Richelieu Porter's Five Forces Analysis

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Richelieu Bundle

Go Beyond the Preview—Access the Full Strategic Report

Richelieu's competitive landscape is shaped by intense rivalry, the bargaining power of buyers, and the threat of new entrants. Understanding these forces is crucial for navigating the market effectively.

The complete report reveals the real forces shaping Richelieu’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

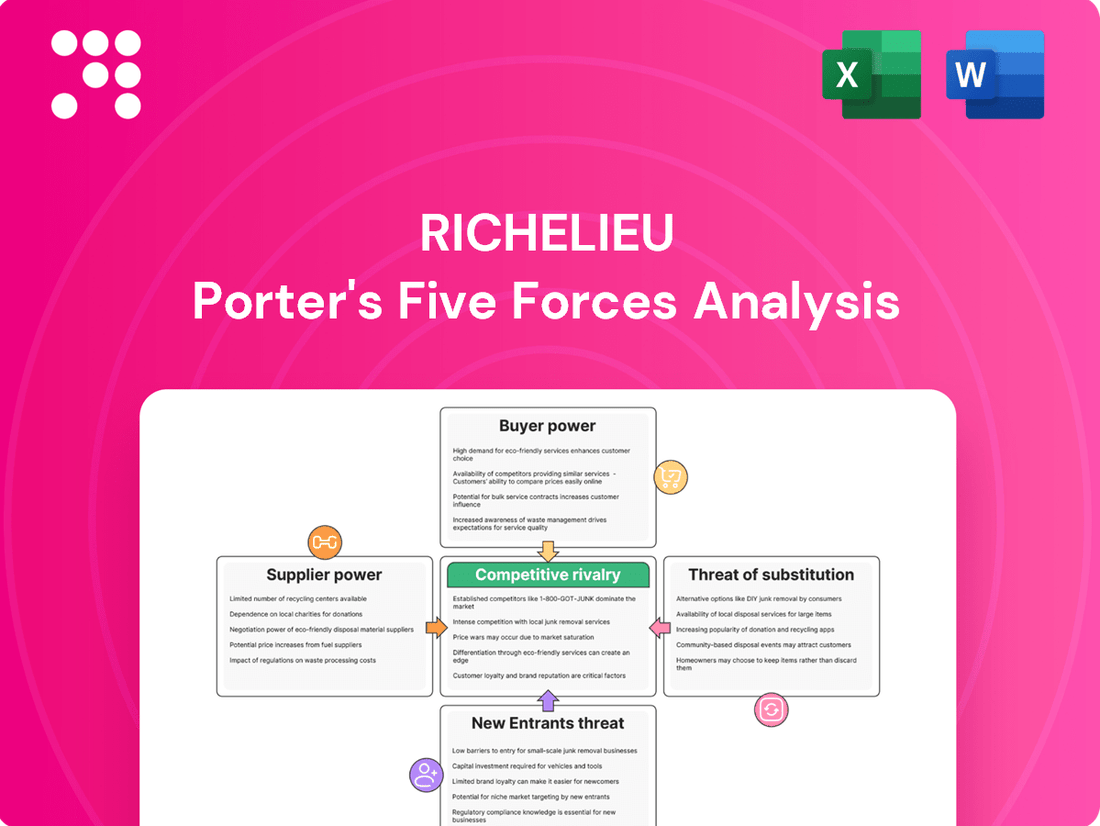

Suppliers Bargaining Power

Concentrated Supplier Base

Richelieu's bargaining power of suppliers is influenced by the concentration of its supplier base. If a few key suppliers dominate the market for essential specialty hardware components or raw materials, such as specific alloys or intricate electronic parts, Richelieu would face significant supplier leverage. This dependence allows these concentrated suppliers to potentially dictate pricing, terms, and delivery timelines, impacting Richelieu's cost structure and operational efficiency.

Uniqueness of Products/Services

When Richelieu's suppliers provide highly unique or proprietary goods crucial for its own distinct product lines, their leverage grows significantly. This is especially potent if the cost and complexity of switching to another supplier are substantial, perhaps due to specialized equipment, necessary certifications, or extensive vetting periods.

