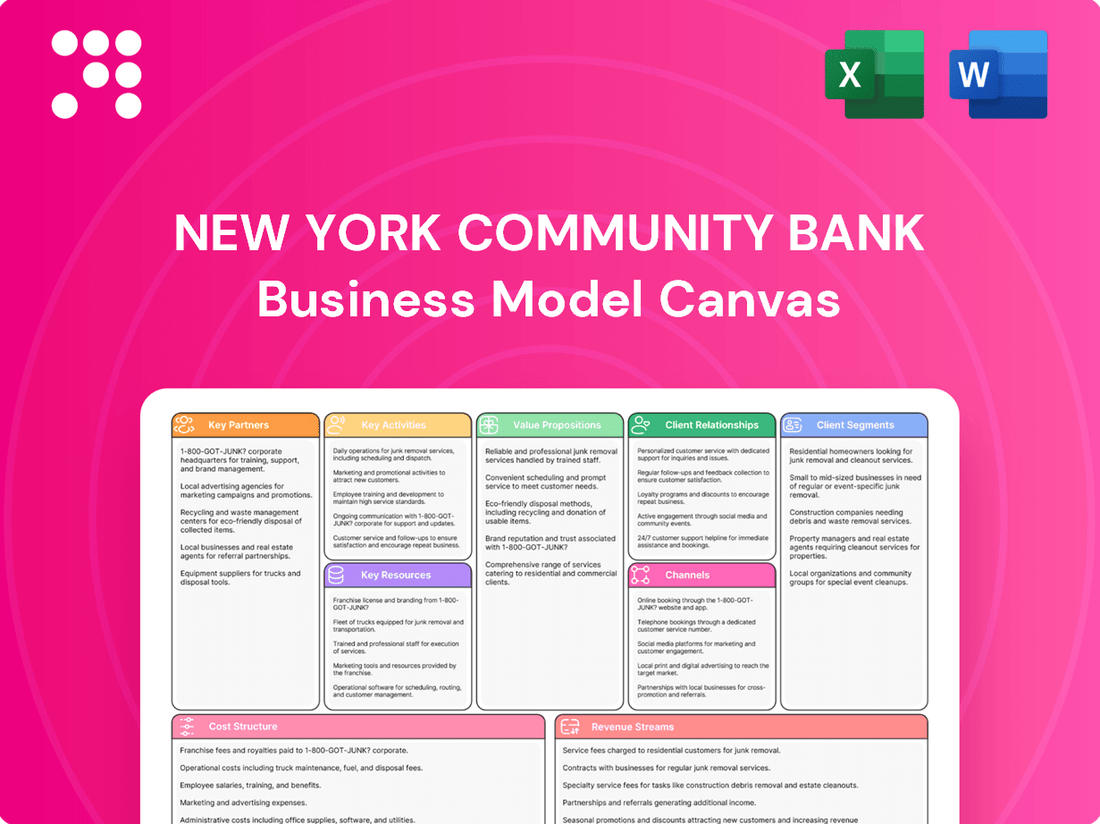

New York Community Bank Business Model Canvas

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

New York Community Bank Bundle

NYCB's Business Model: A Deep Dive

Unlock the strategic blueprint of New York Community Bank's operations with our comprehensive Business Model Canvas. Discover how they build customer relationships, leverage key resources, and generate revenue in the competitive banking sector. This detailed analysis is perfect for anyone looking to understand their success factors.

Partnerships

Strategic Investors and Equity Partners

New York Community Bancorp (NYCB) has recently bolstered its financial position through substantial equity investments, notably a $1 billion infusion led by Liberty Strategic Capital. These strategic partnerships are instrumental in strengthening the bank's capital base and improving its liquidity, especially during periods of transition.

These equity partners provide more than just essential capital; they also bring valuable strategic insights and enhance NYCB's market credibility. Such support is critical for ensuring the bank's stability and paving the way for future expansion and operational improvements.

Financial Technology (Fintech) Collaborations

New York Community Bank (NYCB) strategically partners with fintech firms to boost its digital capabilities and payment systems. These collaborations are crucial for modernizing services and reaching a wider, digitally inclined customer segment.

For example, NYCB has previously explored blockchain technology for trading, signaling a commitment to cutting-edge financial solutions. Such alliances allow the bank to introduce innovative, user-friendly banking experiences.

Government-Sponsored Entities (GSEs)

New York Community Bank's (NYCB) partnerships with Government-Sponsored Entities (GSEs) like Fannie Mae and Freddie Mac are crucial. These collaborations are particularly vital for NYCB's significant presence in mortgage and multi-family lending, especially with its specialization in rent-regulated properties.

These GSE relationships offer NYCB enhanced access to liquidity and a suite of standardized loan products. This access is instrumental in managing its extensive loan portfolio, as GSEs facilitate risk-sharing mechanisms that can mitigate potential losses.

In 2023, the multifamily lending market saw continued activity, with GSEs playing a substantial role. While specific NYCB partnership volumes aren't publicly detailed, the broader market indicates the importance of these channels for institutions like NYCB, which often originate and securitize loans through these entities.

Loan Origination and Servicing Networks

New York Community Bank (NYCB) leverages a robust network of third-party mortgage originators and sub-servicers to amplify its market presence and operational efficiency. This strategic approach, exemplified by Flagstar Mortgage's established wholesale network, enables NYCB to tap into a broader customer base and manage a higher volume of loan originations and servicing. By outsourcing certain functions, NYCB can focus on core competencies while benefiting from the specialized expertise of its partners.

These collaborations are crucial for expanding reach without the need for substantial in-house infrastructure for every stage of the mortgage lifecycle. This partnership model allows for increased market share and the development of diversified revenue streams. For instance, in 2023, Flagstar Bank, a key part of NYCB, reported significant mortgage origination volumes, underscoring the impact of such networks.

- Expanded Origination Channels: Access to a wider pool of borrowers through third-party originators.

- Cost Efficiencies: Reduced overhead by leveraging external servicing capabilities.

- Scalability: Ability to quickly scale loan origination and servicing operations to meet market demand.

- Diversified Revenue: Generating income from both originating and servicing loans facilitated by partners.

