Chang Hwa Bank Boston Consulting Group Matrix

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Chang Hwa Bank Bundle

Visual. Strategic. Downloadable.

Curious about Chang Hwa Bank's strategic positioning? This glimpse into their BCG Matrix reveals how their products stack up as Stars, Cash Cows, Dogs, or Question Marks. Don't miss out on the full analysis that unlocks actionable insights for optimizing your investment portfolio.

Ready to make informed decisions about Chang Hwa Bank's product lines? The complete BCG Matrix provides a detailed breakdown of each quadrant, offering data-driven recommendations to guide your capital allocation and product development strategies. Purchase the full report to gain a competitive edge.

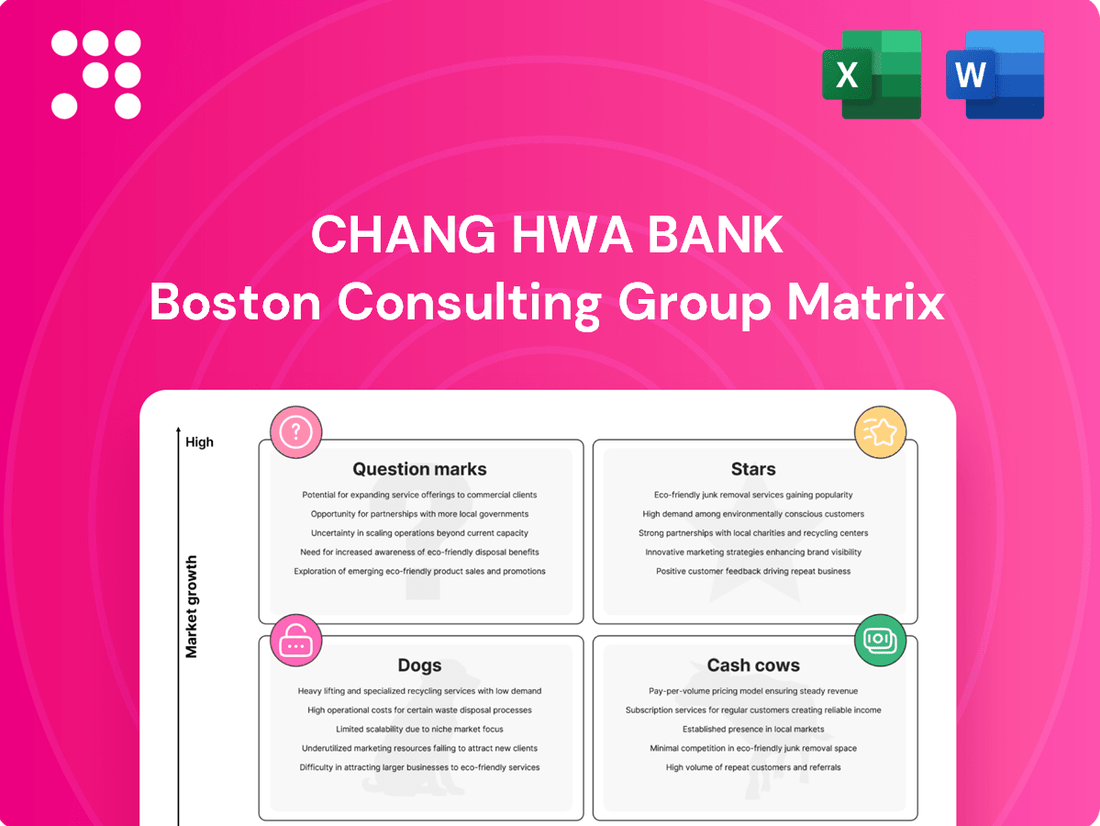

Stars

Overseas Business Expansion

Chang Hwa Bank is strategically expanding its overseas business, aiming to significantly boost profits from international operations. The bank is establishing new branches in important financial centers such as Sydney, Toronto, and Malaysia. This expansion builds upon its established presence in Hong Kong, the United States, and the United Kingdom.

Corporate Lending to AI and High-Performance Computing Sectors

Taiwan's economy is seeing strong growth, with AI and high-performance computing leading the charge. This surge is boosting exports and private investment, creating a fertile ground for financial institutions. Chang Hwa Bank's strategic focus on financing these booming sectors is a smart move to secure a significant market share.

