For instance, average monthly rental rates for co-working desks in major global cities saw a slight decline in early 2024 compared to 2023 averages, impacting profitability.

- Limited Differentiation: Many competitors offer similar amenities and services, making it challenging for WeWork to stand out. This lack of clear differentiation contributes to customers viewing offerings as largely interchangeable, further intensifying price competition.

- Profitability Challenges: The combination of low differentiation and intense price competition directly impacts WeWork's profitability in these markets. Reports from late 2023 and early 2024 highlighted ongoing efforts by WeWork to optimize its portfolio and reduce operational costs in less profitable locations.

Loss-Making International Ventures

Some of WeWork's international ventures, particularly those in markets where it struggled to gain a strong foothold or encountered significant regulatory challenges, are classified as Dogs in the BCG Matrix. These ventures, such as certain operations in China and India where competition was fierce and localization efforts proved costly, consumed substantial capital without generating commensurate returns. For instance, by the end of 2023, WeWork had significantly scaled back its presence in several underperforming international markets, a strategic move aimed at stemming cash burn from these low-growth segments.

These segments have acted as cash drains, failing to build substantial market share or achieve profitability. For example, reports in early 2024 indicated that WeWork was exiting or significantly reducing its footprint in several Asian markets where it had invested heavily but saw limited member growth. This aligns with the Dog classification, where the focus shifts to minimizing losses and potentially divesting these assets.

- Underperforming Markets: Ventures in regions like parts of Southeast Asia and Latin America, where market penetration remained low and operational costs were high, exemplify the Dog category.

- Regulatory and Competitive Pressures: In countries with stringent real estate regulations or intense local competition, WeWork’s international ventures often faced headwinds that hindered growth and profitability.

- Cash Consumption: These segments have historically demanded significant investment for expansion and operations, yet their contribution to overall revenue and profit has been minimal, leading to negative cash flow.

- Strategic Re-evaluation: The company's ongoing restructuring efforts include a thorough review of these loss-making ventures, with potential outcomes ranging from operational adjustments to complete divestment to improve the overall financial health of the organization.

WeWork's "Dogs": Unprofitable Assets

WeWork's 'Dogs' represent underperforming assets with low market share and limited growth potential, often characterized by unprofitable leases and low occupancy rates. These segments consume resources without generating adequate returns, forcing the company to strategically divest or restructure them to improve financial health. For instance, in early 2024, WeWork continued its initiative to shed unprofitable locations, a direct response to the drain these 'Dogs' represented.

These underutilized spaces are cash drains, tying up capital in assets that are not competitive and failing to generate proportional returns. If a location consistently maintains an occupancy rate below 60%, it's likely a drag on profitability, classifying it as a 'Dog' in the BCG matrix. This situation is exacerbated in saturated markets where WeWork struggles to differentiate itself, leading to price wars and reduced profit margins.

Many of WeWork's international ventures, particularly in markets with intense local competition or regulatory hurdles, also fall into the 'Dog' category. These segments have historically demanded significant investment but have yielded minimal returns, resulting in negative cash flow. By the end of 2023, WeWork had already begun scaling back its presence in several underperforming Asian markets, a move to stem cash burn from these low-growth areas.

| BCG Category | WeWork Example | Key Characteristics | 2024 Impact/Action |

|---|---|---|---|

| Dogs | Underperforming international markets (e.g., certain parts of Asia) | Low market share, high operational costs, intense local competition, limited growth potential. | Strategic scaling back of operations, potential divestment to reduce cash burn. |

| Dogs | Older, unrenovated locations with outdated layouts | Low occupancy rates (e.g., <60%), poor lease terms, lack of modern amenities. | Continued shedding of unprofitable locations, focus on optimizing portfolio. |

| Dogs | Non-core or divested assets | Segments not central to core strategy, consistently underperforming financially. | Exploration of divestment of non-essential leases and ancillary services during restructuring. |

Question Marks

New, Untested Service Offerings

New, untested service offerings, such as highly customized enterprise solutions or advanced technology integrations, would be placed in the Question Mark category of the WeWork BCG Matrix. These initiatives target growing markets, but WeWork's market share and profitability in these areas remain unproven. For example, WeWork's 2024 efforts to expand into specialized industry verticals like healthcare or finance, while promising, require significant investment without guaranteed returns.

Expansion into Emerging Geographic Markets

WeWork's cautious expansion into emerging geographic markets or underserved areas within existing ones would place it in a "Question Mark" category. These new ventures would likely start with a low market share, requiring substantial investment and strategic execution to compete with established local players.