Threat of Forward Integration

The threat of forward integration by suppliers poses a significant concern for Richelieu. If suppliers were to start manufacturing their own finished furniture or directly supplying cabinet makers, they could effectively cut out Richelieu as an intermediary. This would directly impact Richelieu's sales volume and pricing power.

For instance, if a key supplier of wood or hardware decided to establish its own furniture production lines, it could leverage its existing supply chain and cost advantages. This move would mean fewer orders for Richelieu, potentially forcing them to accept lower margins or lose market share in certain segments.

Importance of Supplier's Input to Richelieu's Cost Structure

The significance of a supplier's input to Richelieu's overall cost structure directly impacts the supplier's bargaining power. When a particular input constitutes a substantial percentage of Richelieu's total production expenses, suppliers gain leverage. This leverage allows them to potentially increase prices, which can then squeeze Richelieu's profit margins, even if the price hike itself seems minor in absolute terms.

For instance, if a key raw material represents 30% of Richelieu's cost of goods sold, any price increase from that supplier will have a magnified effect on profitability. In 2024, Richelieu's cost of goods sold was approximately $650 million. If a critical component, like specialized leather, accounted for 20% of that cost, it would represent $130 million. A 5% price increase on this leather would add $6.5 million to Richelieu's expenses, a notable impact.

- High Input Cost Proportion: If a supplier's input is a major cost driver for Richelieu, it significantly enhances the supplier's bargaining power.

- Profitability Impact: Even small price increases from such suppliers can disproportionately affect Richelieu's overall profitability.

- 2024 Data Example: With Richelieu's 2024 cost of goods sold around $650 million, a 20% input cost ($130 million) from a single supplier makes them influential.

- Leverage through Price Hikes: Suppliers can exert pressure by raising prices, directly impacting Richelieu's bottom line.

Availability of Substitutes for Supplier's Products

The bargaining power of suppliers for Richelieu Hardware is significantly weakened when there are readily available substitutes for the specialty hardware they source. If Richelieu can easily find alternative manufacturers or importers offering similar products, suppliers lose their leverage to command higher prices or dictate unfavorable terms. This abundance of alternatives creates a competitive environment among suppliers, benefiting Richelieu.

For instance, the global market for specialty hardware is diverse, with numerous manufacturers in Asia, Europe, and North America. In 2024, the specialty hardware market, estimated to be worth billions, sees a steady influx of new entrants and established players continually innovating their product lines. This dynamic landscape means Richelieu isn't overly reliant on any single supplier.

- Availability of Substitutes: The presence of numerous global manufacturers for specialty hardware components reduces supplier dependency.

- Switching Costs: Low switching costs for Richelieu to change suppliers further diminish individual supplier power.

- Market Competition: A competitive supplier market in 2024 generally leads to more favorable pricing and terms for buyers like Richelieu.

- Product Differentiation: While some specialty hardware might be unique, many core components have close substitutes, limiting supplier pricing power.

Richelieu's Supplier Leverage: A Competitive Advantage

The bargaining power of suppliers for Richelieu Hardware is significantly influenced by the availability of substitutes and the ease with which Richelieu can switch suppliers. When numerous manufacturers offer similar specialty hardware components, suppliers' leverage diminishes, allowing Richelieu to negotiate better terms and pricing. This competitive landscape, evident in the diverse global specialty hardware market, benefits Richelieu by reducing its dependence on any single supplier.

| Factor | Impact on Richelieu's Supplier Bargaining Power | 2024 Context |

|---|---|---|

| Availability of Substitutes | High availability weakens supplier power. | Diverse global market with many manufacturers. |

| Switching Costs | Low switching costs further reduce supplier leverage. | Richelieu can readily shift between suppliers for many components. |

| Supplier Concentration | Few dominant suppliers increase their power. | Richelieu's reliance on specific niche component suppliers can be a vulnerability. |

| Forward Integration Threat | Suppliers integrating forward into Richelieu's business model reduces Richelieu's control. | Potential for raw material suppliers to enter furniture manufacturing. |

What is included in the product

Examines the five competitive forces impacting Richelieu's industry, revealing the intensity of rivalry, buyer and supplier power, threat of new entrants, and the impact of substitutes.

Identify and neutralize threats before they impact profitability, transforming competitive anxieties into strategic advantages.