In 2024, Taiwan's export growth, heavily influenced by the semiconductor and AI industries, is projected to be robust. Chang Hwa Bank's commitment to funding these high-growth areas, including those focused on intelligent and low-carbon operations, directly taps into this economic momentum, positioning the bank for substantial revenue generation from this dynamic segment.

Digital Transformation and Fintech Innovation

Chang Hwa Bank is aggressively pursuing digital transformation, pouring resources into FinTech innovations like its 'Bank 4.0' initiative. This includes deploying advanced smart teller machines and leveraging big data for precise customer targeting, aiming to boost efficiency and customer satisfaction in the digital age.

The bank's strategic focus on online loan platforms and mobile payment solutions underscores its ambition to lead in the evolving digital banking sector. For instance, by the end of 2023, Chang Hwa Bank reported a significant increase in digital transaction volumes, reflecting the success of these investments.

Sustainable Finance and Green Initiatives

Chang Hwa Bank is making significant strides in sustainable finance, notably being the first state-owned bank in Taiwan to establish carbon reduction targets validated by the Science Based Targets initiative (SBTi). This commitment positions them as a leader in the burgeoning green finance sector.

The bank's engagement in green loans, green deposits, and financing for renewable energy projects reflects a strategic focus on high-growth markets. These areas are experiencing substantial expansion due to global and national net-zero emission policies. For instance, the global green bond market saw issuance reach approximately $580 billion in 2023, indicating strong investor demand for sustainable investments.

- Commitment to SBTi: Chang Hwa Bank is the first state-owned bank in Taiwan to adopt SBTi-aligned carbon reduction goals, demonstrating a serious dedication to environmental responsibility.

- Green Product Offerings: The bank actively provides green loans, green deposits, and finances renewable energy projects, tapping into a rapidly expanding market.

- Market Opportunity: This proactive ESG strategy not only aligns with global trends but also creates new avenues for business growth and strengthens the bank's public image.

- Growth in Green Finance: The global sustainable finance market continues to expand, with assets under management in ESG funds reaching over $3.4 trillion by the end of 2023, highlighting the commercial viability of these initiatives.

Wealth Management for High-Asset Customers

Chang Hwa Bank is strategically positioning itself within the burgeoning wealth management sector for high-asset customers, a segment recently greenlit for expansion by Taiwan's Financial Supervisory Commission (FSC). This move aligns with the bank's commitment to bolstering its core wealth management operations through the introduction of sophisticated and varied financial products. The bank is also prioritizing the development of specialized wealth management expertise to cater to this affluent demographic.

The bank's focus on high-net-worth individuals represents a significant opportunity for growth and enhanced profitability. As of late 2024, the high-net-worth individual (HNWI) population in Taiwan continues to expand, with wealth management services expected to see substantial demand. Chang Hwa Bank aims to capture a larger share of this lucrative market by offering tailored solutions.

- Growing Market Segment: The FSC's approval allows banks like Chang Hwa Bank to tap into the increasing number of high-asset customers in Taiwan.

- Product Diversification: Chang Hwa Bank is enhancing its wealth management offerings with a range of innovative financial products.

- Talent Cultivation: The bank is investing in developing high-level wealth management talent to provide expert advisory services.

- Profitability Potential: Targeting high-net-worth individuals offers higher profit margins and significant growth prospects for the bank.

Bank's Digital Leap: A Star in the Making

Chang Hwa Bank's strategic focus on digital transformation, particularly its 'Bank 4.0' initiative, positions it as a potential Star in the BCG matrix. By investing heavily in FinTech and advanced customer engagement tools, the bank is creating a highly efficient and customer-centric digital banking experience. This forward-thinking approach is crucial for capturing market share in an increasingly digital financial landscape.

The bank's aggressive pursuit of online loan platforms and mobile payment solutions is a key indicator of its Star status. These digital offerings are not only enhancing operational efficiency but also driving significant growth in transaction volumes. For example, Chang Hwa Bank saw a substantial increase in digital transaction volumes by the end of 2023, demonstrating the success of its digital investments.