Local Community Organizations and Developers

New York Community Bank's strategic focus on multi-family lending, especially within New York City's rent-regulated housing sector, necessitates robust partnerships with local community organizations and property developers. These collaborations are crucial for unlocking access to niche market segments and gaining invaluable insights into the evolving needs of local housing markets.

These alliances help NYCB to better understand and serve the specific housing needs within its core operating regions. For example, by working with community groups, the bank can identify underserved areas or specific demographic needs, allowing for more targeted lending solutions. In 2023, NYCB originated approximately $7.5 billion in multi-family loans, with a significant portion concentrated in the New York metropolitan area, underscoring the importance of these local relationships.

- Community Engagement: Partnerships with organizations like the Community Preservation Corporation (CPC) or local housing advocacy groups provide NYCB with on-the-ground intelligence and a deeper understanding of community development priorities.

- Developer Relationships: Collaborating with experienced property developers, particularly those specializing in affordable or rent-stabilized housing, allows NYCB to participate in projects that align with its lending strategy and community impact goals.

- Market Access: These partnerships serve as a vital channel for identifying and originating loans for multi-family properties, especially those requiring specialized knowledge of local regulations and market dynamics.

Key Partnerships Fuel Lending and Digital Evolution

NYCB's key partnerships extend to financial institutions and government-sponsored entities, crucial for its mortgage and multi-family lending operations. These relationships, including those with Fannie Mae and Freddie Mac, provide access to liquidity and standardized loan products, essential for managing its extensive portfolio. In 2023, the multifamily lending sector remained active, with GSEs playing a significant role, highlighting the importance of these channels for institutions like NYCB.

| Partner Type | Role/Benefit | Example/Context | 2023 Relevance |

|---|---|---|---|

| Equity Investors | Capital infusion, strategic insights, market credibility | Liberty Strategic Capital ($1 billion infusion) | Strengthened capital base and liquidity during transition. |

| Fintech Firms | Digital capabilities, payment systems modernization | Exploration of blockchain technology | Enhancing user experience and reaching digital customers. |

| GSEs (Fannie Mae, Freddie Mac) | Liquidity access, standardized loan products, risk-sharing | Facilitating mortgage and multi-family lending | Integral to managing large loan portfolios in an active market. |

| Third-Party Originators/Sub-servicers | Expanded origination channels, cost efficiencies, scalability | Flagstar Mortgage's wholesale network | Amplified market presence and operational efficiency. |

| Community Organizations/Developers | Niche market access, local market insights, community engagement | Local housing advocacy groups, experienced property developers | Facilitated understanding and targeted solutions for rent-regulated housing. |

What is included in the product

This New York Community Bank Business Model Canvas provides a strategic overview of its customer-centric approach, focusing on community engagement and personalized financial services.

It details key partnerships, revenue streams derived from lending and fee-based services, and the operational structure supporting its branch network and digital offerings.

The New York Community Bank Business Model Canvas acts as a pain point reliever by providing a structured, visual representation of their operations, allowing for clear identification of inefficiencies and opportunities for improvement.

This canvas helps alleviate pain points by offering a concise, one-page snapshot of the bank's value proposition, customer segments, and revenue streams, facilitating targeted problem-solving.

Activities

Multi-Family and Commercial Real Estate Lending

New York Community Bank's core activity centers on originating and managing a substantial portfolio of multi-family and commercial real estate loans. A significant portion of this portfolio is concentrated in rent-regulated properties located within New York City, a key characteristic of their business model.

This involves rigorous credit assessment and underwriting processes to evaluate the viability of each loan. Ongoing portfolio management is crucial for mitigating risks, particularly in light of recent headwinds impacting the commercial real estate (CRE) sector. As of the first quarter of 2024, NYCB reported a total loan portfolio of approximately $57.4 billion, with a notable presence in CRE lending.

The bank has been proactively engaged in reviewing and adjusting its loan book. This strategic recalibration aims to reduce exposure to assets that may be experiencing distress or facing increased risk. For instance, in the first quarter of 2024, NYCB's net charge-offs were reported at $102 million, reflecting some of the challenges in managing this specific loan segment.

Retail and Commercial Banking Services

New York Community Bank's key activities revolve around providing a wide array of banking products and services. This includes essential deposit-taking functions, offering checking and savings accounts, and delivering robust treasury management solutions for businesses.

The bank actively pursues the expansion and diversification of its deposit base. A significant part of this strategy involves leveraging private banking teams to attract and retain a broader range of clients, thereby strengthening its funding sources.

In 2023, New York Community Bancorp reported total deposits of $73.0 billion, a slight decrease from $76.6 billion at the end of 2022, highlighting the ongoing efforts to manage and grow this crucial aspect of their retail and commercial banking operations.

Risk Management and Regulatory Compliance

Risk management and regulatory compliance are paramount for New York Community Bank (NYCB), particularly following recent financial strains and heightened oversight. This includes fortifying internal controls and increasing provisions for potential loan losses. As a Category IV banking organization, NYCB must also meet stricter capital and liquidity requirements.

NYCB has actively reviewed its loan portfolios to identify and rectify any existing weaknesses. These efforts are crucial for maintaining financial stability and trust in the current regulatory environment. For instance, in the first quarter of 2024, NYCB reported a net charge-off ratio of 0.38%, a figure they are working to manage within acceptable parameters.

Digital Platform Development and Management

New York Community Bank's key activities heavily involve the development and ongoing management of its digital banking platforms. This commitment is vital for meeting the evolving needs of today's customers and streamlining internal operations. The bank actively invests in its online banking portal and mobile application to provide a seamless and accessible experience.

Enhancing the digital customer journey is a core focus. This includes not only maintaining existing functionalities but also exploring innovative digital payment solutions and features. A strong digital presence is paramount for attracting and retaining a diverse customer base in the competitive financial landscape.

In 2024, the banking sector saw continued growth in digital adoption. For instance, mobile banking usage often surpasses desktop access, highlighting the importance of user-friendly mobile apps. NYCB's efforts in this area directly support customer acquisition and loyalty.

- Digital Platform Investment: Ongoing financial commitment to building and improving online and mobile banking services.

- Customer Experience Enhancement: Focus on creating intuitive and efficient digital interactions to attract and retain clients.