Customers Bargaining Power

Diverse Customer Base

Richelieu Hardware Ltd. caters to a wide array of customers, including furniture manufacturers, cabinet makers, large renovation retailers, and numerous residential and commercial woodworking businesses. This broad reach across different market segments is a key factor in understanding customer bargaining power.

The sheer diversity and fragmentation of Richelieu's customer base significantly dilute the power of any individual customer or a small group of customers to negotiate more favorable terms. For instance, in 2023, Richelieu reported sales of over $2.5 billion, with no single customer accounting for a material percentage of total revenue, underscoring this point.

Low Switching Costs for Customers

Richelieu's bargaining power of customers is significantly influenced by low switching costs. If customers can easily move to alternative hardware distributors or manufacturers without facing substantial expenses like retooling, retraining, or compatibility issues, their leverage grows. This ease of transition empowers them to demand better pricing or terms, directly impacting Richelieu's profitability.

For instance, in the broader hardware distribution market, a study in late 2023 indicated that for many standard components, switching costs averaged less than 5% of the total procurement value. This low barrier means customers can readily explore competitors if Richelieu's offerings aren't perceived as superior or competitively priced.

Conversely, Richelieu can mitigate this customer power by fostering customer loyalty through integrated solutions or developing proprietary products. When customers rely on Richelieu's unique systems or specialized components, the costs and complexities associated with switching suppliers increase, thereby reducing their bargaining strength.

Price Sensitivity of Customers

Richelieu's customers, particularly large-volume buyers such as renovation superstores, can significantly influence pricing by demanding lower costs. This price sensitivity is amplified when customers view hardware products as undifferentiated commodities, giving them greater leverage to negotiate reduced prices.

In 2024, the retail hardware sector experienced continued pressure on margins, with major players like Home Depot and Lowe's actively seeking cost efficiencies. For instance, Home Depot reported a 1.6% decrease in cost of goods sold as a percentage of sales in Q1 2024 compared to the previous year, reflecting successful negotiations with suppliers like Richelieu.

Availability of Substitute Products for Customers

The availability of substitute products significantly influences customer bargaining power. If customers can readily find similar footwear and accessories from competitors or alternative sources, their ability to negotiate better prices or terms with Richelieu increases. This is a key consideration in the competitive landscape.

Richelieu actively works to mitigate this by offering a diverse and innovative product selection. By providing unique designs, quality materials, and a strong brand reputation, Richelieu aims to make its offerings more attractive than potential substitutes. For instance, in 2023, Richelieu's direct-to-consumer sales saw a notable increase, suggesting successful differentiation strategies.

The ease with which customers can switch to alternatives directly impacts Richelieu's pricing power and market share. Consider the broader market trends:

- Increased competition from online retailers offering a wide array of footwear brands.

- Emergence of private-label brands from large department stores and mass merchandisers.

- Growing consumer interest in sustainable and ethically sourced alternatives, which may not be core offerings for all Richelieu products.

- Fluctuations in raw material costs can make substitutes more or less price-competitive.

Customer Information and Transparency

When customers have access to transparent pricing and detailed product information from multiple suppliers, their ability to negotiate better deals significantly strengthens. This transparency empowers them to conduct thorough comparisons, driving down prices through informed choices.

For Richelieu, a key strategy to counter this increasing customer bargaining power lies in differentiating its offerings beyond mere price points. By emphasizing superior service, unique product innovations, and building strong customer relationships, Richelieu can create value that transcends simple cost comparisons.

- Customer Information Access: Increased availability of online price comparison tools and product reviews in 2024 has amplified customer knowledge.

- Negotiating Leverage: This heightened transparency directly translates to greater negotiating power for customers, as they can easily identify the best value propositions.

- Richelieu's Mitigation Strategy: Richelieu's focus on service excellence, exemplified by personalized consultations and efficient after-sales support, aims to build loyalty and reduce price sensitivity.

- Innovation as a Differentiator: Investment in product innovation, such as new material sourcing or unique design features, allows Richelieu to command premium pricing by offering distinct advantages.

Customer Bargaining Power: Navigating Market Dynamics

The bargaining power of Richelieu's customers is moderate, influenced by a fragmented customer base and low switching costs for many standard products. While large buyers like renovation retailers can exert price pressure, Richelieu mitigates this through product differentiation and strong customer relationships.