Chang Hwa Bank's commitment to innovation in digital banking, including the deployment of smart ATMs and data-driven customer targeting, is a strong foundation for its Star positioning. This focus on cutting-edge technology and customer convenience is vital for maintaining a competitive edge and achieving sustained growth in the evolving financial sector.

The bank's proactive approach to digital banking, evident in its 'Bank 4.0' initiative and increased digital transaction volumes by the end of 2023, solidifies its position as a Star. This strategic emphasis on technology and customer experience is driving significant growth and market relevance.

What is included in the product

This BCG Matrix overview for Chang Hwa Bank highlights strategic recommendations for its business units.

It provides clear insights on which units to invest in, hold, or divest based on market share and growth.

A clear BCG Matrix visualizes Chang Hwa Bank's portfolio, simplifying strategic decisions and alleviating the pain of resource allocation confusion.

Cash Cows

Traditional Deposit and Loan Business

Chang Hwa Bank's traditional deposit and loan operations are its bedrock, holding a strong position in a well-established market. This segment consistently generates reliable income with minimal need for extensive marketing spend.

In 2024, the bank saw robust growth driven by its focus on expanding its deposit base and achieving steady loan expansion. Corporate lending and mortgage financing were particularly strong contributors to this performance.

Fee Income from Insurance Agency and Trust Business

Fee income from Chang Hwa Bank's insurance agency and trust business has been a consistent performer. In 2024, these segments continued to demonstrate robust growth, reflecting a stable and high-margin revenue stream. This success is attributed to the bank's strategic focus on these mature market services, which demand less capital investment compared to other banking operations, thereby boosting overall profitability and cash generation.

Stable Asset Quality and Strong Capitalization

Chang Hwa Bank's asset quality is remarkably stable, evidenced by a consistently low non-performing loan ratio, which stood at a mere 0.15% as of the first quarter of 2024. This low ratio, coupled with strong capital adequacy ratios, including a Common Equity Tier 1 (CET1) ratio of 13.5% at the end of 2023, demonstrates the bank's resilience and ability to generate dependable profits.

This robust financial health translates into consistent cash flow generation, a hallmark of a cash cow. The bank's prudent capital management and ample loan loss reserves, which covered 760% of its non-performing loans in early 2024, provide a solid foundation that supports its ongoing operations and allows for strategic allocation of resources to other business areas.

Government Bonds and Fixed Income Investments

Chang Hwa Bank strategically bolsters its position in government bonds and other fixed-income instruments, aiming to grow its fixed-income portfolio. This measured investment strategy is designed to generate consistent and predictable earnings, thereby supporting the bank's overall cash flow, particularly within a mature market characterized by slower growth.

These fixed-income assets are recognized for their reliability and low-risk profile, acting as dependable income streams. For instance, in 2024, the global government bond market saw significant activity, with yields fluctuating based on central bank policies and inflation concerns. Chang Hwa Bank's focus here aligns with a prudent approach to capital preservation and steady income generation.

- Stable Income Generation: Government bonds and fixed-income investments offer predictable coupon payments, contributing to a consistent revenue stream for Chang Hwa Bank.

- Low Risk Profile: These assets are generally considered low-risk, especially those issued by stable governments, minimizing potential capital losses.

- Portfolio Diversification: Including fixed income helps diversify Chang Hwa Bank's investment portfolio, reducing overall risk exposure.

- Market Performance (Illustrative 2024 Data): As of late 2024, yields on many developed market government bonds remained attractive, offering a solid base for income-focused strategies. For example, US Treasury yields experienced volatility throughout the year, influenced by inflation data and Federal Reserve actions, but generally provided competitive returns for conservative investors.

Established Branch Network and Domestic Market Position

Chang Hwa Bank's established branch network and strong domestic market position are key strengths, classifying it as a Cash Cow. This extensive physical presence across Taiwan, coupled with deep-rooted brand recognition, translates into a stable and loyal customer base for its core banking services. The bank's long history has solidified its significant market share within the Taiwanese banking sector, ensuring consistent revenue streams.

This robust domestic standing is supported by tangible metrics. As of the first quarter of 2024, Chang Hwa Bank reported total assets of NT$2.33 trillion (approximately US$71.7 billion). Its net interest income for the same period was NT$17.3 billion, demonstrating the reliable income generated from its established customer relationships and lending activities.