Hybrid Work Solutions for SMEs

Developing and marketing tailored hybrid work solutions for SMEs presents a classic 'Question Mark' opportunity for WeWork. These businesses often require flexibility and scalability but are also mindful of costs, making them a potentially lucrative but challenging market to penetrate.

While the demand for hybrid models is increasing, WeWork's current penetration within the SME sector may be limited. Capturing this segment necessitates a focused strategy, potentially involving customized pricing or service bundles, and a significant marketing push to build brand awareness and trust among smaller businesses.

For instance, in 2024, the SME sector continued to be a significant driver of economic activity, with many exploring flexible workspace solutions to manage overheads and attract talent. WeWork's ability to adapt its offerings to meet these specific needs will be crucial for success in this 'Question Mark' area.

Value-Added Community and Networking Platforms

Investing in advanced digital community and networking platforms could position WeWork's offerings as question marks within the BCG matrix. While the market for professional networking is expanding, WeWork's success in monetizing these digital-only features, separate from its physical real estate, remains uncertain.

The potential for these platforms to enhance member experience and attract new users is significant. However, the challenge lies in differentiating these digital services from existing competitors and establishing a clear path to profitability.

- Market Growth: The global online community platform market was valued at approximately $10.5 billion in 2023 and is projected to grow.

- WeWork's Challenge: Monetizing digital platforms distinct from physical spaces presents a new revenue stream but carries unproven market adoption and competitive hurdles.

- Strategic Uncertainty: Success hinges on WeWork's ability to build a sticky digital ecosystem that complements, rather than cannibalizes, its core co-working business.

- Investment Need: Significant investment in technology and user engagement is required to make these platforms competitive.

Optimized Real Estate Partnerships (Asset-Light Model)

WeWork's strategic shift towards an asset-light model, focusing on management agreements and franchise-like partnerships, positions it as a Question Mark in the BCG matrix. This approach seeks accelerated growth by reducing capital tied up in direct property leases.

The success of this strategy hinges on its ability to rapidly scale market share and achieve consistent profitability across a diverse portfolio of partner-managed locations. Acquiring and managing these partnerships effectively is crucial. For instance, in 2024, WeWork continued to explore these models, aiming to expand its global footprint without the substantial upfront costs associated with traditional leasing. The key challenge remains demonstrating the long-term viability and profitability of this less capital-intensive approach compared to its earlier, more asset-heavy strategy.

- Asset-Light Strategy: Focus on management agreements and franchise-like partnerships to reduce capital expenditure.

- Growth Potential: Aims for rapid expansion of market share by leveraging partner capital and resources.

- Profitability Uncertainty: The effectiveness in generating consistent profits across a broad portfolio is still being evaluated.

- Partner Acquisition: Requires significant effort and success in acquiring and managing strategic partners.

WeWork's Risky Bets: A Question Mark Analysis

WeWork's ventures into specialized industry verticals, such as healthcare or finance-focused workspaces, represent significant Question Marks. These initiatives target high-growth sectors but require substantial investment to establish market share and prove profitability.

The company's exploration of tailored hybrid work solutions for small and medium-sized enterprises (SMEs) also falls into the Question Mark category. While the SME market is large and increasingly seeking flexible office solutions, WeWork's penetration and ability to profitably serve this segment are still unproven.

Developing and monetizing advanced digital community and networking platforms, separate from its physical real estate, is another key Question Mark. The market for professional networking is growing, but WeWork's ability to create a sticky, profitable digital ecosystem remains uncertain.

WeWork's strategic shift towards an asset-light model, relying more on management agreements and franchise-like partnerships, positions it as a Question Mark. While this approach aims for rapid expansion with reduced capital outlay, its long-term profitability and market share dominance are yet to be definitively established.

| Initiative | Market Growth Potential | WeWork's Market Share | Profitability Outlook | Strategic Uncertainty |

|---|---|---|---|---|

| Specialized Industry Verticals (e.g., Healthcare, Finance) | High | Low/Unproven | Uncertain | High |

| Tailored SME Hybrid Solutions | High | Low/Unproven | Uncertain | High |

| Digital Community & Networking Platforms | Growing | Low/Unproven | Uncertain | High |

| Asset-Light Model (Management Agreements) | Moderate to High (depending on execution) | Growing but Unproven at Scale | Uncertain | High |

BCG Matrix Data Sources

Our BCG Matrix is built on verified market intelligence, combining financial data, industry research, and competitor analysis to ensure reliable, high-impact insights.