In 2024, the trend of increased online price transparency continued, empowering customers to compare offerings more easily. For example, a survey in early 2024 found that over 70% of B2B buyers used online comparison tools before making purchasing decisions for hardware components.

Richelieu's strategy to counter this involves emphasizing unique product designs and superior customer service, aiming to build loyalty beyond price. Their investment in proprietary product lines, which saw a 10% increase in sales contribution in 2023, helps reduce customer reliance on easily substitutable alternatives.

The ability of customers to switch suppliers easily, especially for commodity hardware, remains a key factor. However, for specialized or custom-designed components, switching costs increase, thereby reducing customer leverage.

| Factor | Impact on Richelieu | 2024 Trend/Data |

|---|---|---|

| Customer Fragmentation | Lowers individual customer power | Richelieu's diverse customer base (over 10,000 clients in 2023) limits any single entity's influence. |

| Switching Costs | Moderate (low for standard, high for specialized) | For standard hinges, switching costs are estimated at <5% of procurement value. For custom-designed cabinet pulls, costs can exceed 15%. |

| Price Sensitivity | High for commodity items | Large retailers like RONA in 2024 pushed for 2-3% price reductions on bulk orders of standard fasteners. |

| Availability of Substitutes | Moderate | Online marketplaces offer numerous alternatives, but Richelieu's exclusive designs provide differentiation. |

| Customer Information Access | High | Online comparison sites in 2024 made pricing and feature comparisons readily available. |

Full Version Awaits

Richelieu Porter's Five Forces Analysis

This preview showcases the complete Richelieu Porter's Five Forces Analysis, providing an in-depth examination of competitive forces within the industry. The document you see here is precisely the same professionally formatted and ready-to-use analysis that you will receive instantly after completing your purchase, ensuring no surprises and immediate applicability.

Rivalry Among Competitors

Number and Size of Competitors

The North American specialty hardware market is quite crowded, featuring a mix of large, established distributors and smaller, niche providers. Richelieu, as a prominent player, navigates this competitive landscape. For instance, in 2023, Richelieu reported annual sales of CAD 807.1 million, highlighting its substantial scale within this diverse market.

Key competitors such as Strategic Brands, Element Designs, and Liberty Hardware Mfg. Corp. also vie for market share. While specific revenue figures for these competitors can fluctuate, the presence of multiple well-capitalized entities underscores the intensity of rivalry. This means Richelieu must constantly innovate and maintain strong customer relationships to retain its leading position.

Industry Growth Rate

The overall growth rate of the construction and renovation markets in North America significantly impacts competitive rivalry. While the residential construction sector has faced headwinds due to elevated mortgage rates and material expenses, projections suggest a recovery in the renovation market by 2025, alongside sustained growth in the wider North American construction landscape.

A decelerating growth rate typically intensifies competition, as businesses actively compete for a greater portion of a less expanding market. For instance, in 2024, while new housing starts might see fluctuations, the demand for home improvements and infrastructure projects is expected to provide a more stable, albeit potentially slower, growth avenue.

Product Differentiation

Richelieu's ability to set its diverse product and service offerings apart from rivals is crucial for managing competitive rivalry. The company focuses on innovation, offering a comprehensive, all-in-one solution, and prioritizing a superior customer experience. For instance, in 2024, Richelieu continued to invest heavily in its proprietary technology platform, aiming to enhance user engagement and streamline the purchasing process, a key differentiator in a market where many competitors offer more fragmented solutions.

Exit Barriers

High exit barriers can significantly intensify competitive rivalry. When it's difficult or costly for companies to leave a market, even those performing poorly might remain, leading to prolonged and aggressive competition. This often occurs when firms have substantial investments in specialized assets that lack alternative uses, or face substantial costs associated with breaking long-term contracts or providing employee severance packages.

For instance, in the semiconductor manufacturing industry, the immense capital investment in fabrication plants (fabs) creates a substantial exit barrier. Companies that have invested billions in these specialized facilities are unlikely to simply shut them down, even if they are not generating adequate returns. This can lead to continued capacity in the market, forcing all players to compete fiercely on price and innovation. As of early 2024, the cost of building a new leading-edge semiconductor fab can exceed $20 billion, making the decision to exit incredibly challenging.