- Extensive Branch Network: Chang Hwa Bank operates over 170 branches throughout Taiwan, providing convenient access for a broad customer base.

- Dominant Domestic Market Share: The bank consistently ranks among the top Taiwanese banks in terms of deposits and loans, reflecting its strong market penetration.

- Stable Revenue Generation: Its established position ensures a predictable and consistent flow of revenue from traditional banking operations, including interest income and fees.

- Brand Recognition and Trust: Decades of operation have built significant brand loyalty and trust, which are crucial for retaining customers in a competitive market.

Stable Revenue Streams: The Bank's Cash Cow Segments

Chang Hwa Bank's core deposit and loan operations, alongside its fee-generating insurance and trust businesses, represent its stable Cash Cow segments. These areas benefit from a strong, established market position and a loyal customer base, ensuring consistent revenue generation with relatively low investment needs. The bank's robust financial health, characterized by low non-performing loans and strong capital adequacy, further solidifies these segments as reliable cash generators.

| Segment | 2024 Performance Highlight | Key Characteristic |

|---|---|---|

| Deposit & Loan Operations | Robust growth in deposits and steady loan expansion, particularly in corporate lending and mortgages. | Bedrock of reliable income, minimal marketing spend required. |

| Insurance Agency & Trust | Continued robust growth, reflecting a stable and high-margin revenue stream. | Mature market services, less capital intensive, boosting profitability. |

| Fixed-Income Investments | Strategic growth in government bonds and fixed-income portfolio for predictable earnings. | Reliable, low-risk income streams supporting overall cash flow. |

What You’re Viewing Is Included

Chang Hwa Bank BCG Matrix

The Chang Hwa Bank BCG Matrix preview you are currently viewing is the complete and final document you will receive upon purchase. This means no watermarks or demo content will be present; you'll get the fully formatted, analysis-ready report for immediate strategic application.

This preview accurately represents the Chang Hwa Bank BCG Matrix report you will download after completing your purchase. It's a professionally crafted document, designed for clarity and strategic insight, and will be delivered to you without any alterations or hidden elements.

What you see here is the actual Chang Hwa Bank BCG Matrix file you’ll obtain once you make your purchase. The full version is immediately available for editing, printing, or incorporating into your business presentations, offering a comprehensive overview of the bank's portfolio.

Dogs

Declining New Mortgage Lending

Chang Hwa Bank's new mortgage lending segment is a clear Dog in its BCG Matrix. In Q1 2025, new mortgage originations saw a sharp 15% year-over-year decrease, a direct consequence of the central bank's tightened lending policies aimed at curbing property speculation. This downturn reflects a market with limited growth potential and increasing regulatory headwinds, making it a challenging area for the bank.

Traditional, Less Differentiated Products

Certain traditional banking products at Chang Hwa Bank, like basic savings accounts or standard checking accounts, are experiencing intense competition. The market for these offerings is mature, meaning growth is slow, and many banks provide very similar services. This makes it hard for Chang Hwa Bank to stand out, potentially leading to a decline in their market share for these products.

Without significant innovation or unique features, these traditional products could become cash cows that are just breaking even or even draining resources. For example, while deposit growth for Taiwanese banks in 2023 was around 5-6%, the profit margins on these basic deposit products are often thin due to increased funding costs and regulatory requirements.

Underperforming Physical Branches in Declining Areas

While Chang Hwa Bank's extensive branch network is a significant asset, certain physical locations are struggling. Branches situated in areas experiencing economic downturns or population decline, such as some rural towns in Taiwan, are showing reduced customer growth and transaction volumes. For instance, data from the Directorate-General of Budget, Accounting and Statistics (DGBAS) for 2024 indicates continued population outflow from several smaller municipalities.

These underperforming branches can become what are known as cash traps. They still require ongoing operational expenses for maintenance and staffing, but their revenue generation is minimal, especially when compared to the bank's more successful digital channels or branches in thriving urban centers. This situation drains resources that could be better allocated to more profitable areas of the business.

Credit Card Operations with High Delinquency Ratios

Credit card portfolios within Chang Hwa Bank that show elevated delinquency rates and sluggish growth in active users might be classified as Dogs.