- Payment Solution Exploration: Investigating and potentially integrating advanced digital payment technologies.

- Operational Efficiency: Leveraging digital tools to streamline internal processes and reduce costs.

Strategic Portfolio Diversification and Asset Sales

New York Community Bank (NYCB) is strategically diversifying its loan book to mitigate risks associated with its traditional concentration in multi-family and commercial real estate. A key element of this strategy involves expanding its commercial and industrial (C&I) lending activities, aiming for a more balanced risk profile.

To further refine its operations and enhance financial flexibility, NYCB is undertaking the sale of non-core assets. This includes divesting its warehouse lending portfolio and its residential mortgage servicing business.

- Loan Portfolio Diversification: NYCB is actively growing its Commercial and Industrial (C&I) lending segment to reduce reliance on real estate-related loans.

- Asset Sales for Liquidity: The bank is selling its warehouse lending portfolio and residential mortgage servicing business to improve its liquidity position.

- Operational Simplification: These divestitures are also intended to streamline NYCB's operations and focus on core banking activities.

- Risk Reduction: By diversifying its assets and shedding non-essential businesses, NYCB aims to lower its overall concentration risk in the market.

NYCB's Core Activities: Loan Portfolio, Diversification, Digital Evolution

New York Community Bank's key activities encompass originating and managing a substantial loan portfolio, with a significant concentration in multi-family and commercial real estate, particularly in New York City. This involves rigorous credit assessment and ongoing portfolio management to mitigate risks, especially in the current CRE environment. As of Q1 2024, NYCB's total loan portfolio stood at approximately $57.4 billion, with a notable portion in CRE lending.

The bank is actively working to diversify its loan book by expanding Commercial and Industrial (C&I) lending and divesting non-core assets like its warehouse lending portfolio and residential mortgage servicing business. These actions are designed to simplify operations, improve liquidity, and reduce overall concentration risk.

Furthermore, NYCB focuses on enhancing its digital banking platforms, investing in online and mobile services to improve customer experience and operational efficiency. This includes exploring innovative digital payment solutions to remain competitive and attract a broader client base.

| Activity | Description | Q1 2024 Data/Context |

|---|---|---|

| Loan Origination & Management | Focus on multi-family and commercial real estate loans, with ongoing risk assessment. | Total Loan Portfolio: ~$57.4 billion. Net Charge-offs: $102 million. Net Charge-off Ratio: 0.38%. |

| Portfolio Diversification & Divestiture | Expanding C&I lending, selling warehouse lending and residential mortgage servicing. | Strategic move to reduce concentration risk and enhance financial flexibility. |

| Digital Platform Development | Investing in online and mobile banking for customer experience and efficiency. | Continued focus on user-friendly digital interfaces and payment solutions. |

Full Version Awaits

Business Model Canvas

The New York Community Bank Business Model Canvas you are previewing is the exact document you will receive upon purchase. This isn't a sample or mockup; it's a direct snapshot of the comprehensive analysis, providing a clear understanding of the bank's strategic framework. You'll gain full access to this same professionally structured and detailed canvas, ready for immediate use.

Resources

Financial Capital and Liquidity

Adequate financial capital, encompassing equity and deposits, forms the bedrock of any bank's operations. New York Community Bank (NYCB) has strategically pursued capital raises and diligently expanded its deposit base, reinforcing its financial resilience and liquidity. These actions are paramount for sustaining lending activities and adhering to stringent regulatory mandates.

NYCB's commitment to bolstering its financial strength is evident in its capital management strategies. For instance, in early 2024, following a period of market volatility, NYCB secured significant capital injections. This bolstered its common equity tier 1 (CET1) ratio, a key measure of a bank's financial health, ensuring it remains well-positioned to absorb potential losses and continue its lending operations.

Maintaining robust liquidity is equally vital, enabling NYCB to meet its obligations, including covering uninsured deposits and supporting day-to-day operations. As of the first quarter of 2024, NYCB reported a strong liquidity coverage ratio (LCR), demonstrating its capacity to manage short-term funding needs effectively and provide confidence to its depositors and the market.

Loan Portfolio (Multi-Family and Commercial Real Estate)

New York Community Bank's loan portfolio, heavily concentrated in multi-family and commercial real estate, especially within the New York City metro area, is a cornerstone of its operations. This portfolio is the primary engine for generating interest income, forming the core of the bank's revenue generation.

As of the first quarter of 2024, the bank reported a substantial loan portfolio, with commercial real estate and multi-family loans comprising a significant portion. For instance, their total loans stood around $50 billion, with a notable concentration in these asset classes, highlighting their importance to the bank's business model.

The performance and stability of this real estate loan portfolio are critical, directly influencing the bank's overall financial health and profitability. Managing the inherent risks associated with these concentrated assets is paramount to sustaining the business.

Human Capital (Experienced Management and Staff)

Skilled and experienced personnel are the bedrock of any financial institution, particularly in specialized areas like lending, risk management, and the rapidly evolving digital banking landscape. NYCB's recent leadership overhaul, which saw the appointment of new executives and board members in 2023 and early 2024, underscores a strategic focus on leveraging this expertise to guide its transformation and tackle current challenges.

The deep banking knowledge held by NYCB's teams, including those in private banking, is crucial for fostering strong customer relationships and ensuring smooth, effective operations. This human capital directly impacts the bank's ability to deliver value and maintain its competitive edge in a dynamic market.

Branch Network and Digital Infrastructure

New York Community Bank (NYCB) leverages its extensive branch network, a key resource for customer engagement and deposit acquisition, alongside a growing digital infrastructure. This dual approach allows for both personalized, in-person service and the convenience demanded by modern banking customers. As of early 2024, NYCB operated over 300 branches, primarily concentrated in the New York metropolitan area, providing a tangible local presence.

The bank's digital platforms are integral to its strategy, offering online and mobile banking services that enhance accessibility and streamline transactions. This digital push is crucial for reaching a broader customer base and improving operational efficiency. NYCB is actively working on integrating the systems of recently acquired banks, such as Flagstar Bank, into a unified platform. This consolidation aims to create a more seamless customer experience and drive cost synergies.

- Branch Network: Over 300 branches as of early 2024, predominantly in the New York region, facilitating direct customer interaction and local market penetration.

