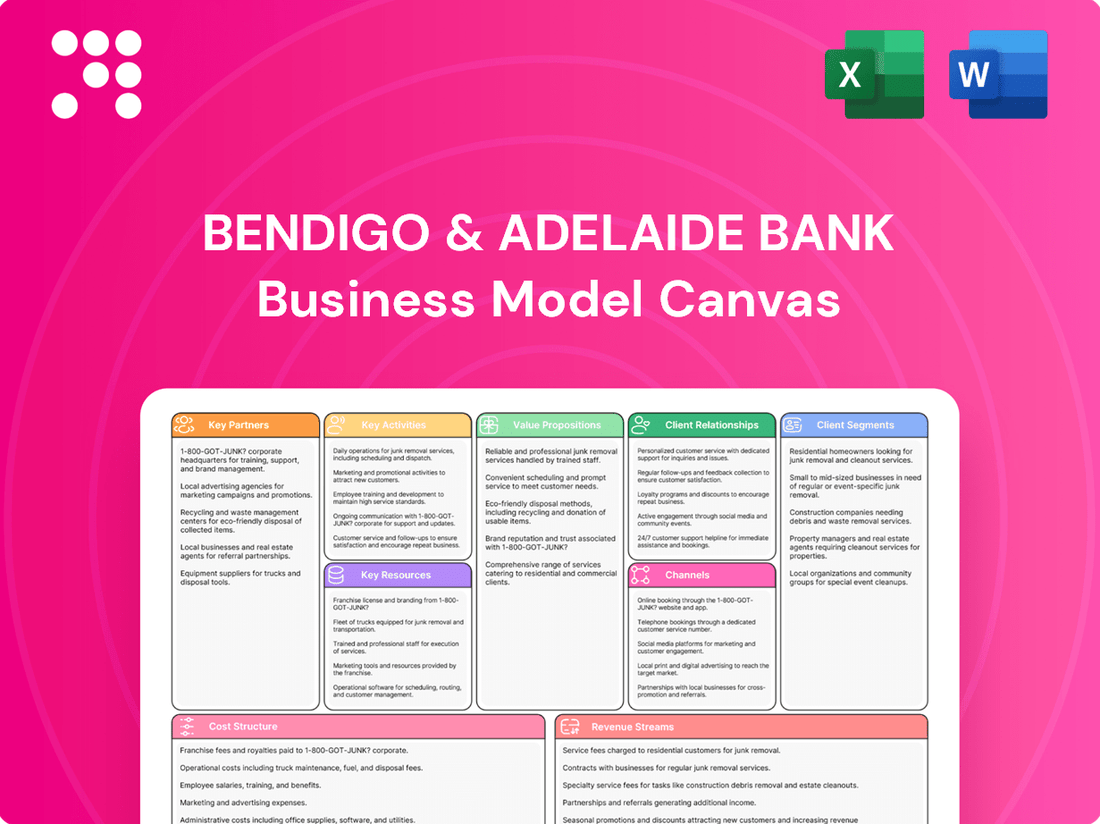

Bendigo & Adelaide Bank Business Model Canvas

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Bendigo & Adelaide Bank Bundle

Bank's Blueprint: Unveiling Strategic Core

Discover the strategic core of Bendigo & Adelaide Bank's success with our comprehensive Business Model Canvas. This detailed breakdown illuminates their customer relationships, revenue streams, and key resources, offering invaluable insights for anyone looking to understand their competitive edge. Download the full canvas to unlock a powerful strategic blueprint.

Partnerships

Community Bank Network

Bendigo and Adelaide Bank's Community Bank network is a cornerstone of its business model, built on partnerships with local communities across Australia. These aren't just branches; they are locally owned and operated entities. This unique structure means a substantial portion of profits generated by these Community Banks is channeled back into local projects and initiatives, fostering a direct link between banking and community development.

As of the 2024 financial year, Bendigo and Adelaide Bank reported that its Community Bank network continued to be a significant driver of its success, with over 300 Community Bank branches operating. This network has collectively contributed over $300 million to local communities since its inception, demonstrating the tangible impact of this partnership approach on local prosperity and development.

Fintech Companies and Technology Providers

Bendigo and Adelaide Bank actively forges partnerships with fintech firms and technology providers to bolster its digital offerings and operational efficiency. These collaborations are crucial for staying competitive in the rapidly evolving financial landscape.

Key alliances include working with Salesforce for customer relationship management and nCino for loan origination processes. These partnerships allow for more streamlined customer interactions and faster application processing, enhancing the overall customer experience.

Furthermore, the bank leverages cloud services from major providers like Amazon Web Services (AWS) and Google Cloud. This strategic move supports infrastructure modernization, offering scalability and improved data management capabilities, which are vital for a modern banking operation.

Mortgage Brokers and Aggregators

Bendigo and Adelaide Bank heavily relies on mortgage brokers and aggregators to distribute its lending products, particularly home loans. This partnership significantly expands the bank's market reach, allowing it to connect with a broader customer base that prefers using intermediary services for their borrowing needs.

In 2024, mortgage brokers were instrumental in settling a substantial volume of home loans for Bendigo and Adelaide Bank. For instance, the bank reported that approximately 60% of its new residential mortgage volume in the first half of 2024 was originated through its broker channels, highlighting the critical role these partnerships play in its lending strategy.

By collaborating with broker networks and aggregators, the bank streamlines the mortgage settlement process. These third-party channels not only facilitate loan origination but also manage a significant portion of the administrative and compliance aspects, enabling Bendigo and Adelaide Bank to efficiently scale its mortgage business.

Strategic Alliances and White Label Partners

Bendigo and Adelaide Bank leverages strategic alliances and white-label partnerships to expand its product and service offerings, often operating under distinct brands or through specialized distribution channels. This approach is crucial for diversifying market reach and tapping into previously inaccessible customer segments.

These collaborations enable the bank to offer specialized financial solutions, such as digital banking platforms or niche lending products, without the need for extensive in-house development. For instance, in 2024, the bank continued to explore partnerships that enhance its digital capabilities and customer experience.

