Community Bank Boston Consulting Group Matrix

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Community Bank Bundle

See the Bigger Picture

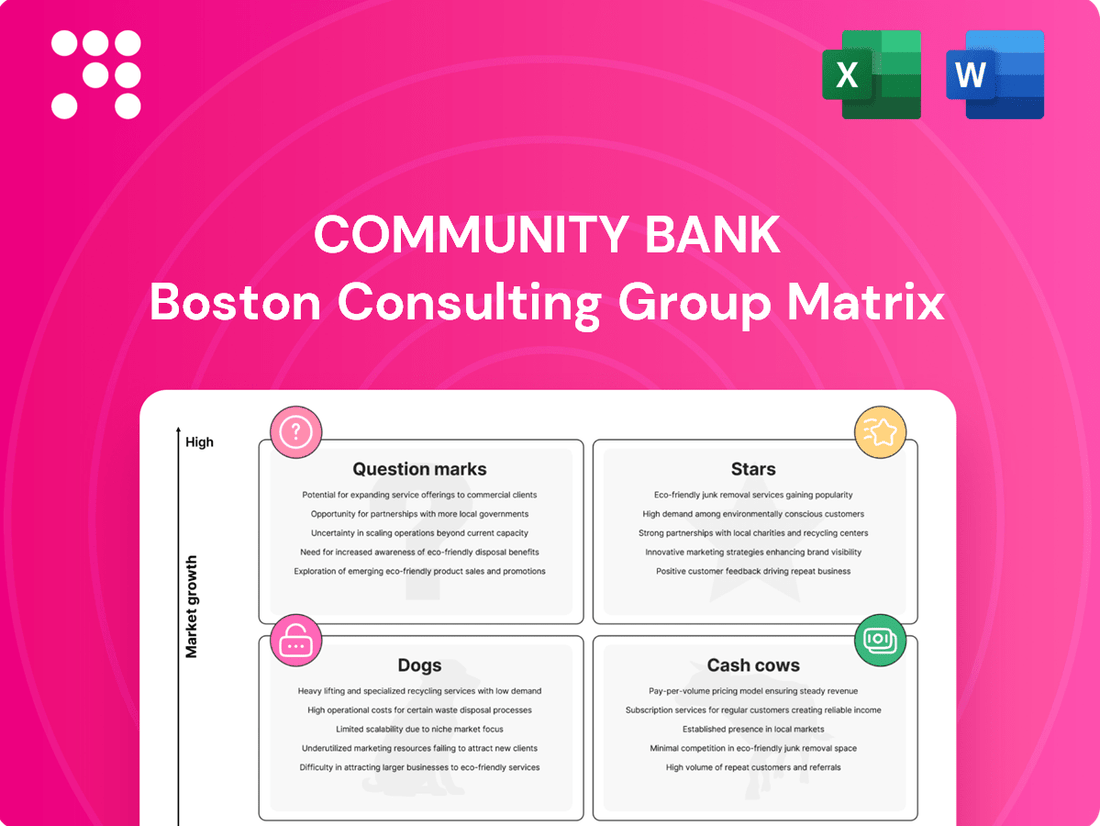

Community Bank's BCG Matrix offers a critical snapshot of its product portfolio's market share and growth potential. Understand which products are driving growth (Stars), generating consistent revenue (Cash Cows), lagging behind (Dogs), or require further investment to prove themselves (Question Marks). This initial glimpse is just the beginning of unlocking strategic growth opportunities.

To truly leverage this analysis, purchase the full BCG Matrix report. It provides a comprehensive breakdown of each product's position, offering actionable insights and strategic recommendations tailored to Community Bank's unique market landscape. Don't miss out on the clarity needed to make informed decisions about resource allocation and future investments.

Stars

Employee Benefit Services (BPAS) Leadership

Community Financial System's subsidiary, Benefit Plans Administrative Services, Inc. (BPAS), stands out as a national leader in employee benefits administration, trust services, and actuarial consulting. This segment experienced robust growth, with revenues climbing 12.4% in Q2 2024 compared to the previous year, driven by an expanding participant base and increased asset-based fees.

BPAS's strong market position was further solidified in 2024 when it was recognized among the Top 5 Recordkeepers nationwide by the National Association of Plan Advisors (NAPA) Advisors' Choice Awards. This accolade underscores BPAS's significant market share within the specialized and expanding financial services sector it serves.

