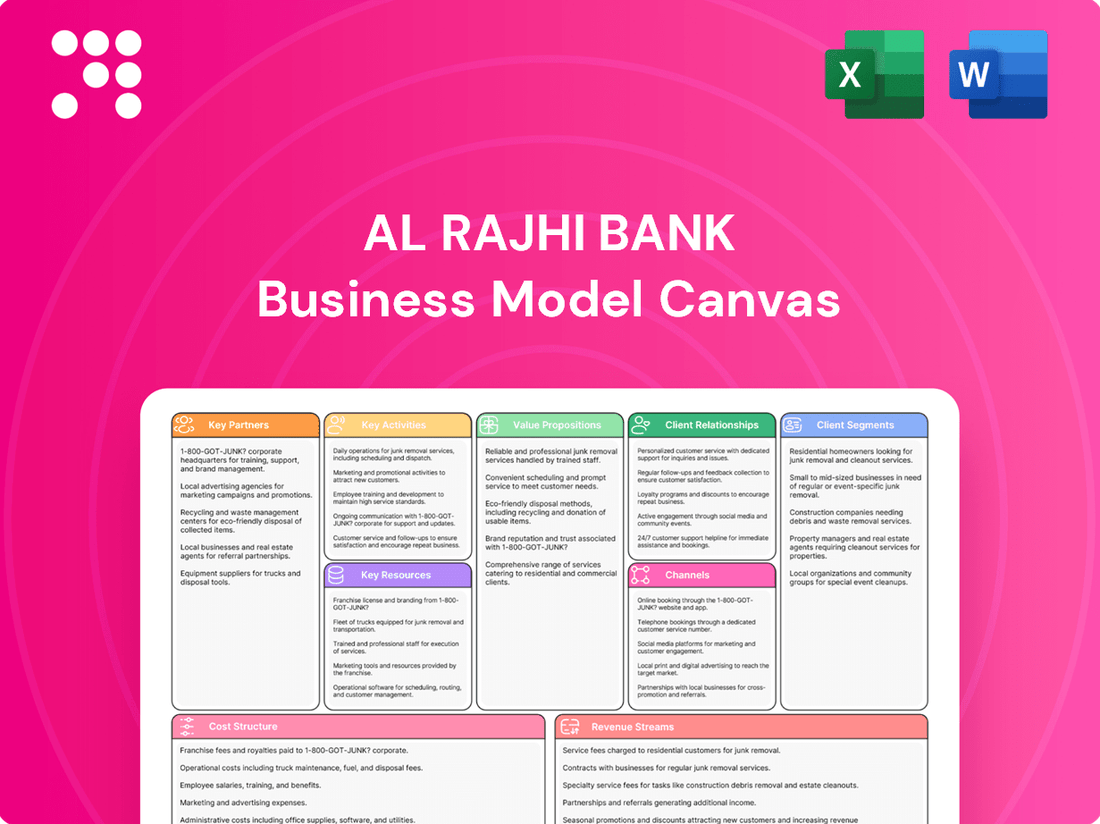

Al Rajhi Bank Business Model Canvas

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Al Rajhi Bank Bundle

Al Rajhi Bank: Unveiling the Business Model Canvas

Curious about the strategic engine driving Al Rajhi Bank's success? Our comprehensive Business Model Canvas breaks down their customer relationships, revenue streams, and key resources. Discover the core elements that power their operations.

Unlock the full strategic blueprint behind Al Rajhi Bank's business model. This in-depth Business Model Canvas reveals how the company drives value, captures market share, and stays ahead in a competitive landscape. Ideal for entrepreneurs, consultants, and investors looking for actionable insights.

Partnerships

Technology Providers

Al Rajhi Bank actively partners with premier technology providers to bolster its digital banking ecosystem. These collaborations are instrumental in upgrading its mobile banking applications, core digital platforms, and robust cybersecurity defenses.

These strategic alliances are vital for Al Rajhi Bank to offer customers a smooth, secure, and cutting-edge digital banking experience. For instance, in 2024, the bank continued to invest heavily in cloud infrastructure and AI-driven customer service solutions through such partnerships.

This focus on technology partnerships directly supports Al Rajhi Bank's forward-looking 'Bank of the Future' strategy and its internal 'Harmonize the Group' initiative, ensuring technological advancements are integrated across its operations.