- Partnerships for Digital Expansion: Collaborations with fintech firms in 2024 aimed to integrate advanced digital tools, improving customer onboarding and transaction processing.

- White Labeling for Niche Markets: The bank may engage in white-label agreements to provide banking services to non-financial companies, reaching new demographics.

- Access to New Customer Segments: By partnering with businesses that have established customer bases, Bendigo and Adelaide Bank can gain access to segments like small businesses or specific demographic groups more efficiently.

Government and Regulatory Bodies

Bendigo and Adelaide Bank actively partners with government and regulatory bodies, including the Australian Prudential Regulation Authority (APRA), to navigate the complex Australian financial services landscape. This collaboration is fundamental to ensuring adherence to all banking regulations, a cornerstone of maintaining public trust and operational integrity.

These partnerships are vital for the bank's commitment to financial inclusion. By working with government entities, Bendigo and Adelaide Bank can better implement strategies that broaden access to financial services across diverse communities, aligning with national economic objectives.

For instance, in 2024, APRA continued to emphasize robust capital requirements and risk management frameworks for Australian banks. Bendigo and Adelaide Bank's engagement with APRA ensures its practices meet these evolving standards, safeguarding its financial stability and customer deposits.

- Regulatory Compliance: Adherence to APRA's prudential standards, including capital adequacy ratios and liquidity management, is paramount.

- Financial Inclusion Initiatives: Collaboration on programs aimed at improving access to banking services for underserved populations.

- Industry Standards: Contributing to the development and maintenance of sound financial sector practices in Australia.

- Trust and Reputation: Maintaining a strong relationship with regulators bolsters the bank's credibility and reputation among stakeholders.

Strategic Partnerships Drive Bank's Growth and Digital Evolution

Bendigo and Adelaide Bank's Key Partnerships are multifaceted, ranging from local community entities to global technology providers and essential intermediaries like mortgage brokers. These collaborations are fundamental to its operational strategy and market reach.

The bank's reliance on mortgage brokers is substantial, with around 60% of new residential mortgage volume in the first half of 2024 originating through these channels, underscoring their critical role in expanding lending. Furthermore, strategic alliances with fintech firms and cloud service providers like AWS and Google Cloud are vital for enhancing digital capabilities and operational efficiency.

These partnerships are not just about distribution; they are about innovation and market penetration. By working with a diverse set of partners, Bendigo and Adelaide Bank can effectively serve a broad customer base and adapt to the evolving financial landscape.

| Partnership Type | Key Partners | Strategic Importance | 2024 Impact/Data Point |

|---|---|---|---|

| Community Banks | Local Communities | Market penetration, brand loyalty, community development | Over 300 branches, $300M+ contributed to communities |

| Financial Technology (Fintech) | Salesforce, nCino | Digital offerings, operational efficiency, customer experience | Streamlined customer interactions, faster application processing |

| Mortgage Brokers & Aggregators | Various Broker Networks | Lending product distribution, market reach | ~60% of new residential mortgage volume (H1 2024) |

| Cloud Services | AWS, Google Cloud | Infrastructure modernization, scalability, data management | Supports infrastructure modernization and improved data management |

| Government & Regulatory Bodies | APRA | Regulatory compliance, financial inclusion, trust | Ensures adherence to prudential standards and risk management |

What is included in the product

A comprehensive overview of Bendigo and Adelaide Bank's business model, detailing its customer segments, value propositions, and revenue streams within the 9 classic BMC blocks.

This model reflects the bank's community-focused approach and digital transformation, providing insights for strategic decision-making and stakeholder communication.

Bendigo & Adelaide Bank's Business Model Canvas acts as a pain point reliever by providing a clear, visual representation of their customer segments and value propositions, allowing for swift identification of underserved markets and opportunities to tailor financial products and services.

This structured approach streamlines the process of understanding customer needs and designing solutions, effectively alleviating the pain of inefficient product development and market misalignment.

Activities

Retail and Business Banking Operations

Retail and business banking operations are the heart of Bendigo and Adelaide Bank, encompassing the daily management of customer accounts, transaction processing, and the provision of essential banking services. This includes everything from savings and checking accounts to loans and mortgages for individuals and businesses alike, forming the bedrock of their customer relationships.

In the financial year 2024, Bendigo and Adelaide Bank reported a net interest margin of 1.72%, reflecting the efficiency of these core operations in generating revenue. The bank's commitment to these activities is evident in its substantial customer base, serving millions of Australians across its retail and business segments.

Lending and Credit Origination

A core activity for Bendigo and Adelaide Bank is originating and managing various lending products. This includes everything from home loans for individuals to personal loans and crucial business loans for companies.

This process involves rigorous credit assessment to evaluate borrower risk, followed by the loan approval stage. Once loans are disbursed, the bank actively manages them, ensuring timely repayments and addressing any potential issues.

In the financial year 2024, Bendigo and Adelaide Bank reported a total lending portfolio of $72.4 billion, highlighting the significant scale of their credit origination activities.

Wealth Management Services

Bendigo and Adelaide Bank provides comprehensive wealth management services, encompassing financial planning, a diverse range of investment products, and superannuation solutions. These offerings are designed to assist customers in effectively growing and managing their financial assets throughout their lives.

In 2024, the Australian superannuation sector alone managed over $3.5 trillion in assets, highlighting the significant demand for such services. Bendigo and Adelaide Bank's engagement in this space positions them to capture a share of this substantial market by offering tailored advice and investment opportunities to individuals and families aiming for long-term financial security and wealth accumulation.

Digital Transformation and Technology Modernisation

Bendigo and Adelaide Bank's commitment to digital transformation is a cornerstone of its strategy, involving a multi-year program to modernize its core banking systems. This initiative aims to streamline operations, improve efficiency, and elevate the customer experience through enhanced digital platforms.

A key component of this transformation is the migration to cloud infrastructure, which offers greater scalability and flexibility. The bank is also heavily focused on process automation to reduce manual effort and speed up service delivery. For instance, in the first half of the 2024 financial year, the bank reported a 12% increase in digital transaction volumes, highlighting the growing adoption of its digital channels.

- Core Banking Modernisation: Ongoing efforts to simplify and update legacy systems.