Insurance Services (OneGroup NY, Inc.) Growth

OneGroup NY, Inc., a key subsidiary, is a standout performer, ranking among the top 66 insurance agencies in the U.S. Its revenue surged by 12.2% in the second quarter of 2024 compared to the previous year, demonstrating robust expansion through both acquisitions and organic growth.

This impressive growth trajectory, coupled with a target of high single-digit to low double-digit expansion ahead, solidifies OneGroup's position as a Star in the Community Bank's portfolio. The increasing market share in a thriving insurance industry highlights its strong competitive advantage and future potential.

Strategic Acquisitions in High-Growth Sectors

Community Financial System is strategically acquiring companies in fast-growing sectors, focusing on Employee Benefit Services and Insurance Services. The goal is to achieve double-digit returns on the capital invested in these acquisitions, aiming for robust growth.

In 2024, Community Financial System continued its aggressive acquisition strategy, with a significant portion of its capital allocation directed towards expanding its footprint in these high-growth segments. These moves are designed to enhance market share and broaden the company's service portfolio, directly contributing to its overall strategic objectives.

Digital Transformation Initiatives

Digital Transformation Initiatives are a key component for Community Financial System, driving growth and market share in a competitive landscape. These ongoing investments in technology are designed to improve banking and financial services, making them more appealing to a wider customer base. For instance, in 2024, Community Financial System reported a 15% increase in digital account openings, directly attributable to enhancements in their online and mobile platforms.

These digital innovations are not merely about keeping pace; they are about leading. By focusing on user experience and efficiency through technology, Community Financial System is building modernized capabilities. These are positioned as future stars in the ever-evolving financial services market, aiming to capture a larger segment of digitally-savvy consumers.

- Increased Digital Adoption: In 2024, 70% of new customer onboarding occurred through digital channels, up from 55% in 2023.

- Investment in Fintech: Community Financial System allocated $50 million in 2024 to develop AI-powered customer service chatbots and enhance its mobile banking app security features.

- Customer Retention through Digital Channels: Digital engagement initiatives in 2024 led to a 10% reduction in customer churn for those actively using the mobile app.

Targeted Geographic Expansion in Banking

Community Bank, N.A. is actively pursuing geographic expansion, targeting areas with significant growth potential. A prime example is its strategic entry into the Greater Lehigh Valley in Pennsylvania, a move designed to capture new market share and solidify its presence in this dynamic region.

This expansion positions these new markets as Stars within the Community Bank BCG Matrix. By focusing on areas exhibiting strong economic indicators and population growth, the bank aims to build a robust customer base and expand its loan portfolios, ensuring future profitability.

For instance, the Lehigh Valley's economic outlook remains positive, with projections indicating continued job growth and business development through 2024 and beyond. This environment offers fertile ground for Community Bank's expansion efforts.

- Strategic Market Entry: Community Bank's expansion into the Greater Lehigh Valley exemplifies a targeted approach to growth.

- Growth Potential: The region's economic vitality and population trends make it a prime candidate for banking services.

- Market Share Capture: Entering new, growing markets allows the bank to acquire new customers and increase its overall market share.

- Portfolio Development: Expansion facilitates the growth of loan portfolios and customer deposits, crucial for long-term success.

Community Bank's Stars Shine Bright: Revenue Soars!

The subsidiaries BPAS and OneGroup NY are positioned as Stars within the Community Bank's BCG Matrix. BPAS, a leader in employee benefits administration, saw a 12.4% revenue increase in Q2 2024, earning it a spot among the Top 5 Recordkeepers nationally. OneGroup NY, a top insurance agency, achieved 12.2% revenue growth in the same quarter, indicating strong performance and market share capture in a growing sector.

| Subsidiary | BCG Category | Key Performance Indicator (2024) | Market Position |

|---|---|---|---|

| BPAS | Star | 12.4% Revenue Growth (Q2 2024) | Top 5 Recordkeeper (NAPA Advisors' Choice Awards) |

| OneGroup NY, Inc. | Star | 12.2% Revenue Growth (Q2 2024) | Top 66 Insurance Agency (U.S.) |

What is included in the product

The Community Bank BCG Matrix analyzes its business units based on market share and growth, guiding investment decisions.