- Digital Infrastructure: Robust online and mobile banking services offering convenience and accessibility, supporting a wider customer reach.

- System Integration: Ongoing efforts to unify acquired bank platforms, including Flagstar Bank, to enhance operational efficiency and customer experience.

- Deposit Gathering: Both physical branches and digital channels are critical for attracting and retaining customer deposits, a core component of NYCB's funding strategy.

Brand Reputation and Customer Relationships

New York Community Bank's brand reputation and deep-rooted customer relationships are cornerstones of its business model. These established connections with individuals, families, and businesses across the New York metropolitan area represent significant intangible assets, built over decades of service.

Despite facing recent market headwinds, the bank is strategically focused on leveraging this enduring reputation to stabilize its deposit base. The plan involves actively nurturing existing relationships and cultivating new ones, with a particular emphasis on expanding its private banking segment.

- Established Trust: NYCB's long history in the New York market fosters a sense of trust and reliability among its customer base.

- Deposit Stability: The bank aims to use its strong relationships to retain and attract deposits, a critical funding source.

- Private Banking Growth: A key strategy involves deepening relationships within its private banking division to attract and manage higher-value client assets.

- Reputation Resilience: Efforts are underway to reinforce its brand image and customer loyalty, even amidst industry challenges.

Bank's Core Resources: Capital, Loans, Talent, Network, Trust

New York Community Bank's key resources include its substantial financial capital, a significant loan portfolio concentrated in real estate, a skilled workforce, a widespread branch network complemented by digital platforms, and a strong brand reputation built on decades of customer relationships. These elements collectively enable NYCB to generate revenue, manage risk, and serve its diverse customer base.

| Key Resource | Description | Key Data (as of Q1 2024) |

| Financial Capital | Equity and deposits supporting lending and operations. | CET1 ratio bolstered; strong liquidity coverage ratio (LCR). |

| Loan Portfolio | Primarily multi-family and commercial real estate in NYC metro. | Total loans approx. $50 billion, with significant concentration in CRE/multi-family. |

| Human Capital | Experienced personnel in lending, risk management, and digital banking. | Recent leadership appointments in 2023-2024 to guide transformation. |

| Physical & Digital Infrastructure | Over 300 branches and growing digital services. | Over 300 branches; ongoing integration of Flagstar Bank systems. |

| Brand & Customer Relationships | Established trust and loyalty in the New York market. | Focus on deepening private banking relationships for deposit stability. |

Value Propositions

Specialized Multi-Family Lending Expertise

New York Community Bank (NYCB) leverages its specialized multi-family lending expertise, particularly in the New York City market, as a core value proposition. This deep focus allows them to offer tailored financial solutions and possess an unparalleled understanding of the local real estate landscape, especially for rent-regulated properties.

This specialization positions NYCB as a preferred lender for property owners and developers navigating the complexities of the New York City multi-family sector. Their market-leading position in this niche is a significant differentiator, attracting clients seeking specialized knowledge and reliable financing.

As of the first quarter of 2024, NYCB reported a substantial loan portfolio, with multi-family loans forming a significant portion. This demonstrates their commitment and success in this specialized lending area, reflecting their deep engagement with the market and their clients' needs.

Comprehensive Banking Services for Diverse Needs

New York Community Bank offers a complete suite of commercial and retail banking solutions, designed to meet the diverse financial requirements of individuals, families, and businesses. This comprehensive approach includes essential services like checking and savings accounts, various loan options, and sophisticated treasury management for companies.

By providing this wide array of products, the bank positions itself as a convenient one-stop shop for a broad customer base. This strategy directly supports their objective of operating as a diversified regional bank, ensuring they can serve multiple market segments effectively.

As of the first quarter of 2024, New York Community Bank reported total assets of approximately $117.6 billion, demonstrating its significant scale and capacity to offer extensive banking services across its operational footprint.

Local Market Focus and Community Presence

New York Community Bank (NYCB) leverages its extensive branch network, particularly within the New York City metropolitan area, to foster a strong community presence. This localized approach, with over 200 branches as of early 2024, allows them to deeply understand the unique economic currents and customer requirements of the regions they serve.

This commitment to local markets translates into a more personalized banking experience for customers. By being embedded in the community, NYCB can offer tailored financial solutions and build lasting relationships, differentiating itself from larger, more geographically dispersed institutions.

Accessibility and Convenience through Multi-Channel Banking

New York Community Bank offers customers the flexibility to bank how and when they want, blending the personal touch of physical branches with the ease of digital tools. This means you can pop into a branch for a complex transaction or manage your accounts on the go through their mobile app or website.

This strategy is crucial for meeting diverse customer needs. For instance, in 2023, community banks across the US reported that while digital transactions continued to rise, approximately 60% of customers still utilized physical branches for certain services, highlighting the ongoing importance of a hybrid approach.

- Branch Network: Maintains a physical presence for in-person service and complex needs.

- Digital Platforms: Offers robust online and mobile banking for 24/7 account management.

- Customer Experience: Enhances convenience and accessibility, catering to varied preferences.

- Service Integration: Ensures a seamless transition between physical and digital interactions.

Financial Stability and Prudent Risk Management

New York Community Bank prioritizes financial stability and prudent risk management, offering a core value proposition of security to its customers. Despite facing headwinds, the bank is actively working to fortify its balance sheet and enhance its risk mitigation strategies. This commitment translates into a reliable and trustworthy banking experience, especially during periods of market uncertainty.

This focus on stability aims to reassure depositors and investors alike. For instance, as of the first quarter of 2024, NYCB reported a Common Equity Tier 1 (CET1) ratio of 10.1%, demonstrating a foundational level of capital. The bank's ongoing efforts to manage its loan portfolio and capital structure are designed to ensure its resilience and ability to weather economic fluctuations.

- Enhanced Security: Customers gain peace of mind knowing their deposits are protected by a bank actively strengthening its financial foundation.

- Reliable Operations: The emphasis on risk management ensures consistent and dependable banking services, even amidst market volatility.

- Investor Confidence: A robust balance sheet and sound risk practices attract and retain investors seeking stable financial institutions.