- Cloud Migration: Transitioning infrastructure to cloud-based solutions for improved agility.

- Process Automation: Implementing technology to streamline internal operations and customer interactions.

- Digital Platform Development: Investing in and expanding offerings like the Up digital banking app, which saw its customer base grow by 25% in 2023.

Community Engagement and Development

Bendigo and Adelaide Bank's Community Engagement and Development is central to its business model. Through its unique Community Bank branches, the bank actively reinvests profits back into the local areas they serve, fostering economic growth and social well-being. This commitment goes beyond traditional banking, directly contributing to the vitality of these communities.

This engagement manifests in tangible ways, such as providing scholarships to local students and supporting a wide array of community projects. For instance, in the 2023 financial year, Bendigo and Adelaide Bank reported a statutory profit after tax of $990 million. A significant portion of this success is channeled back into community initiatives, underscoring their purpose-driven approach.

- Reinvestment of Profits: A core activity involves returning a portion of profits to the communities where Community Bank branches operate, directly benefiting local economies.

- Scholarship Programs: The bank actively funds and supports educational opportunities for local residents, investing in future generations.

- Community Project Support: Bendigo and Adelaide Bank provides financial and in-kind support to various local projects, enhancing community infrastructure and services.

- Purpose-Driven Approach: These activities are not just philanthropic; they are integral to the bank's identity and its strategy to build stronger, more resilient communities.

Digital Transformation & Community Impact

Bendigo and Adelaide Bank's key activities revolve around providing a full spectrum of banking and financial services. This includes the origination and management of loans, offering wealth management solutions, and a strong focus on digital transformation to enhance customer experience and operational efficiency.

Their unique community engagement model, particularly through Community Bank branches, involves reinvesting profits and supporting local initiatives, which is a defining characteristic of their operations.

| Key Activity | Description | 2024 Data/Context |

| Lending Operations | Originating and managing home loans, personal loans, and business loans. | Total lending portfolio of $72.4 billion. |

| Wealth Management | Providing financial planning, investment products, and superannuation. | Operating within a superannuation sector managing over $3.5 trillion in assets. |

| Digital Transformation | Modernizing core systems, cloud migration, and process automation. | 12% increase in digital transaction volumes in H1 FY24. Up digital banking app customer base grew 25% in 2023. |

| Community Engagement | Reinvesting profits into local communities via Community Bank branches. | Statutory profit after tax of $990 million in FY23, with profits channeled into community initiatives. |

Full Version Awaits

Business Model Canvas

The Bendigo & Adelaide Bank Business Model Canvas you are previewing is the exact document you will receive upon purchase. This isn't a sample or a mockup; it's a direct representation of the comprehensive analysis that will be yours. You'll gain full access to this same, professionally structured document, ready for your immediate use and strategic planning.

Resources

Financial Capital and Funding Base

Bendigo and Adelaide Bank's financial capital and funding base are its bedrock, enabling its core lending operations and ensuring resilience. This strength is significantly bolstered by robust capital levels and a substantial customer deposit base.

Customer deposits, a vital source of funding, saw a healthy increase of 3.4% in the fiscal year 2024, reaching an impressive $68.3 billion. This growth underscores customer confidence and provides the bank with a stable and cost-effective foundation for its lending activities.

Human Capital and Expertise

Bendigo and Adelaide Bank's human capital is a core asset, with over 7,000 dedicated employees. Their collective expertise spans critical areas like financial services, cutting-edge technology, and building strong customer relationships, forming the backbone of the bank's operations and strategic initiatives.

The bank actively cultivates specialized teams, such as those focused on driving digital transformation and supporting the vital agribusiness sector. This deep bench of talent ensures the bank can effectively navigate evolving market demands and deliver tailored solutions to its diverse customer base.

Technology Infrastructure and Digital Platforms

Bendigo and Adelaide Bank's technological backbone includes its core banking systems, which are undergoing modernization to enhance operational efficiency and customer service. These systems are critical for managing accounts, transactions, and customer data securely and reliably.

Key digital platforms like the Up super app and the Bendigo Lending Platform are vital for customer engagement and streamlined product delivery. The Up app, for instance, offers a modern, user-friendly banking experience, while the lending platform aims to simplify the mortgage application process.

The bank's investment in cloud infrastructure is a strategic move to increase agility, scalability, and data processing capabilities. This allows for faster innovation and a more resilient operational environment, supporting the delivery of new digital services and improving overall system performance.

Brand Reputation and Trust

Bendigo and Adelaide Bank's brand reputation and trust are cornerstones of its business model, acting as a vital intangible asset. This reputation is cultivated through a deep commitment to community engagement and a consistent focus on customer satisfaction, which has earned it recognition as Australia's most trusted bank.

This trust translates into tangible benefits, fostering customer loyalty and attracting new business. For instance, in the 2024 financial year, the bank reported a customer satisfaction score of 85%, a testament to its ongoing efforts.

- Community Focus: The bank actively invests in local communities, supporting various initiatives which strengthens its ties and builds goodwill.

- Customer Loyalty: High customer satisfaction scores, like the 85% reported in FY24, directly contribute to customer retention and organic growth.

- Brand Equity: Being recognized as Australia's most trusted bank provides a significant competitive advantage in a crowded financial services market.

Extensive Branch and Partner Network

Bendigo and Adelaide Bank leverages an extensive physical branch network, including its unique Community Bank model, alongside a robust partner network. This dual approach ensures broad reach and accessibility throughout Australia, acting as a critical resource for attracting new customers and delivering services effectively.

In 2024, the bank continued to emphasize its community-centric approach. For instance, its Community Bank network, which comprises over 300 branches as of recent reports, plays a vital role in local economic development and customer engagement, often outperforming traditional branches in customer loyalty and community support.

- Physical Presence: Over 300 Community Bank branches and a significant number of traditional branches provide direct customer interaction points.

- Partner Channels: Collaborations with other businesses and organizations extend the bank's reach beyond its own physical footprint.

- Customer Acquisition: The diversified channel strategy is instrumental in reaching a wider customer base and fostering strong relationships.

- Service Delivery: This network ensures efficient and accessible service delivery, catering to diverse customer needs across urban and rural areas.