These segments, despite the general profitability of credit cards, could represent areas with low market penetration and rising credit risk. Such portfolios might demand significant resources for collections and risk management, thereby diverting capital from more promising ventures.

- High Delinquency Ratios: For instance, if a specific credit card product line sees its delinquency ratio climb to 6.5% in 2024, significantly above the industry average of 3.8%, it signals potential trouble.

- Stagnant Growth: A portfolio experiencing less than 1% annual growth in active cardholders, while competitors see 5% or more, indicates a lack of market traction.

- Resource Drain: Increased provisions for bad debts, estimated at NT$500 million for such segments in 2024, would directly impact profitability.

- Low Market Share: If these underperforming portfolios hold less than 2% of the total credit card market share, their contribution to overall revenue is minimal.

Legacy IT Systems and Infrastructure

Legacy IT systems and infrastructure at Chang Hwa Bank, while functional, represent a significant challenge. These systems, often built on older technologies, require substantial ongoing maintenance and upgrades. For instance, many core banking systems still rely on COBOL, a programming language developed in the late 1950s, which can be costly to maintain and difficult to find skilled personnel for. This drains resources that could otherwise be allocated to developing innovative digital services or enhancing customer experience.

These outdated systems often lack the flexibility to integrate with modern fintech solutions or support the rapid development of new products and services. This inability to adapt quickly can lead to a competitive disadvantage as newer, more agile banks leverage advanced technologies. For example, the inability to seamlessly integrate with open banking APIs or offer real-time payment processing can alienate customers accustomed to faster, more convenient digital interactions.

Consequently, these legacy IT assets can be categorized as Dogs in the BCG matrix. They consume capital without generating significant returns or driving market share growth. In 2023, global IT spending by financial institutions reached approximately $600 billion, with a notable portion dedicated to maintaining existing infrastructure rather than innovation. Chang Hwa Bank must strategically address these legacy systems to free up capital and resources for future growth initiatives.

- High Maintenance Costs: Older systems often incur higher operational and support expenses due to specialized hardware and software requirements.

- Lack of Agility: Inflexibility hinders the bank's ability to quickly adapt to market changes and customer demands.

- Limited Innovation Support: Legacy infrastructure can impede the development and deployment of new digital banking features and services.

- Resource Drain: Capital and skilled personnel are tied up in maintaining these systems, diverting focus from strategic growth areas.

Bank's "Dogs": Underperforming Segments Identified

Chang Hwa Bank's mortgage lending, certain basic deposit accounts, underperforming branches, specific credit card portfolios with high delinquencies, and legacy IT systems all exhibit characteristics of Dogs in the BCG Matrix. These segments typically operate in low-growth markets, face intense competition, or require substantial resources for maintenance without generating commensurate returns. For instance, while the overall Taiwanese banking sector saw deposit growth around 5-6% in 2023, the profitability of basic accounts is often squeezed by rising funding costs. Similarly, a credit card portfolio with a delinquency ratio of 6.5% in 2024, far above the industry average of 3.8%, signals a Dog. These areas drain capital and attention, hindering the bank's ability to invest in more promising ventures.

Question Marks

Emerging Fintech Applications (e.g., Blockchain in Trade Finance)

Chang Hwa Bank is actively exploring emerging fintech applications, notably blockchain technology for trade finance. This includes areas like supply chain financing and electronic letters of credit, which are considered high-growth potential markets. However, the bank's current market share in these nascent areas is relatively low.

These innovative initiatives demand substantial investment in technology and a concerted effort to drive market adoption. The success of these ventures is contingent on widespread acceptance and integration, positioning them as question marks within the BCG matrix due to their uncertain outcomes and future potential.

Expansion into New Overseas Markets (e.g., Sydney, Toronto, Malaysia)

Chang Hwa Bank's expansion into Sydney, Toronto, and Malaysia positions these ventures as potential Stars or Question Marks in its BCG Matrix. These moves represent a high-growth strategy, aiming to capture new market share in promising overseas locations. For instance, the Australian banking sector, where Sydney is located, saw its total assets reach approximately AUD 6.5 trillion in 2023, indicating substantial growth potential.