- Navigating Challenges: The bank's commitment to improvement signals a proactive approach to overcoming recent difficulties and building long-term strength.

Unpacking a Bank's Value: Niche Expertise, Local Reach, Digital Access

NYCB's value proposition centers on its deep specialization in multi-family lending, particularly within the dynamic New York City market. This niche expertise allows them to provide tailored financial solutions and a nuanced understanding of complex property types, especially rent-regulated ones.

The bank's extensive branch network, exceeding 200 locations as of early 2024, fosters a strong community presence and enables personalized service. This localized approach allows NYCB to deeply understand regional economic trends and customer needs, differentiating it from larger, less embedded institutions.

NYCB offers a hybrid banking model, seamlessly integrating its physical branch network with robust digital platforms. This caters to diverse customer preferences, providing both in-person support for complex needs and 24/7 accessibility through online and mobile channels, a strategy supported by data showing continued branch utilization alongside digital growth.

Financial stability and prudent risk management form another key value. Despite recent challenges, NYCB is actively fortifying its balance sheet, as evidenced by its Common Equity Tier 1 ratio of 10.1% in Q1 2024, aiming to provide a secure and reliable banking experience for depositors and investors.

| Value Proposition | Key Aspect | Supporting Data (as of Q1 2024) |

|---|---|---|

| Specialized Lending | Multi-family expertise in NYC | Significant portion of loan portfolio dedicated to multi-family properties. |

| Community Presence | Extensive branch network | Over 200 branches, fostering local understanding and relationships. |

| Hybrid Banking | Physical and Digital Integration | Supports varied customer needs with both in-person and online/mobile services. |

| Financial Stability | Risk Management & Capital Strength | CET1 ratio of 10.1%, demonstrating commitment to a fortified balance sheet. |

Customer Relationships

Personalized Relationship Management

New York Community Bank (NYCB) cultivates personalized relationships with key customer segments, particularly multi-family property owners and commercial clients. This approach is often facilitated by dedicated loan officers and private banking teams who deeply understand each client's specific financial requirements.

By offering tailored solutions, NYCB aims to build significant trust and foster enduring loyalty. For instance, in 2023, NYCB's commercial real estate portfolio, a significant area for their multi-family focus, remained robust, demonstrating the bank's commitment to these client relationships.

Branch-Based Service and Local Engagement

New York Community Bank leverages its extensive branch network to foster deep customer relationships through face-to-face interactions. This allows for personalized service and direct engagement, catering to those who value traditional banking. For instance, in 2024, the bank continued to emphasize its community presence, supporting local events and initiatives across its service areas.

Digital Self-Service and Support

New York Community Bank (NYCB) enhances customer relationships through robust digital self-service and support. Their digital platforms allow customers to independently manage accounts, initiate payments, and retrieve essential banking information, offering significant convenience and efficiency. This approach is particularly appealing to their digitally-inclined customer base, providing a seamless complement to their traditional branch services.

Proactive Communication and Transparency

New York Community Bank (NYCB) prioritizes proactive communication and transparency, especially during market turbulence. For instance, following their significant acquisition of Flagstar Bank in 2023, which added $37.4 billion in deposits and $30.5 billion in loans, NYCB focused on clearly communicating the integration process to their customers. This included updates on branch consolidations and system changes, aiming to minimize disruption and maintain confidence.

This commitment to openness helps build and maintain customer trust, a vital component of their customer relationships. By providing clear information regarding financial performance, strategic decisions, and any operational adjustments that might affect their banking, NYCB aims to foster a sense of partnership.

- Clear Updates on Integration: Following the Flagstar acquisition, NYCB provided regular customer communications regarding the merger's progress, including system and branch integration timelines.

- Financial Performance Transparency: NYCB regularly publishes financial reports, allowing customers and stakeholders to understand the bank's health and strategic direction.

- Addressing Customer Concerns: Proactive outreach and accessible communication channels are employed to address customer inquiries and concerns promptly, particularly during periods of change.

- Digital Communication Channels: Leveraging email, secure messaging within online banking, and their website, NYCB ensures information is readily available to a broad customer base.

Advisory and Financial Guidance

New York Community Bank (NYCB) extends its customer relationships beyond basic transactions by offering robust advisory and financial guidance. This is particularly crucial for their business clients and high-net-worth individuals, who benefit from a more personalized, consultative approach.

This strategy aims to foster deeper, more enduring relationships by empowering clients to make sound financial decisions. For instance, in 2024, NYCB continued to emphasize personalized financial planning, with a significant portion of their wealth management clients engaging in regular advisory sessions.

- Personalized Financial Planning: NYCB provides tailored advice to help clients navigate complex financial landscapes, from investment strategies to retirement planning.

- Business Advisory Services: The bank offers guidance on capital management, expansion, and risk mitigation for its corporate clientele.

- Relationship Deepening: By acting as a trusted financial partner, NYCB strengthens customer loyalty and encourages long-term engagement.

- Informed Decision-Making: Clients receive expert insights to make more confident and strategic financial choices.

NYCB: Building Trust, Fostering Loyalty, Empowering Clients

New York Community Bank (NYCB) nurtures customer relationships through dedicated personal bankers and a community-focused branch strategy, fostering trust and loyalty, particularly with multi-family property owners. The bank also enhances these connections via accessible digital platforms, offering convenience for self-service banking.

NYCB prioritizes transparency and proactive communication, especially during significant events like the 2023 Flagstar acquisition, to maintain customer confidence. Furthermore, they provide valuable advisory services, acting as financial partners to clients, which deepened engagement in 2024.

| Relationship Focus | Key Activities | 2023/2024 Data Points |

| Personalized Service | Dedicated loan officers, private banking teams | Flagstar acquisition added $37.4B deposits, $30.5B loans (2023) |

| Community Presence | Branch network, local event support | Continued emphasis on community initiatives (2024) |

| Digital Engagement | Self-service platforms, online account management | Seamless complement to branch services |

| Advisory Services | Financial planning, business guidance | Increased client engagement in advisory sessions (2024) |

Channels

Branch Network

New York Community Bank (NYCB) leverages a significant branch network as a core component of its business model. This network, spanning the New York City metropolitan area, Northeast, Midwest, Southeast, and West Coast, acts as a crucial channel for customer interaction.