The Bank's Pillars: Capital, People, Tech, Trust, Reach

Bendigo and Adelaide Bank's key resources are multifaceted, encompassing financial strength, dedicated human capital, robust technology, a trusted brand, and an extensive physical and partner network.

Financial capital, evidenced by a 3.4% increase in customer deposits to $68.3 billion in FY24, underpins its lending capabilities. Human capital, with over 7,000 employees, drives innovation and customer service, particularly in specialized areas like digital transformation and agribusiness.

Technological assets, including modernized core banking systems and digital platforms like the Up app, enhance efficiency and customer experience. The bank's brand, recognized as Australia's most trusted, fosters loyalty, with an 85% customer satisfaction score in FY24.

Its physical network, featuring over 300 Community Bank branches, alongside partner channels, ensures broad accessibility and community engagement, a key differentiator in customer acquisition and service delivery.

| Resource Category | Key Components | FY24 Data/Highlights |

|---|---|---|

| Financial Capital | Capital Levels, Customer Deposits | Customer Deposits: $68.3 billion (+3.4% growth) |

| Human Capital | Employees, Specialized Teams | Over 7,000 employees; Digital transformation & Agribusiness teams |

| Technology | Core Banking Systems, Digital Platforms | Up super app, Bendigo Lending Platform, Cloud infrastructure |

| Brand & Reputation | Trust, Community Engagement | Australia's most trusted bank; 85% customer satisfaction |

| Physical & Partner Network | Branch Network, Community Banks | Over 300 Community Bank branches |

Value Propositions

Community-Centric Banking

Bendigo and Adelaide Bank's Community Bank model is a cornerstone of its value proposition, directly channeling a substantial portion of profits back into local communities. This commitment fosters strong customer loyalty among those who prioritize local economic growth and development.

In the 2023 financial year, Bendigo and Adelaide Bank reported a cash net profit after tax of $511 million. A key aspect of their community focus is the Community Bank model, which has seen over $300 million returned to local communities since its inception.

Comprehensive Product and Service Suite

Bendigo and Adelaide Bank provides a comprehensive selection of personal and business banking products, including home loans and credit cards. This extensive suite ensures customers can manage all their financial needs through a single provider, simplifying their banking experience.

Beyond transactional banking, the bank also offers robust wealth management services. This holistic approach allows them to cater to customers across different life stages and evolving financial requirements, from everyday banking to long-term investment planning.

In 2024, Bendigo and Adelaide Bank reported a net interest margin of 1.76%, reflecting their ability to manage diverse product offerings effectively. Their commitment to a broad product suite supports their strategy of being a primary financial partner for their customers.

Trusted and Relationship-Focused Service

Bendigo and Adelaide Bank positions itself as a relationship-focused institution, striving to be Australia's most trusted bank. This commitment is evident in their emphasis on quality service and personalized customer interactions, aiming to build strong, lasting connections.

Their strategy blends this human-centric approach with digital innovation, ensuring customers benefit from both personal touchpoints and convenient online capabilities. This dual focus creates a well-rounded and adaptable customer experience.

In 2024, the bank continued to invest in its people and technology, reflecting this value proposition. For instance, their customer satisfaction scores, as reported in their annual statements, consistently highlight the value customers place on the bank's responsive and helpful staff.

Digital Innovation and Convenience

Bendigo and Adelaide Bank's commitment to digital innovation is a core value proposition, offering customers highly convenient and efficient banking experiences. Platforms like Up, their digital-only bank, exemplify this, providing seamless online interactions and faster service delivery. For instance, in the first half of 2024, Up reported a significant increase in customer acquisition, driven by its user-friendly interface and quick digital processes, including faster home loan approvals which are crucial for many customers.

This focus on digital convenience directly addresses the evolving needs of modern consumers who expect instant access and streamlined transactions. The bank’s investment in its digital infrastructure allows for quicker processing times across various services, from account opening to loan applications. This agility not only enhances customer satisfaction but also positions Bendigo and Adelaide Bank competitively in a rapidly digitizing financial landscape.

- Digital Transformation: Ongoing investment in technology to enhance customer experience.

- Up Digital Bank: A key platform offering a modern, convenient banking solution.

- Efficiency Gains: Streamlined processes leading to faster service delivery, such as quicker home loan approvals.

- Customer Acquisition: Digital offerings are a significant driver for attracting new customers, as seen with Up's growth in early 2024.

Support for Regional and Rural Australia

Bendigo and Adelaide Bank's value proposition for regional and rural Australia is deeply rooted in its history and community focus. The bank offers specialized financial products and services designed to meet the unique challenges and opportunities faced by individuals, small businesses, and agricultural enterprises in these areas.

This commitment directly supports the economic development and sustainability of regional communities. For instance, in 2023, Bendigo and Adelaide Bank reported a strong lending performance in regional areas, with a significant portion of its home loan portfolio supporting customers outside major metropolitan centers.

- Tailored Financial Solutions: Offering products specifically designed for agribusiness, small business, and personal banking needs in regional settings.

- Community Investment: Actively investing in local communities through sponsorships and partnerships that foster economic growth and social well-being.

- Accessibility: Maintaining a physical presence and digital services that ensure access to banking for those in remote or underserved areas.

- Economic Vitality: Contributing to the economic health of regional Australia by supporting local businesses and employment.

Community-Powered Banking: A Distinct Value Proposition

Bendigo and Adelaide Bank's core value proposition centers on its unique Community Bank model, which demonstrably returns profits to local areas. This fosters deep customer loyalty by aligning financial services with community well-being.

The bank offers a comprehensive suite of banking products, from personal loans to business solutions, aiming to be a one-stop financial partner. This breadth of offerings simplifies customer financial management.