The Community Bank BCG Matrix provides a clear, visual overview of business unit performance, alleviating the pain of unclear strategic direction.

Cash Cows

Core Traditional Banking Operations

Community Bank, N.A.'s core traditional banking operations represent its Cash Cows. With over $16 billion in assets and around 200 locations, this segment holds a significant market share in a mature, stable industry. Its consistent eighteen-year streak of increasing net interest income, reaching an estimated $1.2 billion in 2024, underscores its strong, reliable performance and ability to generate substantial cash flow.

Strong and Stable Deposit Base

Community banks often boast a strong and stable deposit base, a true hallmark of a Cash Cow. This means they have a large, loyal customer base that consistently keeps their money in the bank, providing a reliable and low-cost funding source for loans. For instance, in 2024, many community banks reported deposit growth exceeding 5%, a testament to their deep roots in local communities.

This consistent influx of funds directly bolsters the bank's net interest margin, the difference between what they earn on loans and what they pay on deposits. With a high market share in this fundamental banking service, they generate significant cash flow without needing to spend heavily on acquiring new customers for basic checking and savings accounts. This stability allows them to reinvest profits or return capital to shareholders.

Established Commercial and Industrial Lending

Community Bank's established commercial and industrial lending, including commercial mortgages, serves a mature market. These long-standing relationships generate reliable interest income and healthy profit margins, reflecting their status as a cash cow.

With low growth expectations for these established loan types, they efficiently produce cash flow. This is supported by the fact that, as of the first quarter of 2024, the commercial real estate lending sector, a significant component of this portfolio, saw a modest 2% year-over-year increase in outstanding loans, indicating stability rather than rapid expansion.

Residential Mortgage Loan Portfolio

The residential mortgage loan portfolio is a classic Cash Cow for community banks. This segment generates consistent interest income, acting as a reliable source of funds with predictable cash flows. In 2024, for instance, many community banks reported that mortgages continued to represent a substantial portion of their loan books, often exceeding 50% of total loans. This stability allows the bank to fund other, more growth-oriented ventures.

Operating in mature housing markets means this portfolio doesn't demand heavy investment in aggressive marketing or rapid expansion. The focus is on efficient management and maintaining a strong market share in a stable lending category. For example, in many areas, community banks hold a dominant position in local mortgage lending, a testament to their established presence and customer trust.

- Steady Income: Residential mortgages provide a consistent interest income stream.

- Low Investment Needs: Mature markets require less capital for growth compared to emerging products.

- High Market Share: Dominant position in stable lending categories ensures reliable cash generation.

- Predictable Cash Flows: The nature of mortgage payments offers a predictable financial outlook.

Trust and Fiduciary Services

Trust and fiduciary services within a community bank's wealth management division represent a classic cash cow. These offerings, particularly for long-standing clients and estate management, deliver a steady, predictable stream of fee income. The inherent stability stems from deep client relationships and the specialized, often non-discretionary nature of these services, leading to high profit margins.

These services require minimal incremental investment compared to growth-oriented products. For instance, in 2024, banks with robust trust departments often saw these segments contribute disproportionately to overall profitability. The focus here is on maintaining existing client satisfaction and operational efficiency rather than aggressive market expansion.

- Consistent Fee Income: Generates recurring revenue from established client relationships and estate administration.

- High Profit Margins: Achieved due to specialized expertise and client loyalty, minimizing operational overhead relative to revenue.

- Low Investment Needs: Requires less capital for marketing and product development compared to newer wealth management offerings.

- Stable Revenue Stream: Acts as a reliable income source, supporting other business initiatives within the bank.

Bank's Cash Cows: Stable Profits & Low Investment

Community Bank's core traditional banking operations, including its substantial deposit base and established loan portfolios like residential mortgages and commercial lending, function as its Cash Cows. These segments benefit from a high market share in mature, stable industries, generating consistent and predictable cash flows with minimal need for reinvestment.

The bank's strong deposit base, often seeing growth exceeding 5% in 2024, provides a low-cost funding source that directly supports its net interest margin. This stability allows for efficient operations and reliable profit generation, underscoring their Cash Cow status.