Financial Institutions & Payment Networks

Al Rajhi Bank actively partners with other financial institutions to facilitate crucial interbank transactions, enabling seamless remittances and participation in syndicated financing deals. These collaborations are vital for managing liquidity and offering larger-scale financial solutions.

Crucially, the bank maintains strong ties with major payment networks. This allows Al Rajhi Bank to offer robust card services, including debit and credit cards, and ensures widespread accessibility through extensive ATM networks and point-of-sale (POS) terminals. In 2023, Saudi Arabia's non-cash transactions, largely driven by card payments, reached a significant milestone, reflecting the importance of these partnerships.

Government and Regulatory Bodies

Al Rajhi Bank cultivates crucial partnerships with government and regulatory bodies, notably the Saudi Central Bank (SAMA). These relationships are foundational for ensuring strict adherence to Sharia principles and all banking regulations, thereby maintaining operational legitimacy.

These collaborations extend to supporting national economic development agendas, such as Saudi Arabia's Vision 2030. For instance, Al Rajhi Bank actively participates in initiatives aimed at boosting financial inclusion and supporting small and medium-sized enterprises (SMEs), contributing to the Kingdom's broader economic diversification goals.

Real Estate Developers and Mortgage Partners

Al Rajhi Bank's substantial mortgage lending activities make strategic alliances with real estate developers and housing initiatives absolutely crucial to its business model. These partnerships are instrumental in delivering Sharia-compliant home financing options to a broad customer base, simultaneously fueling expansion within the real estate market.

These collaborations enable Al Rajhi Bank to offer tailored financing solutions that align with Islamic principles, making homeownership more accessible. For instance, in 2024, the bank continued to leverage these relationships to support various government housing programs aimed at increasing homeownership rates across Saudi Arabia.

- Developer Collaborations: Al Rajhi Bank partners with leading real estate developers to offer integrated financing packages for new property developments, streamlining the home-buying process for customers.

- Housing Initiative Support: The bank actively participates in and supports national housing initiatives, providing mortgage solutions that align with government objectives for affordable housing.

- Market Growth Contribution: By facilitating access to Sharia-compliant financing, these partnerships directly contribute to the dynamism and growth of the Saudi real estate sector.

Small and Medium Enterprise (SME) Support Organizations

Al Rajhi Bank actively partners with various Small and Medium Enterprise (SME) support organizations to expand its SME financing business. These collaborations are crucial for reaching a broader spectrum of SMEs and providing them with specialized financial products designed to address their unique requirements, thereby supporting economic diversification efforts.

These partnerships allow Al Rajhi Bank to tap into established networks and leverage the expertise of organizations dedicated to SME growth. This strategic approach ensures that the bank can effectively identify and serve SMEs that might otherwise be underserved, fostering a more inclusive financial ecosystem.

- Enhanced Reach: Collaborations with chambers of commerce, industry associations, and government SME agencies in Saudi Arabia allow Al Rajhi Bank to connect with a larger pool of potential SME clients.

- Tailored Solutions: Working with these organizations helps Al Rajhi Bank understand specific industry needs, enabling the development of customized financing options, such as specialized working capital loans or equipment financing.

- Economic Impact: By supporting SMEs through these partnerships, Al Rajhi Bank contributes to job creation and economic diversification, aligning with national development goals. For instance, Saudi Arabia's Vision 2030 emphasizes the significant role of SMEs in its economic transformation.

Enhancing Digital Banking: Strategic Tech Partnerships & 2024 AI Focus

Al Rajhi Bank's key partnerships extend to technology providers, enabling enhancements in digital banking, cybersecurity, and customer service solutions. These collaborations are crucial for delivering a seamless and secure digital experience, with significant investments in cloud infrastructure and AI in 2024.

What is included in the product

A comprehensive, pre-written business model tailored to Al Rajhi Bank’s strategy, covering customer segments, channels, and value propositions in full detail.

Reflects the real-world operations and plans of Al Rajhi Bank, organized into 9 classic BMC blocks with full narrative and insights.

Al Rajhi Bank's Business Model Canvas acts as a pain point reliever by clearly outlining how they address customer financial challenges through Sharia-compliant solutions and accessible digital platforms.

Activities

Retail Banking Operations

Al Rajhi Bank's retail banking operations are centered on managing its extensive physical and digital infrastructure to serve individual customers. This includes a wide network of over 700 branches and more than 4,700 ATMs across Saudi Arabia, alongside robust digital platforms. The bank focuses on delivering core services like current and savings accounts, personal financing, and credit cards, aiming for a seamless customer journey.