Furthermore, Bendigo and Adelaide Bank emphasizes a relationship-driven approach, prioritizing personalized service and trust. This human-centric strategy is augmented by significant investments in digital innovation, creating a blended, convenient customer experience.

| Value Proposition Area | Key Offering | Impact/Benefit | Supporting Data (2023/2024) |

|---|---|---|---|

| Community Banking | Profit sharing with local communities | Strong customer loyalty, local economic development | Over $300 million returned to communities since inception. |

| Product Breadth | Personal and business banking, wealth management | One-stop financial solution, caters to diverse needs | Net interest margin of 1.76% in 2024 reflects diverse product management. |

| Relationship Focus | Personalized service, trust building | High customer satisfaction, lasting connections | Consistent positive customer satisfaction scores related to staff helpfulness. |

| Digital Innovation | Digital banking platforms (e.g., Up) | Convenience, efficiency, faster service delivery | Up reported significant customer acquisition growth in early 2024. |

Customer Relationships

Community-Based Engagement

Bendigo and Adelaide Bank's Community Bank model thrives on building deep, local relationships. Customers often feel a direct connection to the bank's positive impact on their communities, fostering loyalty and trust.

This engagement is actively cultivated through local boards, which provide governance and local insight, and by funding community projects. In 2024, the bank continued to support numerous local initiatives, reinforcing its commitment to community well-being.

Personalized service at the branch level is another cornerstone. This hands-on approach, where staff know their customers, differentiates the Community Bank model and strengthens customer bonds, contributing to a strong sense of belonging.

Personalised and Human-Centric Service

Bendigo and Adelaide Bank prioritizes a human-centric approach to customer relationships, even amidst digital evolution. Their strategy emphasizes personalized interactions, ensuring customers feel valued and understood through direct engagement channels. This commitment translates into a 'human when it matters' experience, fostering loyalty and trust.

Digital Self-Service and Support

Bendigo and Adelaide Bank offers robust digital self-service options, including online banking and mobile applications like Up, allowing customers to manage their accounts and transactions conveniently. This digital focus caters to a growing preference for remote financial management, enhancing accessibility and customer engagement.

The bank's digital mortgage application process streamlines a traditionally complex procedure, providing a user-friendly experience for borrowers. This digital innovation aims to reduce friction and improve turnaround times, reflecting a commitment to modernizing customer interactions.

In 2024, digital engagement continues to be a key driver for financial institutions. Banks like Bendigo and Adelaide are investing heavily in these platforms to meet customer expectations for 24/7 access and efficient service delivery, a trend that is expected to accelerate.

Dedicated Relationship Managers for Businesses

Bendigo and Adelaide Bank recognizes that businesses, whether small startups or large corporations, have unique financial journeys. To support these diverse needs, they provide dedicated relationship managers. These professionals act as a single point of contact, offering personalized guidance and strategic advice tailored to each client's specific situation.

This approach fosters deeper, more enduring partnerships with their commercial clientele. By understanding the intricacies of a business, these managers can proactively identify opportunities and offer solutions that drive growth and stability. For instance, in 2024, the bank reported a significant increase in customer satisfaction scores within its business banking division, directly correlating with the effectiveness of its dedicated relationship manager program.

- Tailored Advice: Dedicated managers offer customized financial strategies for businesses of all sizes.

- Long-Term Partnerships: This personalized service cultivates stronger, lasting relationships with commercial clients.

- Proactive Support: Managers anticipate needs and provide solutions, enhancing client success.

- Customer Satisfaction: The program has demonstrably improved client satisfaction, as evidenced by 2024 performance metrics.

Proactive Financial Wellbeing Support

Bendigo and Adelaide Bank actively supports customer financial wellbeing through its Financial Inclusion Action Plan. This commitment translates into accessible products and services designed to uplift all customers, particularly those facing vulnerabilities.

The bank prioritizes financial literacy, equipping customers with the knowledge to make sound financial decisions. In 2024, the bank continued to expand its digital tools and educational resources aimed at improving financial confidence and capability across its customer base.

- Financial Inclusion Action Plan: A strategic roadmap to improve access and outcomes for all customers.

- Accessible Products and Services: Offering a range of banking solutions tailored to diverse needs.

- Financial Literacy Programs: Initiatives designed to enhance customers' understanding and management of their finances.

- Support for Vulnerable Customers: Targeted assistance and resources for individuals facing financial challenges.

Community Bank Model: Cultivating Strong Customer Relationships

Bendigo and Adelaide Bank cultivates strong customer relationships through its unique Community Bank model, fostering local engagement and trust by supporting community projects and providing personalized, human-centric service. This approach extends to business clients with dedicated relationship managers offering tailored advice and building long-term partnerships.

| Customer Relationship Aspect | Key Features | 2024 Impact/Focus |

|---|---|---|

| Community Engagement | Local boards, community project funding | Reinforced commitment to local well-being; continued support for numerous initiatives. |

| Personalized Service | Branch-level staff knowing customers, dedicated relationship managers for businesses | Differentiated model, strengthened customer bonds, improved business client satisfaction. |

| Digital Accessibility | Online banking, mobile apps (Up), streamlined digital mortgage applications | Catered to preference for remote management, enhanced accessibility, modernized interactions. |

| Financial Wellbeing Support | Financial Inclusion Action Plan, financial literacy programs | Improved access and outcomes, enhanced financial confidence and capability. |

Channels

Branch Network (including Community Banks)

Bendigo and Adelaide Bank's branch network, including its unique Community Bank model, acts as a crucial touchpoint for customers seeking face-to-face interactions and local support. These branches are not just about transactions; they foster community engagement and build trust, which is vital for a regional bank.

The physical presence of branches remains a significant driver of business. For the half-year ending December 2024, the branch network was instrumental in facilitating 30% of all residential lending settlements, highlighting its continued importance in key banking activities.

Digital Platforms (Website and Mobile Apps)

Bendigo and Adelaide Bank leverages its official website and mobile banking applications as crucial digital platforms. These channels offer a full suite of services, from personal and business banking to loan applications and wealth management, providing customers with convenient access to financial tools.

The bank's commitment to digital innovation is particularly evident in the performance of its Up app. In the half-year period concluding December 2024, the Up app experienced a significant 13.2% growth in its customer base, highlighting its increasing popularity and effectiveness in engaging users.

Partner Networks (Mortgage Brokers)

Partner networks, especially mortgage brokers, are vital for reaching customers with lending products, particularly for home loans. These intermediaries significantly expand the bank's distribution capabilities.