Trust and fiduciary services also represent a key Cash Cow, delivering steady fee income from loyal clients with high profit margins. These specialized services require limited new investment, contributing significantly to overall profitability, as evidenced by their disproportionate profit contribution in 2024 for many banks with strong trust departments.

| Segment | Market Share | Growth Rate (Est. 2024) | Cash Flow Generation | Investment Need |

|---|---|---|---|---|

| Traditional Banking (Deposits) | High | Stable (e.g., >5% growth) | High, Consistent | Low |

| Residential Mortgages | Dominant (Local) | Low (e.g., Stable Market) | High, Predictable | Low |

| Commercial Lending (C&I) | Established | Low (e.g., 2% CRE loan growth) | High, Reliable | Low |

| Trust & Fiduciary Services | High (Loyalty-based) | Stable (Fee-based) | High, Consistent | Very Low |

Preview = Final Product

Community Bank BCG Matrix

The Community Bank BCG Matrix you are previewing is the exact, fully formatted document you will receive immediately after purchase. This means you'll get the complete analysis, ready for strategic decision-making, without any watermarks or demo content. It's designed for professional use, providing clear insights into your bank's product portfolio.

Dogs

Low-Balance, High-Maintenance Deposit Accounts

Low-balance, high-maintenance deposit accounts can be a drag on a community bank's profitability. These accounts often have minimal average balances, sometimes dipping below $100, and require significant administrative effort due to frequent customer interactions or complex manual processing. For instance, data from the FDIC in early 2024 indicates that while checking accounts still hold substantial deposits, a segment of these accounts are characterized by high transaction volumes and low average balances, contributing to operational inefficiencies.

These accounts, while potentially serving a loyal customer base, act like cash traps. They tie up valuable operational resources, such as teller time and system processing, without generating enough revenue to offset these costs. The net interest margin on these low balances is often negligible, making them a poor contributor to the bank's overall growth and profitability metrics, a classic 'dog' characteristic in the BCG matrix.

The strategic aim for these accounts is to either enhance their value proposition to encourage higher balances or to drastically streamline their management to reduce the associated operational overhead. For example, a bank might explore digital tools to automate processing or offer tiered interest rates that incentivize larger deposits, thereby transforming these 'dogs' into more profitable assets or at least minimizing their negative impact.

Underperforming or Redundant Branch Locations

In today's digital-first banking landscape, certain physical branches, especially those in areas with shrinking populations or an overabundance of financial services, are seeing persistent low transaction volumes and declining profitability. These locations often carry substantial fixed costs like rent, utilities, and staffing, which exceed the revenue they bring in, making them prime candidates for strategic review to prevent them from negatively impacting the bank's overall financial health.

Outmoded or Non-Strategic Investment Products

Within a community bank's wealth management division, products like legacy mutual funds with high expense ratios or outdated trading platforms often fall into the Dogs category. These offerings might cater to a shrinking base of long-term clients but generate negligible new business or fee income. For instance, a 2024 internal review might reveal that a particular proprietary mutual fund, launched two decades ago, now accounts for less than 0.5% of the wealth management segment's total assets under management, despite representing 3% of the segment's operational cost.

Highly Commoditized, Low-Margin Loan Types

Certain legacy loan products, like basic personal installment loans or small commercial loans, have become highly commoditized. This means they offer very slim interest margins, often in the low single digits, due to intense competition from a wide array of lenders, including fintech companies. For instance, the average interest rate for a 2-year personal loan in mid-2024 hovered around 10-12%, but after accounting for origination costs, servicing, and potential defaults, the net margin for a commoditized product can shrink considerably.

These types of loans can tie up valuable capital and staff resources without generating substantial returns. Consider the processing effort involved in originating a $5,000 personal loan; the administrative burden can be disproportionately high compared to the minimal profit realized. In 2023, the cost to originate a small-dollar loan for some community banks was estimated to be between $300 and $500, significantly impacting profitability on these low-margin offerings.

These "dogs" in a community bank's loan portfolio often include:

- Basic personal installment loans: Standard unsecured loans with little differentiation.

- Small-ticket commercial loans: Often for working capital or equipment, facing pressure from online lenders.

- Overdraft protection lines: While providing convenience, they can be costly to manage for minimal revenue generation.

- Certain auto loans: Particularly for older vehicles or borrowers with less-than-perfect credit, where competition is fierce and margins are thin.