A significant emphasis is placed on digital transformation to create a hyper-personalized, omnichannel experience. In 2024, Al Rajhi Bank reported a substantial increase in its digital customer base, with over 1.7 million active digital users, underscoring the success of its strategy to enhance digital engagement and service delivery.

Corporate and SME Banking

Al Rajhi Bank offers a broad spectrum of financial solutions specifically designed for corporations and Small and Medium-sized Enterprises (SMEs). This includes vital services such as corporate financing to fuel growth, trade finance to facilitate international business, and sophisticated treasury services for efficient cash management.

The bank is strategically focused on deepening its relationships with large corporations, aspiring to be their primary banking partner. Simultaneously, Al Rajhi Bank is actively expanding its SME customer base by developing and delivering customized financial products that address the unique needs of these businesses.

In 2023, Al Rajhi Bank reported significant growth in its corporate and SME segments, with a notable increase in financing facilities extended to these clients. For instance, the bank's total financing portfolio saw robust expansion, reflecting its commitment to supporting Saudi Arabia's economic diversification efforts under Vision 2030.

Investment Banking and Treasury Services

Al Rajhi Bank's Investment Banking and Treasury Services are central to its operations, focusing on managing investment portfolios and providing Sharia-compliant financial products. This segment offers expertise in wealth management and capital markets, catering to a diverse client base seeking ethical investment opportunities.

The bank actively engages in treasury operations, including liquidity and capital management, crucial for financial stability. In 2024, Al Rajhi Bank continued its commitment to sustainable finance by issuing Sukuk, reinforcing its leadership in Islamic finance and its role in supporting economic development through responsible financial practices.

Digital Transformation and Innovation

Al Rajhi Bank's key activities heavily revolve around driving digital transformation and fostering innovation. A central focus is the ongoing development and refinement of its digital banking services. This includes enhancing its mobile application and online banking platforms, as well as expanding its digital payment solutions to meet evolving customer needs.

These efforts are directly tied to the bank's strategic objectives, particularly its vision to be the 'Bank of the Future' and to 'Harmonize the Group'. The aim is to deliver a banking experience that is not only seamless but also digitally superior, ensuring customer convenience and accessibility across all touchpoints.

- Digital Platform Enhancement: Continuous investment in improving the user experience and functionality of Al Rajhi Bank's mobile app and online portal.

- Innovation in Payments: Development and integration of new digital payment methods and technologies to facilitate secure and efficient transactions.

- Customer-Centric Digital Solutions: Creating digital tools and services that directly address customer pain points and preferences, fostering greater engagement.

Sharia Compliance and Governance

Al Rajhi Bank's key activity revolves around ensuring all its operations and financial products strictly adhere to Islamic Sharia principles. This commitment is paramount to its identity and customer trust.

This involves robust governance structures, including the continuous oversight and guidance of its Sharia Supervisory Board. This board plays a crucial role in validating the Sharia compliance of new products and existing services.

Integrating ethical and sustainable practices is also a core activity, reflecting a broader commitment to responsible finance. This includes avoiding investments in prohibited sectors and promoting socially beneficial activities.

- Sharia Compliance: Al Rajhi Bank's core activity is maintaining strict adherence to Islamic Sharia principles across its entire product and service portfolio.

- Sharia Supervisory Board: Continuous oversight and validation by an independent Sharia Supervisory Board is a critical ongoing activity.

- Ethical Integration: Embedding ethical considerations and sustainable practices into all financing and operational activities is a fundamental key activity.

- Product Development: Ensuring all new and existing financial products are developed and managed in compliance with Sharia guidelines is a constant activity.

Islamic Finance Leader's Digital Evolution & Sharia Adherence

Al Rajhi Bank's key activities are deeply rooted in its digital transformation strategy and its unwavering commitment to Sharia compliance. The bank continuously enhances its digital platforms, aiming for a superior customer experience. This includes innovation in payment solutions and the development of customer-centric digital tools, a focus that saw its digital customer base grow significantly in 2024.

Furthermore, a core activity is ensuring all financial products and operations strictly adhere to Islamic Sharia principles, overseen by a dedicated Sharia Supervisory Board. This ethical integration extends to promoting sustainable practices, reinforcing its position as a leader in Islamic finance.