These physical locations are central to deposit gathering and providing essential banking services. In 2024, NYCB continued to operate hundreds of branches, serving as vital community hubs for both retail and commercial clients seeking personalized financial assistance.

Digital Banking Platforms (Online and Mobile)

New York Community Bank leverages its digital banking platforms, encompassing both online and mobile applications, as a core component of its customer value proposition. These platforms empower customers with convenient, 24/7 access to manage accounts, execute transactions, and handle bill payments from virtually anywhere.

The emphasis on digital accessibility is crucial for attracting and retaining a modern customer base. In 2024, a significant portion of banking interactions are expected to occur through these digital channels, reflecting a broader industry trend where customer preference for digital self-service continues to grow.

Private Banking Teams

New York Community Bank's private banking teams are crucial for serving high-net-worth individuals and their businesses. These dedicated teams offer specialized services and build personalized relationships, acting as a high-touch channel for affluent clients in key metropolitan areas.

In 2024, the demand for personalized wealth management continues to grow, with many high-net-worth individuals seeking tailored financial solutions beyond standard retail banking. Private banking units are designed to meet this demand by providing expert advice on investments, estate planning, and lending, often managing significant assets for their clientele.

Wholesale Mortgage Network

Flagstar Mortgage, a key component of New York Community Bank's (NYCB) business model, utilizes a national wholesale network to originate residential mortgages. This strategy allows NYCB to tap into a broad market by partnering with third-party mortgage originators, effectively extending its reach without the overhead of a large internal sales team.

This wholesale channel is crucial for NYCB's growth in the mortgage sector. By leveraging these established relationships, the bank can efficiently scale its operations and capture a larger share of the mortgage market. In 2024, the wholesale channel continued to be a significant contributor to the overall mortgage origination volume for many lenders, reflecting its importance in reaching diverse borrower segments.

- National Reach: Flagstar's wholesale network enables NYCB to serve customers across the United States.

- Partnership Leverage: It allows NYCB to grow its mortgage business by utilizing the existing infrastructure and client bases of third-party originators.

- Cost Efficiency: This model reduces the need for extensive in-house sales force management, leading to potentially lower operational costs.

Direct Sales and Loan Officers

New York Community Bank (NYCB) leverages direct sales teams and experienced loan officers as a core channel for its multi-family and commercial real estate lending. These professionals actively cultivate relationships with property owners and developers, which is essential for originating substantial and intricate loan agreements. This personal approach fosters client loyalty and allows for a deeper understanding of borrower needs.

This direct engagement model is particularly vital for NYCB's specialization in large-scale real estate financing. By having dedicated teams who understand the nuances of these complex transactions, the bank can effectively navigate the origination process. For instance, in 2024, NYCB continued to focus on its traditional strength in originating loans for stabilized multi-family properties across key metropolitan areas, where these direct relationships are paramount.

The effectiveness of this channel is reflected in NYCB's ability to secure and service a significant volume of real estate loans. These loan officers act as the primary point of contact, guiding clients through the entire lending lifecycle. This direct interaction facilitates quicker decision-making and tailored financial solutions, reinforcing NYCB's position as a trusted lender in the real estate sector.

- Relationship-Driven Origination: Direct sales teams and loan officers build and maintain strong connections with property owners and developers.

- Complex Loan Expertise: This channel is crucial for originating large and intricate multi-family and commercial real estate loans.

- Client Retention: Direct engagement fosters loyalty and ensures a consistent flow of business from key clients.

- Market Specialization: NYCB's focus on specific real estate segments, like stabilized multi-family properties, relies heavily on this direct outreach.

Multi-Channel Banking: Expanding Reach, Driving Growth

New York Community Bank (NYCB) utilizes a multi-channel approach to reach its diverse customer base. This includes a robust physical branch network, digital platforms, specialized private banking, and a national wholesale mortgage operation. These channels are designed to cater to different customer needs, from everyday banking to complex real estate financing and wealth management.

In 2024, NYCB continued to balance its traditional branch presence with investments in digital capabilities. The wholesale mortgage channel, operated through Flagstar Mortgage, remained a key avenue for expanding its mortgage origination reach nationwide. Direct sales teams are critical for its core multi-family and commercial real estate lending business.

The bank's strategy emphasizes leveraging these channels to foster strong customer relationships and drive growth across its product offerings. This integrated approach allows NYCB to serve a broad spectrum of clients effectively.

Customer Segments

Multi-Family Property Owners and Developers

Multi-family property owners and developers represent a core customer segment for New York Community Bank (NYCB). These clients are primarily focused on the New York City metropolitan area, with a particular emphasis on those managing rent-regulated properties. NYCB offers tailored lending services to support their acquisition, refinancing, and development projects.

In 2024, the multifamily lending market in NYC continued to be robust, though influenced by evolving economic conditions. NYCB's deep understanding of the local market, including the complexities of rent regulation, positions it as a key partner for these property owners. The bank's ability to provide specialized financing solutions is crucial for clients navigating the unique challenges and opportunities within this sector.

Commercial Real Estate Investors and Businesses

New York Community Bank (NYCB) extends its financial reach beyond multi-family housing to cater to a diverse commercial real estate (CRE) investor base. This includes businesses and individuals looking for capital to acquire, develop, or refinance a wide array of commercial properties, from office buildings to retail spaces and industrial facilities. In 2024, the CRE market continued to navigate economic shifts, with interest rates influencing investment strategies and property valuations across different sectors.

Furthermore, NYCB actively supports businesses that require more than just property financing. They offer a suite of commercial loans, including lines of credit and term loans, designed to fuel operational growth, expansion, and working capital needs. This segment also benefits from comprehensive banking services, aiming to be a full-service partner for businesses operating within the dynamic New York metropolitan area and beyond.

Individuals and Families (Retail Customers)

New York Community Bank (NYCB) serves individuals and families through a widespread branch network and robust digital channels, offering essential everyday banking services. These include a variety of checking and savings accounts designed to meet diverse financial needs, alongside personal loans and other retail banking products.

In 2024, NYCB continued to focus on its retail customer base, a core segment for its operations. The bank's strategy involves leveraging its physical presence in key markets, particularly in the New York metropolitan area, to attract and retain individual depositors and borrowers.