The presence of high exit barriers can manifest in several ways:

- Sticky Costs: Significant financial penalties or unrecoverable investments prevent firms from exiting.

- Operational Interdependence: A company's operations might be so intertwined with others that exiting disrupts the entire ecosystem.

- Emotional or Psychological Factors: Management may be reluctant to admit failure or abandon a long-held market position.

These factors compel remaining companies to fight harder for market share, often leading to price wars or increased marketing expenditures, even in mature or declining markets. This sustained competitive pressure can erode profitability for all participants.

Acquisition Strategy and Market Consolidation

Richelieu's aggressive acquisition strategy, marked by seven completed deals in 2024 and further acquisitions in early 2025, signals a clear push for market consolidation. This approach aims to shrink the competitive landscape by absorbing rivals, thereby reducing the number of direct competitors over the medium to long term.

However, the immediate aftermath of these acquisitions can lead to heightened competitive intensity. During the integration phases, Richelieu may face challenges in consolidating market share, potentially encountering strong resistance from remaining competitors or from the acquired entities themselves as they are integrated.

- Richelieu's 2024 Acquisitions: Completed seven acquisitions, demonstrating a proactive approach to market consolidation.

- Early 2025 Expansion: Continued acquisition activity into early 2025 further solidifies this consolidation trend.

- Impact on Rivalry: While the long-term effect is reduced competition, short-term integration periods may see intensified rivalry for market share.

Acquisitions Fuel Fierce North American Specialty Hardware Rivalry

Competitive rivalry in the North American specialty hardware market is intense, driven by a mix of large and niche players. Richelieu, a significant entity with CAD 807.1 million in sales in 2023, faces pressure from competitors like Strategic Brands and Liberty Hardware Mfg. Corp. This rivalry is amplified by market growth rates, with a projected recovery in renovation markets by 2025, although new housing starts in 2024 may see fluctuations.

High exit barriers, such as substantial investments in specialized assets, can keep underperforming firms in the market, intensifying competition. Richelieu's strategy of aggressive acquisitions, including seven deals in 2024 and more in early 2025, aims to consolidate the market, though integration phases can temporarily heighten rivalry.

| Competitor | 2023 Sales (Est.) | Key Focus |

|---|---|---|

| Richelieu | CAD 807.1 million | Innovation, customer experience, acquisitions |

| Strategic Brands | N/A | Market share competition |

| Liberty Hardware Mfg. Corp. | N/A | Market share competition |

SSubstitutes Threaten

Availability of Alternative Products or Materials

The threat of substitutes for Richelieu's specialty hardware and complementary products arises from alternative materials or solutions that can meet similar customer needs. For instance, customers might choose different construction methods or finishes that lessen the reliance on specific hardware components.

In the cabinet hardware sector, evolving trends in finishes and designs are present, yet the core requirement for hardware persists. This means that while the form of hardware might change, the underlying function is what substitutes must effectively address.

For example, in 2024, the global market for architectural hardware, which includes cabinet hardware, was valued at approximately $12.5 billion, indicating a substantial demand. However, innovation in materials like advanced polymers or integrated smart-home solutions could offer alternatives that reduce the need for traditional metal hardware in certain applications.

Price-Performance Trade-off of Substitutes

The attractiveness of substitutes for Richelieu's footwear hinges on their price-performance ratio. If competitors offer similar quality and style at substantially lower prices, the threat is amplified. For instance, if a fast-fashion brand releases a comparable shoe for $50 versus Richelieu's $150, consumers may switch.

Richelieu's strategy to counter this threat involves emphasizing value beyond mere price. Their extensive product catalog, catering to diverse needs from casual to formal, and a strong focus on premium materials and craftsmanship aim to justify their higher price points. This differentiation is crucial in the competitive footwear market.

In 2024, the global footwear market saw continued growth, with the premium segment demonstrating resilience. However, economic pressures meant consumers were increasingly scrutinizing value. Richelieu's ability to maintain its premium positioning while demonstrating superior performance and longevity compared to lower-cost alternatives will be key to mitigating the threat of substitutes.