In the first half of the 2025 financial year, the Bendigo Lending Platform was responsible for 28% of all residential lending settlements. This highlights the substantial role these third-party channels play in the bank's overall lending volume.

Furthermore, digital mortgages represented 19% of residential lending settlements during the same period. This demonstrates a growing trend towards digital channels, often facilitated through broker networks or directly by the bank.

Customer Contact Centres

Customer Contact Centres are a vital channel for Bendigo and Adelaide Bank, offering direct engagement for inquiries, support, and transactions. This ensures customers who prefer telephone interactions have a readily accessible avenue for their banking needs.

In 2024, the bank continued to invest in its contact centre capabilities, aiming for efficient and effective customer service. This focus is critical for maintaining customer loyalty and addressing a significant portion of customer interactions.

- Direct Customer Engagement: Telephone banking and dedicated contact centres provide a primary touchpoint for resolving queries and facilitating transactions.

- Accessibility: This channel caters to customers who prefer or require phone-based communication, ensuring inclusivity in service delivery.

- Operational Efficiency: Effective contact centre management contributes to streamlined operations and can reduce the need for in-person branch visits for routine matters.

- Customer Support: These centres are crucial for providing timely assistance, troubleshooting issues, and offering guidance on banking products and services.

Automated Teller Machines (ATMs)

Automated Teller Machines (ATMs) serve as a crucial physical touchpoint, offering customers convenient access for essential transactions like cash withdrawals, deposits, and balance checks. This channel directly supports basic banking needs, ensuring accessibility even when digital platforms or branches are not utilized. As of 2024, Bendigo and Adelaide Bank operates a substantial ATM network across Australia, facilitating everyday banking for a broad customer base.

The ATM network complements Bendigo and Adelaide Bank's digital and branch offerings, providing a consistent and reliable channel for fundamental banking services. This physical presence remains vital for customer engagement and transaction completion, especially for those who prefer or require in-person interactions for simple tasks. The bank continues to invest in maintaining and upgrading its ATM fleet to ensure optimal functionality and security.

- ATM Network Reach: Bendigo and Adelaide Bank maintains a significant ATM footprint across Australia, providing widespread access for its customers.

- Transaction Capabilities: ATMs facilitate core banking functions including cash withdrawals, deposits, and balance inquiries, meeting fundamental customer needs.

- Channel Complementarity: The ATM channel works in tandem with digital banking and branch services to offer a comprehensive customer experience.

Multi-Channel Banking: Reaching Customers Everywhere

Bendigo and Adelaide Bank utilizes a multi-channel approach to reach its customers, encompassing both physical and digital touchpoints. This strategy ensures broad accessibility and caters to diverse customer preferences for banking interactions.

The bank's branch network, including its unique Community Bank model, remains a cornerstone for customer engagement and local support. Digital platforms, such as the official website and mobile apps, offer comprehensive self-service options, while partner networks, particularly mortgage brokers, are critical for expanding lending reach.

Customer Contact Centres provide essential support for inquiries and transactions, complementing the accessibility of ATMs for everyday banking needs. This integrated channel strategy is key to delivering a consistent and convenient banking experience.

| Channel | Description | Key Data (H1 FY2025 unless otherwise stated) |

|---|---|---|

| Branches (incl. Community Bank) | Face-to-face interaction, local support, community engagement | 30% of residential lending settlements |

| Digital Platforms (Website, Mobile Apps) | Full suite of services, convenient access, self-service | Up app customer base grew 13.2% |

| Partner Networks (e.g., Mortgage Brokers) | Expanded distribution for lending products | Bendigo Lending Platform responsible for 28% of residential lending settlements; Digital mortgages 19% |

| Customer Contact Centres | Direct engagement for inquiries, support, transactions | Continued investment in capabilities for efficient service (2024) |

| ATMs | Convenient access for essential transactions (cash, deposits) | Substantial network across Australia (2024) |

Customer Segments

Individuals and Households

Bendigo and Adelaide Bank serves a diverse array of individuals and households, catering to everyone from digitally-savvy young adults drawn to offerings like Up, to families needing comprehensive home loan and everyday banking solutions. By December 2024, the bank had expanded its customer base to over 2.7 million individuals.

Small to Medium-sized Enterprises (SMEs)

Bendigo and Adelaide Bank's customer segment includes a broad range of Small to Medium-sized Enterprises (SMEs) across diverse industries. They provide essential business banking services, lending options, and tools for effective cash flow management to help these businesses thrive.

A key focus for the bank is the support and growth of microbusinesses, recognizing their vital role in the economy. This commitment extends to their dedicated agribusiness division, aiming to facilitate transformation and success within this sector as well.

In 2024, SMEs continued to be a significant driver of the Australian economy, with data indicating they represent over 97% of all businesses. Bendigo and Adelaide Bank's strategies are designed to capture a substantial portion of this market by offering tailored financial solutions.

Agribusiness Customers

Bendigo and Adelaide Bank recognizes the unique needs of the agricultural sector, serving a specialized segment of agribusiness customers. This includes farmers and broader agribusiness enterprises, offering them financial products and services specifically designed for their operations.

This focus on agribusiness is a significant growth driver for the bank. In fact, agribusiness cash earnings saw a substantial increase of 13.4% in the fiscal year 2024, highlighting the segment's importance and the bank's success in serving it.

Regional and Rural Communities

Bendigo and Adelaide Bank specifically caters to regional and rural communities throughout Australia, leveraging its extensive network of Community Bank branches. This approach resonates deeply with these areas, as customers prioritize local investment and a strong community focus in their banking relationships. For instance, in 2024, the bank continued its commitment to these regions, with a significant portion of its customer base residing outside major metropolitan centers.

The bank's Community Bank model is a key differentiator, directly channeling profits back into the local areas where branches operate. This fosters a sense of ownership and mutual benefit, making it an attractive proposition for residents and businesses in these locations. Data from 2024 highlights the tangible impact of this model, with numerous community projects and initiatives funded through the success of these local branches.

- Community Focus: Customers in regional and rural areas value the bank's commitment to local development and community well-being.

- Local Investment: The Community Bank model ensures profits are reinvested locally, strengthening regional economies.