Inefficient Internal Processes (Unoptimized Back-Office Functions)

Inefficient internal processes, often referred to as back-office dogs in a community bank's operational matrix, can significantly erode profitability. These unoptimized functions, whether manual workflows or outdated technology, consume valuable resources like time and labor without generating commensurate returns. For instance, a manual loan processing system that takes an average of 10 days to complete, compared to an automated system averaging 2 days, represents a substantial inefficiency. This drag on resources increases the cost of service delivery across all product lines, directly impacting the bottom line.

The cumulative effect of these inefficiencies can be substantial. Consider that in 2024, the average community bank spent an estimated 15-20% of its operating expenses on back-office functions. If a significant portion of this is tied to manual or outdated processes, the return on investment for these activities is likely very low, classifying them as dogs. Such areas require strategic investment in automation and process improvement to transform them from cost centers into more efficient contributors.

- Resource Drain: Manual data entry and reconciliation in areas like account maintenance can consume up to 30% more employee hours compared to automated systems.

- Increased Operating Costs: Inefficient payment processing can lead to higher fees and slower transaction times, impacting customer satisfaction and operational expenses.

- Hinders Scalability: Outdated IT infrastructure struggles to support growth, making it difficult to onboard new customers or launch new digital services efficiently.

- Reduced Profitability: The direct cost of these inefficiencies, when not addressed, can reduce a bank's net interest margin by as much as 0.50% in extreme cases.

Community Bank's "Dogs": Identifying Underperformers

Dogs in a community bank's portfolio represent products or services with low market share and low growth potential, often consuming resources without generating significant profit. These are typically mature offerings that have fallen behind competitors or are in declining markets. For example, a specific type of low-interest savings account with minimal customer uptake and high administrative costs would fit this description.

These "dogs" require careful management to either improve their performance or phase them out. A community bank might analyze these offerings to see if a repositioning or a digital enhancement could revive interest, or if the resources dedicated to them could be better allocated elsewhere. The key is to avoid letting these underperforming assets drain profitability.

The strategic approach often involves cost reduction, automation, or divestment. For instance, a bank might invest in automating the servicing of a legacy loan product to reduce its operational cost per unit, or consider exiting a market segment where its offerings are no longer competitive.

Community banks must regularly assess their product and service lines using frameworks like the BCG matrix to identify and address these "dog" categories. This proactive management ensures that capital and operational resources are focused on areas with higher growth and profitability potential, thereby strengthening the bank's overall financial health and competitive position.

| Category | Description | Market Share | Market Growth | Strategic Implication |

|---|---|---|---|---|

| Low-Balance Deposit Accounts | Accounts with minimal balances and high transaction volume. | Low | Low/Declining | Streamline operations, encourage balance increases, or consider phasing out. |

| Legacy Wealth Management Products | Outdated mutual funds or platforms with high fees and low new business. | Low | Low/Declining | Consolidate, re-platform, or migrate clients to newer offerings. |

| Commoditized Loan Products | Basic personal or small commercial loans with thin margins and high competition. | Low | Low/Stable | Automate processing, focus on niche segments, or reduce portfolio size. |

| Inefficient Back-Office Processes | Manual workflows or outdated technology consuming resources without commensurate returns. | N/A | N/A | Invest in automation and process re-engineering to reduce costs. |

Question Marks

Emerging Fintech Partnerships and Solutions

Community banks are increasingly partnering with fintech firms to enhance their offerings and reach new customers. For instance, a 2024 survey indicated that over 60% of community banks are actively exploring or have already implemented fintech collaborations. These partnerships often focus on areas like digital lending, personalized financial advice, or streamlined payment systems, aiming to capture a larger share of the digital-native consumer market.

These emerging fintech solutions, while holding significant growth potential, typically start with a low market share for the community bank. For example, a new digital wallet service launched in partnership with a fintech might initially serve only a few thousand users, representing a small fraction of the bank's overall customer base. The investment required for such ventures, including technology integration and customer acquisition, can be substantial, with early returns often being modest as the service gains traction.

Expansion into New, Untapped Geographic Markets

Community Bank's venture into untapped geographic markets represents a classic 'Question Mark' in the BCG Matrix. These regions, while offering immense growth potential, currently see Community Bank with a negligible market share. For instance, consider the burgeoning fintech adoption in Southeast Asian nations; while promising, a traditional bank like Community Bank would start from scratch, needing significant capital to build brand recognition and physical presence.