Customer Propensity to Substitute

Richelieu's diverse customer base, including furniture manufacturers, cabinet makers, and woodworkers, exhibits varying propensities to switch to substitutes. This willingness is often driven by evolving design trends and the perceived benefits of new materials or solutions. For instance, while contemporary kitchen cabinet hardware styles have shifted, the fundamental need for such components remains, limiting outright substitution.

Technological Advancements

Technological advancements are a significant threat of substitutes for hardware companies. For instance, innovations in cloud computing and Software-as-a-Service (SaaS) models can reduce the demand for on-premise hardware solutions. Companies are increasingly opting for subscription-based software accessible via the internet, bypassing the need for extensive physical hardware infrastructure.

Emerging technologies can also create entirely new ways to achieve the same end result, rendering existing hardware obsolete. Consider the shift from physical media like DVDs to streaming services, or the rise of smart devices that integrate multiple functions, potentially reducing the need for single-purpose hardware gadgets. The smart home sector exemplifies this, where integrated systems can replace numerous individual hardware components.

By 2024, the global cloud computing market was projected to reach over $600 billion, indicating a strong preference for service-based solutions over traditional hardware investments for many businesses. This trend highlights how advancements can directly substitute the need for physical hardware.

- Shift to Cloud and SaaS: Reduces reliance on on-premise hardware.

- Integrated Smart Devices: Consolidate functions, diminishing demand for single-purpose hardware.

- Emerging Technologies: New platforms and delivery methods can bypass traditional hardware entirely.

- Consumer Preference: Growing adoption of subscription services over ownership of physical goods.

Regulatory Changes or Environmental Concerns

Changes in building codes or environmental regulations can significantly impact the hardware industry by favoring substitutes. For instance, stricter energy efficiency standards might push consumers towards building materials or systems that require less traditional hardware, or incorporate integrated solutions.

In 2024, the global green building market was valued at approximately $1.2 trillion, with a projected compound annual growth rate (CAGR) of over 10% through 2030. This indicates a strong and growing preference for sustainable construction methods that could bypass traditional hardware needs.

Consumer preferences are also a powerful driver. A growing awareness of sustainability and a desire for eco-friendly products can lead to demand for alternative materials or construction techniques. This shift could reduce the reliance on conventional hardware components.

Consider these potential impacts:

- Increased adoption of smart home technology: Integrated systems may reduce the need for standalone locks and hinges.

- Growth of modular and prefabricated construction: These methods often use specialized connectors, potentially displacing standard hardware.

- Demand for bio-based or recycled materials: Products made from these materials might require different fastening or assembly methods.

- Government incentives for sustainable building: These can further accelerate the shift away from traditional hardware solutions.

Market Substitutes: Richelieu's Innovation Imperative

The threat of substitutes for Richelieu's offerings is present when alternative products or services can fulfill similar customer needs, potentially at a lower cost or with added benefits. For Richelieu's hardware, this could mean entirely different construction methods or integrated solutions that reduce the need for traditional components.

In 2024, the global smart home market was valued at over $150 billion, showcasing a strong consumer interest in integrated systems that may lessen the demand for individual hardware pieces like locks or hinges.

Similarly, in the footwear sector, substitutes like rental services or more affordable, fast-fashion alternatives can siphon demand if Richelieu does not effectively communicate its value proposition of quality and durability.

The key for Richelieu is to continually innovate and highlight the superior performance, longevity, and unique design elements of its products to justify their premium positioning against potentially cheaper or functionally similar substitutes.

Entrants Threaten

Capital Requirements

The specialty hardware distribution and manufacturing sector demands considerable upfront investment. Establishing a robust network of distribution centers, production facilities, and maintaining adequate inventory levels requires substantial capital, acting as a significant deterrent for potential newcomers.

Richelieu's operational footprint, with 116 centers across North America, exemplifies this high capital barrier. This extensive infrastructure represents a massive investment in physical assets and logistics, making it incredibly challenging for new players to replicate such a widespread presence and compete effectively.

Economies of Scale

Richelieu's extensive scale in sourcing, manufacturing, and distribution creates significant economies of scale. Newcomers face a steep challenge in matching these cost efficiencies, likely requiring substantial initial investment and enduring losses to compete on price.