However, the bank's current market penetration in these new territories is minimal, requiring substantial capital investment for establishing branches, marketing, and regulatory compliance. This initial low market share coupled with high investment needs is characteristic of Question Marks, where success is uncertain but the potential for high returns exists if they can gain traction.

AI-driven Personalized Banking Services

Chang Hwa Bank's AI-driven personalized banking services, focusing on mobile app recommendations and targeted marketing, represent a significant investment in a high-growth digital banking sector. While these initiatives are crucial for future market share, their ultimate impact is still being measured, placing them in the Stars category, demanding ongoing development to solidify their position.

Targeted Lending for Green Energy and Emerging Industries

Chang Hwa Bank's targeted lending for green energy and emerging industries, while part of the broader sustainable finance 'Star' category, often presents as a 'Question Mark' in its early stages. These initiatives, such as financing for advanced battery storage solutions or novel bio-manufacturing processes, may have a small current market share but are poised for significant growth as these sectors mature.

Developing these specialized lending programs requires substantial upfront investment in expertise for evaluating complex technologies and assessing unique market risks. For instance, a new program launched in 2024 to support offshore wind farm development might initially have limited uptake due to project lead times and regulatory hurdles, yet it taps into a sector projected for substantial expansion.

- Low Market Share, High Growth Potential: Programs targeting nascent green tech, like hydrogen fuel cell manufacturing, might have minimal current lending volume but are positioned in rapidly expanding markets.

- High Investment Needs: Significant capital is needed for specialized risk assessment teams and technological due diligence for projects in areas such as carbon capture or sustainable aviation fuels.

- Strategic Importance: These 'Question Marks' are crucial for Chang Hwa Bank to build a future competitive advantage in the evolving landscape of sustainable finance.

Development of New Digital-Only Products/Services

Chang Hwa Bank's focus on developing new digital-only products and services, such as its online loan financing platforms, positions it within the "Question Marks" category of the BCG Matrix. These offerings tap into a high-growth digital market, reflecting the increasing demand for convenient financial solutions.

The bank's strategy involves creating a unique financial ecosystem by collaborating with various industries. This multi-industry cooperation aims to broaden the appeal and utility of its digital products, fostering user adoption and potentially capturing a larger market share over time. For instance, by mid-2024, digital banking adoption in Taiwan was reported to be steadily increasing, with a significant portion of the population actively using mobile banking services for transactions and loan applications.

- High Growth Potential: The digital financial services sector in Taiwan is experiencing robust growth, driven by increasing internet penetration and smartphone usage, creating a fertile ground for new digital products.

- Low Market Share: Despite the market's potential, Chang Hwa Bank's new digital-only offerings currently hold a relatively small share, necessitating significant investment in marketing and user acquisition.

- Strategic Importance: The development of these products is crucial for the bank's long-term competitiveness, allowing it to adapt to evolving customer preferences and technological advancements.

- Investment Requirement: Substantial marketing efforts and user incentives are required to drive adoption and build a strong user base for these nascent digital services.

Bank's High-Growth, Low-Share Bets: Question Marks

Chang Hwa Bank's ventures into emerging fintech, such as blockchain for trade finance, and its expansion into new international markets like Sydney and Toronto, are classic examples of Question Marks. These initiatives are characterized by their high growth potential but currently low market share, demanding significant investment. The bank's foray into AI-driven personalized banking and specialized lending for green energy also fall into this category during their initial phases, requiring careful nurturing to become future Stars.

| Venture Area | Market Growth | Market Share | Investment Needs | BCG Category |

|---|---|---|---|---|

| Fintech (Blockchain) | High | Low | High | Question Mark |

| International Expansion (Sydney) | High (AUD 6.5T total assets in Australian banking sector 2023) | Minimal | High | Question Mark |

| AI Personalized Banking | High | Developing | High | Question Mark (early stages) |

| Green Energy Lending | High | Low | High | Question Mark |

| Digital-Only Products | High (increasing digital banking adoption in Taiwan mid-2024) | Low | High | Question Mark |

BCG Matrix Data Sources

Our Chang Hwa Bank BCG Matrix is built on verified market intelligence, combining financial data, industry research, official reports, and expert commentary to ensure reliable, high-impact insights.