High-Net-Worth Individuals and Their Businesses

New York Community Bank’s private banking division actively courts high-net-worth individuals and their businesses, providing bespoke financial strategies, comprehensive wealth management, and highly personalized client service. This clientele demands a level of sophistication and customization that goes beyond standard banking offerings.

This segment is crucial for the bank, as these clients often have complex financial needs, including investment management, estate planning, and specialized lending for their enterprises. For instance, in 2024, the average investable assets managed by private banks for high-net-worth clients often exceed $1 million, with many relationships managing tens or even hundreds of millions.

- Targeted Outreach: Private banking teams engage directly with affluent individuals and business owners, fostering deep relationships.

- Tailored Solutions: Services are customized to meet unique wealth accumulation, preservation, and transfer goals.

- Sophisticated Needs: This segment requires advanced financial products and expert advice for complex personal and business finances.

- Business Integration: The bank also serves the commercial banking needs of the businesses owned by these high-net-worth individuals, creating synergistic opportunities.

Small to Mid-Size Businesses

New York Community Bank (NYCB) serves small to mid-size businesses by offering essential commercial banking services. This includes everything from basic deposit accounts to more complex treasury management solutions. These businesses often look for a banking partner that truly understands the nuances of their local market and can provide straightforward access to capital.

In 2024, the small and mid-sized business sector remained a cornerstone of the US economy, with many actively seeking financing to fuel growth and operational needs. NYCB's offerings are tailored to meet these demands, recognizing that accessibility and local market insight are key differentiators for this segment.

- Deposit Accounts: Providing businesses with secure and efficient ways to manage their cash flow.

- Business Loans: Offering various loan products to support working capital, expansion, and equipment purchases.

- Treasury Management: Delivering tools and services to optimize cash collection, disbursement, and liquidity management.

- Local Market Focus: Emphasizing a deep understanding of the New York metropolitan area's business landscape.

Serving Key Market Segments

New York Community Bank (NYCB) primarily targets multi-family property owners and developers, particularly those with rent-regulated properties in the New York City metropolitan area. They also serve a broader commercial real estate investor base, encompassing various property types. Additionally, NYCB caters to individuals and families through retail banking services and high-net-worth individuals via its private banking division. Small to mid-size businesses also form a key segment, receiving commercial banking services and access to capital.

| Customer Segment | Focus Area | 2024 Relevance |

|---|---|---|

| Multi-family Property Owners & Developers | NYC Metro, Rent-Regulated Properties | Robust market, specialized financing crucial. |

| Commercial Real Estate Investors | Various CRE types (office, retail, industrial) | Navigating economic shifts, interest rate impact. |

| Individuals & Families | Everyday banking, retail products | Core operational base, leveraging physical presence. |

| High-Net-Worth Individuals | Wealth management, bespoke financial strategies | Complex needs, average investable assets >$1M. |

| Small & Mid-Size Businesses | Commercial banking, access to capital | Cornerstone of economy, seeking growth financing. |

Cost Structure

Interest Expense on Deposits and Borrowings

Interest expense on deposits and borrowings is a major cost for New York Community Bank. In the first quarter of 2024, the bank reported $474 million in interest expense, a significant increase from $280 million in the same period of 2023, reflecting higher interest rates.

The bank is actively managing its deposit base to control this cost. For instance, they are focusing on attracting and retaining core deposits while strategically reducing their reliance on more expensive wholesale funding sources.

Provision for Credit Losses

The provision for credit losses is a critical cost for New York Community Bank (NYCB), reflecting its anticipation of potential loan defaults. This expense is particularly relevant given NYCB's significant exposure to multi-family and commercial real estate loans.

In recent times, the bank has substantially ramped up these provisions. For instance, in the first quarter of 2024, NYCB reported a provision for credit losses of $552 million, a stark increase compared to previous periods, directly impacting its net income.

Operating Expenses (Salaries, Benefits, Occupancy)

New York Community Bank's operating expenses, encompassing salaries, benefits, and occupancy costs, represent a significant portion of its cost structure. These are the essential expenditures for maintaining its physical presence and compensating its workforce, the backbone of its service delivery.

In 2024, the bank continued to focus on driving efficiency within these operational areas. Following its acquisition of Flagstar Bancorp, NYCB has been actively pursuing integration and optimization strategies to streamline operations and reduce redundant costs. For instance, in the first quarter of 2024, NYCB reported non-interest expenses of $760 million, reflecting ongoing integration efforts and the costs associated with managing its expanded branch network and employee base.

Technology and Integration Costs

New York Community Bank faces substantial technology and integration costs. These are essential for keeping its digital banking platforms modern and competitive, as well as for smoothly merging the operations of recently acquired banks, notably Flagstar Bank and Signature Bank. These investments directly impact how efficiently the bank can operate and its ability to stand out in the market.

For instance, in 2023, NYCB reported significant technology and integration expenses related to its acquisitions. These costs are critical for unifying disparate systems, enhancing cybersecurity, and rolling out new digital services to customers across a broader network. The bank's strategic focus on digital transformation means these expenditures are ongoing and vital for long-term growth and customer satisfaction.

- Digital Platform Investment: Ongoing spending on upgrading online and mobile banking features to meet evolving customer expectations.

- Acquisition Integration: Costs associated with merging IT infrastructure, core banking systems, and data from Flagstar and Signature Bank acquisitions.

- Cybersecurity Enhancements: Necessary investments to protect sensitive customer data and maintain system integrity against increasing cyber threats.

- Operational Efficiency: Technology spending aimed at streamlining internal processes, reducing manual work, and improving overall service delivery.

Regulatory and Compliance Costs

As a substantial banking institution, New York Community Bank (NYCB) faces significant expenses related to regulatory compliance. These costs are essential for adhering to the complex web of financial regulations and maintaining the trust of depositors and investors. In 2024, the banking sector, in general, continued to see elevated compliance spending, driven by evolving capital requirements and anti-money laundering directives.

NYCB's investment in robust risk management frameworks and sophisticated reporting systems directly contributes to meeting these stringent standards. These expenditures are not merely operational overhead but are critical investments in the bank's stability and long-term viability.