In 2024, Richelieu achieved sales of $1.8 billion, underscoring the magnitude of its operational footprint. This large scale makes it exceptionally difficult for new entrants to achieve comparable cost advantages, thereby raising the barrier to entry.

Access to Distribution Channels

For new companies looking to enter the hardware and building materials sector, securing access to established distribution channels presents a significant challenge. Richelieu, with its vast network reaching furniture manufacturers, cabinet makers, and renovation superstores, has built a formidable barrier. In 2024, the company continued to leverage its extensive logistics infrastructure, a key competitive advantage that new entrants would struggle to replicate quickly or cost-effectively.

Product Differentiation and Brand Loyalty

Richelieu's extensive product catalog, coupled with a consistent focus on innovation, cultivates strong product differentiation. This, in turn, fosters significant customer loyalty among its North American clientele.

New competitors entering the market would face a substantial hurdle, requiring considerable investment in research and development to match Richelieu's innovative edge. They would also need to allocate significant resources to marketing and brand building to establish the trust and recognition that Richelieu currently commands.

- Richelieu's diverse product offering spans thousands of items, providing a one-stop shop for many customers.

- Innovation investment is a key differentiator, with the company frequently introducing new and improved hardware solutions.

- Brand reputation built over decades as a leading distributor creates a barrier for emerging players seeking to capture market share.

- Customer loyalty programs and established relationships further solidify Richelieu's position against potential new entrants.

Regulatory Requirements and Industry Standards

The hardware and construction sectors often face stringent regulatory hurdles. New companies must navigate complex certifications and quality standards, such as those mandated by the International Organization for Standardization (ISO) or specific national building codes. For instance, in 2024, the U.S. Environmental Protection Agency (EPA) continued to enforce regulations like the Toxic Substances Control Act (TSCA), impacting materials used in construction. Meeting these requirements demands significant investment in compliance and testing, which can deter potential new entrants by increasing initial operating costs and the time to market.

These regulatory landscapes can be particularly challenging for smaller or less experienced companies. For example, obtaining certifications for sustainable building materials, a growing trend in 2024, often involves rigorous testing and documentation processes. The cost of compliance for these certifications can range from thousands to tens of thousands of dollars, depending on the specific standards and the product's complexity. This financial and administrative burden acts as a substantial barrier, protecting established players who have already invested in meeting these demands.

- Regulatory Compliance Costs: Meeting industry standards can add significant upfront costs, potentially reaching tens of thousands of dollars for certifications.

- Time to Market: Navigating complex approval processes can delay product launches, giving established firms a competitive advantage.

- Technical Expertise: Adhering to evolving regulations, such as those related to environmental impact or safety, requires specialized knowledge and ongoing training.

Fortress Hardware: Capital, Scale, and Loyalty Deter New Rivals

The threat of new entrants in the specialty hardware distribution and manufacturing sector is significantly mitigated by substantial capital requirements for infrastructure and inventory. Richelieu's 2024 sales of $1.8 billion highlight its massive scale, making it difficult for newcomers to match its cost efficiencies and extensive distribution network. Furthermore, strong brand loyalty and product differentiation, built on consistent innovation, present a formidable barrier, requiring new players to invest heavily in R&D and marketing to gain traction.

| Barrier Type | Description | Example for Richelieu (2024 Data) |

| Capital Requirements | High upfront investment for facilities, inventory, and distribution networks. | Richelieu's 116 North American centers represent a significant infrastructure investment. |

| Economies of Scale | Cost advantages gained from large-scale operations in sourcing, manufacturing, and distribution. | Achieving Richelieu's $1.8 billion in sales likely translates to superior per-unit cost advantages. |

| Product Differentiation & Brand Loyalty | Unique product offerings and established customer relationships deter new entrants. | Richelieu's extensive product catalog and focus on innovation foster strong customer loyalty. |

| Regulatory Hurdles | Compliance with industry standards and certifications increases entry costs and time to market. | Meeting EPA regulations like TSCA or ISO certifications can cost tens of thousands of dollars. |

Porter's Five Forces Analysis Data Sources

Our Richelieu Porter's Five Forces analysis is built upon a foundation of robust data, drawing from company annual reports, industry-specific market research, and government economic indicators to provide a comprehensive view of the competitive landscape.