- Branch Network: A strong physical presence in regional Australia is crucial for serving this customer segment effectively.

- Customer Loyalty: The alignment of values between the bank and its regional customers drives strong loyalty and engagement.

Digitally Savvy Customers (e.g., Up users)

Digitally savvy customers, like those using the Up brand, are a core focus for Bendigo and Adelaide Bank. These individuals are comfortable and actively use digital channels for their banking needs, from everyday transactions to more complex financial management. The Up brand, in particular, has seen substantial growth by effectively serving this segment.

In 2024, the trend of digital adoption continued to accelerate. For instance, the number of active digital users across the Australian banking sector saw a notable uptick, with many customers preferring mobile apps for convenience. Bendigo and Adelaide Bank's investment in its digital offerings, including the Up app, positions it well to capture and retain these engaged users.

- Digital Preference: Customers in this segment actively choose digital platforms over traditional branch interactions.

- Up Brand's Success: The Up brand has demonstrated a strong ability to attract and retain digitally native customers.

- Growth in Digital Engagement: In 2024, there was a marked increase in customers utilizing mobile banking apps for a wide range of financial services.

- Strategic Importance: Catering to digitally savvy customers is crucial for future growth and maintaining a competitive edge in the evolving banking landscape.

Serving Over 2.7 Million Diverse Australian Customers

Bendigo and Adelaide Bank serves a broad spectrum of customers, from individuals and families seeking comprehensive banking solutions to digitally-focused users drawn to its innovative Up brand. By December 2024, the bank had successfully grown its customer base to over 2.7 million individuals, reflecting its wide reach.

The bank also places a strong emphasis on Small to Medium-sized Enterprises (SMEs) and microbusinesses, recognizing their critical role in the Australian economy. In 2024, SMEs continued to represent over 97% of all Australian businesses, underscoring the importance of tailored financial services for this segment.

Furthermore, Bendigo and Adelaide Bank actively supports the agribusiness sector, a key growth area. This commitment is evident in the 13.4% increase in agribusiness cash earnings observed in fiscal year 2024, highlighting the bank's effectiveness in serving this specialized market.

| Customer Segment | Key Characteristics | 2024 Relevance/Data |

|---|---|---|

| Individuals & Households | Diverse needs, from digital banking (Up) to traditional family finance. | Over 2.7 million customers by December 2024. |

| SMEs & Microbusinesses | Require business banking, lending, and cash flow management. | SMEs constitute over 97% of Australian businesses. |

| Agribusiness | Specialized financial products for farmers and agricultural enterprises. | Agribusiness cash earnings grew 13.4% in FY2024. |

| Regional & Rural Communities | Value local investment and community focus via Community Bank branches. | Significant customer base resides outside major metropolitan centers. |

| Digitally Savvy Customers | Prefer digital channels, actively use mobile apps. | Up brand shows strong growth in this segment. |

Cost Structure

Employee Salaries and Benefits

Employee salaries, wages, and benefits represent a substantial cost for Bendigo and Adelaide Bank, supporting its extensive network of over 7,000 employees. These individuals are crucial to the bank's operations across its branch network, corporate offices, and burgeoning digital services.

In the financial year 2024, the bank actively pursued productivity enhancements, which resulted in a 4% decrease in full-time equivalent (FTE) employees. This strategic move aimed to optimize operational efficiency and manage cost structures more effectively.

Technology and IT Infrastructure Costs

Bendigo and Adelaide Bank's commitment to staying competitive necessitates significant ongoing investment in technology. This includes the crucial maintenance of its core banking systems, a vital component for daily operations.

The bank is also heavily invested in its cloud migration strategy and the continuous development of its digital platforms, aiming to enhance customer experience and operational efficiency.

Furthermore, robust cybersecurity measures are a substantial and ever-increasing cost, reflecting the evolving threat landscape. For fiscal years 2025 and 2026, investment in these technology areas is projected to rise by an estimated $30 million to $40 million annually.

Branch Network and Property Expenses

Bendigo and Adelaide Bank's extensive branch network, a cornerstone of its customer engagement strategy, incurs substantial costs. These include expenditures on property leases or ownership, ongoing maintenance, utilities, and the salaries of branch staff. In the 2024 financial year, the bank reported operating expenses that reflect these significant investments in its physical presence across Australia.

The unique Community Bank model, where branches are locally owned and operated, also introduces a layer of shared operational costs. While this model fosters community ties, it necessitates shared resources for back-office functions and technology, contributing to the overall cost structure. These shared expenses are crucial for maintaining the efficiency and reach of the bank’s distributed network.

Marketing and Advertising Expenses

Bendigo and Adelaide Bank allocates significant resources to marketing and advertising, covering brand promotion and customer acquisition across diverse channels. This expenditure is crucial for maintaining brand visibility and attracting new customers to both the core Bendigo Bank offering and its digital banking arm, Up.

In the financial year 2024, the bank reported marketing expenses as part of its operating costs. While specific figures for marketing and advertising alone are often integrated within broader operational expenditure lines, the bank's commitment to growth, particularly through its digital platforms, necessitates consistent investment in these areas. For instance, Up's strategy heavily relies on digital marketing, social media engagement, and targeted online advertising to drive user acquisition and retention.

- Brand Building: Ongoing investment in brand campaigns to reinforce trust and community connection for Bendigo Bank.

- Digital Acquisition: Significant spend on digital marketing, search engine optimization, and social media for Up to attract new users.

- Promotional Offers: Costs associated with customer acquisition incentives and product launch campaigns.

- Content Creation: Development of marketing materials, including digital content and advertising creatives.

Regulatory and Compliance Costs

Bendigo and Adelaide Bank faces substantial costs to maintain compliance with Australia's rigorous banking regulations. These expenses cover essential areas like detailed reporting, robust risk management systems, and regular external audits. For instance, in the 2023 financial year, the bank reported increased investment in its risk and compliance functions, reflecting the ongoing effort to strengthen these critical frameworks.

The bank's commitment to adhering to these standards translates into significant operational expenditures. These costs are crucial for ensuring the stability and integrity of its operations and protecting customer interests. The continuous strengthening of risk and compliance frameworks is not just a regulatory necessity but a strategic imperative for maintaining trust and a strong market position.