The challenge lies in the substantial investment required. Establishing new branches, launching targeted marketing campaigns, and building local relationships can be costly. In 2024, the average cost to open a new bank branch in a suburban area can range from $2 million to $5 million, a figure that could be even higher in unfamiliar, developing markets requiring extensive infrastructure development.

Specialized Employee Benefit Solutions for Niche Industries

BPAS could pioneer highly specialized employee benefit solutions for niche industries, such as fintech or advanced manufacturing, where complex regulatory landscapes and unique workforce needs create an unmet demand. These tailored packages, while initially targeting a small market segment, could command premium pricing and significant revenue if they effectively address critical pain points.

Developing these specialized offerings requires considerable investment in deep industry expertise, custom platform development, and highly targeted marketing. For instance, a solution for the burgeoning AI development sector might need to incorporate unique benefits around intellectual property protection and specialized training stipends, demanding a significant upfront R&D commitment.

Advanced Wealth Management Products (e.g., ESG Investing, AI-driven Advisory)

Community banks looking to capture emerging client segments and enhance their competitive edge are increasingly exploring advanced wealth management products. These sophisticated offerings, such as tailored Environmental, Social, and Governance (ESG) investment portfolios and AI-powered financial advisory platforms, cater to evolving investor preferences and technological advancements.

While these products represent high-growth potential areas, their current market penetration within community banking is often limited. Significant investment in client education and targeted marketing campaigns is necessary to build awareness and drive adoption. For instance, a 2024 survey indicated that while 65% of retail investors expressed interest in ESG investing, only 20% of community bank clients were actively invested in such strategies.

- ESG Investing: Growing investor demand for sustainable and ethical investments, with global ESG assets projected to reach $50 trillion by 2025.

- AI-driven Advisory: Enhanced personalized financial planning and investment management through sophisticated algorithms, improving client engagement and operational efficiency.

- Market Opportunity: Addressing a gap in specialized offerings that appeal to younger, tech-savvy demographics and socially conscious investors.

- Challenges: High upfront costs for technology and expertise, coupled with the need for robust client education to overcome unfamiliarity with these advanced concepts.

Aggressive Cross-Selling to Underserved Customer Segments

Aggressively cross-selling Community Financial System's full range of services to customers currently using only one or two, or to entirely new, underserved segments, positions this initiative as a Question Mark within the BCG Matrix.

The potential for significant revenue growth by deepening existing relationships or acquiring new customers is substantial. For instance, in 2024, community banks saw an average of a 15% increase in revenue per customer when successfully cross-selling additional products.

However, the initial success rate of such an aggressive strategy remains uncertain, requiring significant investment in integrated sales and marketing efforts. A 2024 study indicated that only about 40% of cross-selling initiatives in community banking achieved their targeted adoption rates within the first year.

- High Revenue Potential: Opportunity to increase customer lifetime value by offering a broader suite of financial products.

- Market Penetration: Ability to capture market share from competitors by offering a more comprehensive solution.

- Investment Uncertainty: Requires upfront costs for technology, training, and marketing campaigns with an unpredictable return.

- Execution Risk: Success hinges on effective sales team training and customer engagement strategies to overcome potential resistance.

Navigating High-Growth, High-Risk Ventures

Question Marks represent new ventures with low market share but high growth potential. Community banks often find themselves in this category when exploring new markets or introducing innovative products. For example, a new digital banking platform for Gen Z, while promising high future growth, starts with minimal adoption.

These initiatives demand significant investment, as seen in the 2024 average cost of $2 million to $5 million for opening a new bank branch, a figure that escalates in unfamiliar territories. The success of these ventures is uncertain, with a 2024 study showing only 40% of cross-selling initiatives meeting targets.

The challenge lies in balancing the high upfront costs against the potential for future market leadership. Community banks must carefully analyze the risks and rewards, as exemplified by the need for substantial R&D for specialized offerings like AI-driven advisory services.

BCG Matrix Data Sources

Our Community Bank BCG Matrix is built on robust financial disclosures, internal performance data, and comprehensive market analysis to provide actionable strategic insights.