- Increased Compliance Burden: Larger banks like NYCB are subject to more rigorous oversight, demanding greater resources for adherence.

- Risk Management Infrastructure: Significant investment is required in technology and personnel to manage and report on various financial risks effectively.

- Reporting Obligations: Meeting the detailed reporting requirements of regulatory bodies necessitates specialized systems and expertise.

Bank's Q1 2024 Costs Soar: Interest, Credit Losses Lead Expense Surge

Interest expense remains a primary cost driver for New York Community Bank, significantly impacted by prevailing interest rates. In Q1 2024, this expense reached $474 million, a notable jump from $280 million in Q1 2023, highlighting the sensitivity to market conditions.

The bank is strategically managing its funding to mitigate these interest costs, prioritizing stable, lower-cost deposits over more expensive wholesale funding. This approach is crucial for maintaining profitability in a dynamic rate environment.

Provision for credit losses is another substantial cost, reflecting the bank's exposure to real estate loans. In Q1 2024, this provision surged to $552 million, a significant increase that directly impacts the bank's earnings.

Operating expenses, including salaries, benefits, and occupancy, are essential for the bank's functioning. Following the Flagstar acquisition, NYCB reported $760 million in non-interest expenses in Q1 2024, reflecting integration efforts and expanded operational scale.

| Cost Category | Q1 2024 (Millions) | Q1 2023 (Millions) | Key Drivers |

| Interest Expense | $474 | $280 | Higher interest rates, deposit mix |

| Provision for Credit Losses | $552 | (Not specified, but significant increase) | Real estate loan portfolio, economic outlook |

| Non-Interest Expense | $760 | (Not specified, but reflects integration) | Salaries, benefits, occupancy, acquisition integration |

Revenue Streams

Net Interest Income from Loans

New York Community Bank's primary revenue driver is net interest income, largely derived from its extensive loan portfolio. This income represents the spread between the interest the bank earns on its loans and the interest it pays out on customer deposits and other borrowings. In 2024, the bank's focus on multi-family and commercial real estate lending continues to be a significant contributor to this core revenue stream.

Fees and Service Charges

New York Community Bank (NYCB) generates significant revenue through a variety of fees and service charges. These charges are applied to both retail and commercial banking products, covering everything from basic account maintenance to transactional activities.

For instance, account maintenance fees, overdraft fees, and wire transfer charges contribute to the bank's fee income. In 2023, NYCB reported non-interest income, which includes these fees, totaling $1.2 billion. This highlights the substantial role of service charges in their overall revenue mix.

Mortgage Origination and Servicing Fees

New York Community Bank's revenue historically included significant income from mortgage origination and servicing fees. Even as the bank has adjusted its mortgage portfolio, these fee-based activities represent a consistent revenue stream, generating income from both creating new loans and managing existing ones for other entities.

In 2023, while specific figures for mortgage origination and servicing fees as a standalone segment are not readily available due to the bank's evolving structure, the overall mortgage lending activity contributes to this revenue. For context, in the first quarter of 2024, New York Community Bank reported a net interest margin of 2.45%, indicating the core profitability of its lending operations, which include mortgage activities.

Specialty Finance and Other Commercial Services

New York Community Bank (NYCB) diversifies its revenue beyond core real estate lending through specialty finance and other commercial services. This includes areas like equipment financing, asset-based lending, and treasury management services, which generate fee-based income and interest income from a broader client base.

For instance, in the first quarter of 2024, NYCB reported total revenue of $340 million. While specific breakdowns for specialty finance are not always granularly detailed in quarterly reports, these ancillary services contribute significantly to the bank's overall financial performance and stability by reducing reliance on any single lending segment.

Key revenue drivers within these commercial services include:

- Treasury Management Fees: Income generated from services like cash management, payment processing, and fraud prevention for business clients.

- Commercial Lending Income: Interest and fees earned from specialty loans such as equipment financing and asset-based lending, supporting diverse business needs.

- Other Fee Income: Revenue derived from various commercial banking activities, including account maintenance and transaction processing.

Investment Income

New York Community Bank's investment income is a key revenue stream, generated primarily from its portfolio of investment securities. This includes earnings from interest on bonds and dividends from stocks held by the bank. For instance, in the first quarter of 2024, the bank reported net interest income of $464 million, reflecting the yield on its asset portfolio.

The bank actively manages its investment securities to generate returns, which are crucial for its profitability. These investments can include U.S. Treasury securities, corporate bonds, and mortgage-backed securities. The performance of these assets directly impacts the bank's overall financial health and its ability to fund operations and provide services.

- Interest Income: Earnings from debt securities like bonds and loans.

- Dividend Income: Payments received from owning stocks in other companies.

- Capital Gains: Profits realized from selling investment securities at a higher price than their purchase cost.

Bank's Revenue: A Detailed Breakdown

New York Community Bank's revenue streams are multifaceted, with net interest income from its substantial loan portfolio, particularly in multi-family and commercial real estate, forming the bedrock.

Fee and service charges on both retail and commercial accounts, alongside income from mortgage origination and servicing, further diversify its earnings.

Specialty finance, treasury management, and investment income from its securities portfolio also contribute significantly, creating a robust revenue model.

| Revenue Stream | Description | 2023/2024 Data Point |

|---|---|---|

| Net Interest Income | Interest earned on loans minus interest paid on deposits. | Q1 2024 Net Interest Margin: 2.45% |

| Fee and Service Charges | Income from account maintenance, overdrafts, wire transfers, etc. | 2023 Non-Interest Income: $1.2 billion |

| Mortgage Origination & Servicing | Fees from creating and managing mortgage loans. | Contributes to overall lending activity; Q1 2024 Net Interest Income: $464 million |

| Specialty Finance & Other Commercial Services | Income from equipment financing, asset-based lending, treasury management. | Q1 2024 Total Revenue: $340 million |

| Investment Income | Earnings from interest on bonds and dividends from stocks. | Reflected in Net Interest Income; includes interest on U.S. Treasuries, corporate bonds. |

Business Model Canvas Data Sources

The New York Community Bank Business Model Canvas is informed by a blend of internal financial statements, regulatory filings, and customer transaction data. This ensures a data-driven approach to understanding revenue streams, cost structures, and customer relationships.