- Reporting and Data Management: Costs associated with generating and submitting regulatory reports to bodies like APRA.

- Risk Management Systems: Investment in technology and personnel for credit, market, and operational risk oversight.

- Audit and Assurance: Fees paid to internal and external auditors to verify compliance and financial accuracy.

- Compliance Program Development: Expenses related to training, policy updates, and implementing new regulatory requirements.

Optimizing Bank Costs: A Strategic Shift Towards Efficiency and Digital

Bendigo and Adelaide Bank's cost structure is significantly influenced by its extensive employee base, technology investments, branch network, marketing efforts, and regulatory compliance. The bank's strategic focus on efficiency, as seen in its 2024 FTE reduction, aims to manage these costs effectively while pursuing growth, particularly in digital channels.

Key cost drivers include employee compensation, technology upgrades and maintenance, physical branch operations, marketing and customer acquisition, and robust risk and compliance frameworks. These elements are fundamental to the bank's operational model and its ability to serve customers and meet regulatory obligations.

The bank's commitment to its Community Bank model also contributes to shared operational costs, ensuring the efficient functioning of its distributed network. These ongoing investments are critical for maintaining competitiveness and customer trust in the evolving financial landscape.

| Cost Category | Description | Financial Year 2024 Impact/Focus |

|---|---|---|

| Employee Costs | Salaries, wages, benefits for ~7,000 employees. | 4% FTE reduction for productivity enhancement. |

| Technology Investment | Core banking systems, cloud migration, digital platforms, cybersecurity. | Projected $30-40 million annual increase in investment for FY25/26. |

| Branch Network | Leases, maintenance, utilities, branch staff. | Significant operating expenses reflecting physical presence. |

| Marketing & Advertising | Brand promotion, customer acquisition (Bendigo Bank & Up). | Integral to growth strategy, especially digital marketing for Up. |

| Regulatory Compliance | Reporting, risk management, audits, policy updates. | Increased investment in risk/compliance functions (FY23). |

Revenue Streams

Net Interest Income (NII)

Net Interest Income (NII) is Bendigo and Adelaide Bank's main way of making money. It comes from the difference between the interest they earn on loans and investments and the interest they pay out on customer deposits and other borrowings.

For the financial year 2024, the bank reported a Net Interest Margin (NIM) of 1.90%. This figure is crucial as it directly reflects the profitability of their core lending and deposit-taking activities.

Lending Fees and Charges

Bendigo and Adelaide Bank generates revenue from lending fees and charges, which supplement its core interest income. These fees include charges for originating loans, ongoing service fees, and penalties for late payments. For example, in the first half of FY24, the bank reported a statutory profit of $521 million, indicating robust lending activity that likely generated substantial fee income alongside interest.

Account and Transaction Fees

Bendigo and Adelaide Bank generates revenue through account and transaction fees, which form a significant portion of its non-interest income. These fees are levied for various banking services, encompassing account maintenance charges, the processing of daily transactions, and specific service fees like ATM withdrawals and international money transfers.

In the fiscal year 2023, Bendigo and Adelaide Bank reported total operating income of AUD 1.75 billion. While specific breakdowns of fee income are not always granularly detailed in public reports, these charges are a consistent contributor to the bank's profitability, reflecting the volume and complexity of customer banking activities.

Wealth Management Fees

Bendigo and Adelaide Bank generates income through wealth management services, encompassing advisory fees, management fees for investment products like superannuation and managed funds, and commissions from financial product sales. This revenue stream is crucial for diversifying the bank's overall income, reducing reliance on traditional lending. For the fiscal year 2023, the bank reported a statutory net profit after tax of $990 million, showcasing the contribution of its diverse operations, including wealth management.

The bank's wealth management arm, BENDIGO AND ADELAIDE BANK WEALTH, offers a range of products and services designed to meet the financial needs of its customers. This diversification strategy is key to maintaining profitability in a competitive financial landscape.

Key components of this revenue stream include:

- Advisory Fees: Charges for personalized financial planning and advice.

- Management Fees: Ongoing fees for managing investment portfolios and superannuation accounts.

- Commissions: Earnings from the sale of financial products such as insurance and investment solutions.

Other Income and Commissions

Bendigo and Adelaide Bank generates revenue through a variety of sources beyond traditional interest income. These include fees earned from partner networks, which leverage the bank's infrastructure and customer base. Additionally, foreign exchange transactions contribute to this income stream, reflecting the bank's role in international commerce.

Other non-interest income activities also play a significant role. For 2024, the bank reported total revenue of A$2.01 billion, with a portion of this attributed to these diverse revenue streams.

- Fees from partner networks

- Foreign exchange income

- Other non-interest income activities

- Total 2024 revenue: A$2.01 billion

Bank's Diverse Revenue: A$2.01 Billion in FY24

Bendigo and Adelaide Bank’s revenue streams are diverse, extending beyond core Net Interest Income (NII). These include various fees and commissions from banking services and wealth management, alongside income from partner networks and foreign exchange. For the financial year 2024, the bank reported total revenue of A$2.01 billion, reflecting the contribution of these varied activities.

| Revenue Stream | Description | FY24 Impact (Illustrative) |

| Net Interest Income (NII) | Interest earned on loans minus interest paid on deposits. | NIM of 1.90% |

| Lending Fees and Charges | Fees for loan origination, servicing, and late payments. | Contributes to robust lending activity. |

| Account and Transaction Fees | Charges for account maintenance, transaction processing, and specific services. | Significant portion of non-interest income. |

| Wealth Management Income | Advisory, management, and commission fees from financial products. | Diversifies income, contributing to overall profitability. |

| Partner Networks & FX Income | Fees from leveraging infrastructure and customer base, plus foreign exchange gains. | Part of the A$2.01 billion total revenue. |

Business Model Canvas Data Sources

The Bendigo & Adelaide Bank Business Model Canvas is informed by a blend of internal financial data, comprehensive market research, and strategic analysis of the Australian banking sector. This ensures a robust and data-driven representation of the bank's operations and market positioning.