Preview Before You Purchase

Business Model Canvas

The Al Rajhi Bank Business Model Canvas preview you're viewing is an exact replica of the document you will receive upon purchase. This means you're seeing the actual, complete file, not a simplified sample or a mockup. Once your order is processed, you'll gain full access to this professionally structured and formatted Business Model Canvas, ready for immediate use.

Resources

Strong Financial Capital

Al Rajhi Bank's strong financial capital is a cornerstone of its business model, evidenced by a significant asset base and a healthy deposit base. As of the first quarter of 2024, the bank reported total assets of SAR 853.1 billion, underscoring its substantial financial muscle.

This robust capital structure, including strong shareholder equity, is critical for supporting its extensive lending activities and ensuring ample liquidity. The bank's ability to attract and retain deposits, a key component of its funding, allows it to efficiently finance its operations and pursue growth opportunities in the financial services sector.

Extensive Branch and ATM Network

Al Rajhi Bank's extensive branch and ATM network is a cornerstone of its business model, offering unparalleled accessibility to its vast customer base. As of early 2024, the bank operates over 700 branches and more than 5,000 ATMs across Saudi Arabia, facilitating seamless transactions and customer service. This robust physical infrastructure ensures convenience for millions of customers, solidifying its position as a leading financial institution.

Advanced Technology Infrastructure

Al Rajhi Bank's advanced technology infrastructure is a cornerstone of its business model, encompassing state-of-the-art digital banking platforms, robust core banking systems, and sophisticated cybersecurity measures. This technological backbone is essential for driving its digital transformation initiatives and delivering innovative financial solutions to its customers.

In 2024, Al Rajhi Bank continued to invest heavily in its digital capabilities, aiming to enhance customer experience and operational efficiency. This focus on technology allows the bank to offer a seamless and secure digital banking environment, a critical factor in retaining and attracting customers in today's competitive market.

Skilled Human Capital

Al Rajhi Bank's skilled human capital is a cornerstone of its operations, encompassing a diverse team of banking professionals, Sharia scholars, IT specialists, and customer service representatives. This extensive workforce is crucial for delivering superior financial services and fostering innovation across the organization.

The bank actively prioritizes attracting, retaining, and developing its talent pool. This commitment ensures the workforce remains equipped with the latest skills and knowledge to meet evolving market demands and customer expectations. For instance, in 2023, Al Rajhi Bank reported a significant number of employees dedicated to enhancing customer experience and digital transformation initiatives.

- Talent Pool: A large and experienced workforce is essential for high-quality service delivery and innovation.

- Expertise: Includes banking professionals, Sharia scholars, IT specialists, and customer service staff.

- Development Focus: The bank emphasizes talent attraction, retention, and continuous development programs.

- 2023 Data: Al Rajhi Bank's employee count and investment in training reflect its commitment to human capital.

Reputation and Brand Value

Al Rajhi Bank leverages its status as the world's largest Islamic bank and a prominent Saudi brand to build significant reputation and brand value. This strong standing, rooted in Sharia compliance, trustworthiness, and a focus on customer needs, acts as a crucial intangible asset.

This established brand value directly contributes to customer acquisition and loyalty, attracting and retaining a broad base of clients and stakeholders who value the bank's ethical and customer-centric approach.

- Global Recognition: As the largest Islamic bank globally, Al Rajhi Bank commands international recognition, enhancing its credibility and appeal to a diverse customer base.

- Trust and Compliance: Its unwavering commitment to Sharia principles fosters deep trust, a critical differentiator in the financial services sector.

- Customer Loyalty: A consistent focus on customer satisfaction and tailored services cultivates strong brand loyalty, reducing churn and increasing lifetime customer value.

- Market Leadership: Being a leading Saudi brand reinforces its domestic market dominance and provides a strong foundation for regional and international expansion.

Unveiling a Bank's Core Strengths: Capital, Network, Tech, Talent, Reputation

Al Rajhi Bank's key resources include its substantial financial capital, extensive physical network, advanced technology infrastructure, skilled human capital, and its strong global reputation as the world's largest Islamic bank. These elements collectively enable the bank to offer a comprehensive range of financial services and maintain its market leadership.

| Key Resource | Description | 2024 Data/Significance |

| Financial Capital | Robust asset and deposit base, strong shareholder equity. | SAR 853.1 billion in total assets (Q1 2024). |

| Physical Network | Extensive branch and ATM presence. | Over 700 branches and 5,000+ ATMs across Saudi Arabia (early 2024). |

| Technology Infrastructure | State-of-the-art digital platforms, core banking systems, cybersecurity. | Continued heavy investment in digital capabilities for enhanced customer experience and efficiency. |

| Human Capital | Diverse team of banking professionals, Sharia scholars, IT specialists, customer service staff. | Focus on talent attraction, retention, and development; employees dedicated to customer experience and digital transformation. |

| Reputation & Brand Value | World's largest Islamic bank, prominent Saudi brand, Sharia compliance, trustworthiness. | Attracts and retains customers through ethical and customer-centric approach. |

Value Propositions

Sharia-Compliant Financial Solutions

Al Rajhi Bank's core value lies in providing a full suite of financial products and services that are meticulously designed to comply with Islamic Sharia law. This commitment ensures that customers can engage in banking activities that align with their ethical and religious beliefs, a crucial differentiator in the market.

This adherence to Sharia principles is not just a service but a fundamental pillar, attracting a significant customer base. For instance, in 2023, Al Rajhi Bank reported a net profit of SAR 13,573 million, reflecting strong customer trust and demand for its Sharia-compliant offerings.

The bank's extensive network and digital platforms further enhance this value proposition, making it convenient for customers to access Sharia-compliant banking, whether for personal finance, business needs, or investments, thereby fostering loyalty and market leadership.

Comprehensive and Universal Banking Services

Al Rajhi Bank's value proposition centers on offering a comprehensive suite of banking services, encompassing retail, corporate, investment, and treasury functions. This creates a holistic financial ecosystem, allowing customers to manage all their financial needs within a single, integrated platform.

This universal banking approach caters to a broad customer base, from individual consumers seeking personal accounts and loans to large corporations requiring complex financing and investment solutions. For instance, in 2024, Al Rajhi Bank continued to expand its digital offerings, reporting a significant increase in transactions processed through its mobile banking app, demonstrating its commitment to providing accessible and diverse financial tools.

Digital Convenience and Innovation

Al Rajhi Bank provides a banking experience that is both easy to use and forward-thinking, offering customers a smooth journey across all channels. This means you can bank how and when you want, whether it's through their advanced mobile app or their online portal.

Their commitment to digital innovation means they're constantly improving their services. For instance, in 2023, Al Rajhi Bank reported a significant increase in digital transactions, highlighting customer adoption of their tech-forward approach. This focus allows for services tailored specifically to individual needs and instant access to all your banking needs.

Strong Customer-Centricity and Trust

Al Rajhi Bank places a strong emphasis on customer-centricity, aiming to build lasting trust and loyalty. This is evident in their commitment to tailored customer propositions designed to meet individual needs. Their focus on customer satisfaction directly contributes to long-term relationship building.

The bank's customer-centric approach is validated by its performance metrics. For instance, Al Rajhi Bank consistently achieves a high Net Promoter Score (NPS), indicating strong customer advocacy. This dedication to customer experience is a cornerstone of their business strategy.

- Customer-Centricity: Al Rajhi Bank prioritizes understanding and meeting customer needs.

- Trust and Loyalty: Building strong relationships through reliable service fosters customer loyalty.

- High NPS: A strong Net Promoter Score reflects positive customer experiences and satisfaction.

- Tailored Propositions: Offering customized products and services enhances customer value.

Financial Inclusion and Social Responsibility

Al Rajhi Bank's commitment extends beyond financial gains, focusing on broadening access to banking services for previously unbanked or underbanked populations. This dedication to financial inclusion is a core part of its value proposition, ensuring more individuals and communities can participate in the formal economy.

The bank actively invests in social development initiatives, aligning its business strategy with broader societal well-being. This dual focus on financial accessibility and community upliftment underscores its role as a responsible corporate citizen.

- Financial Inclusion Efforts: Al Rajhi Bank strives to reach underserved segments, making banking services more accessible.

- Social Responsibility Programs: The bank actively participates in and supports various social development initiatives.

- Community Engagement: This commitment to community engagement enhances its societal value and brand reputation.

- Sustainability Focus: By integrating social responsibility, Al Rajhi Bank builds a sustainable business model that benefits both shareholders and society.

Sharia-Compliant Banking: Digital, Customer-Centric, Community-Focused

Al Rajhi Bank offers a comprehensive suite of Sharia-compliant financial products and services, catering to diverse customer needs across retail, corporate, and investment banking. This commitment to Islamic finance is a key differentiator, attracting a loyal customer base seeking ethical banking solutions.

The bank’s value proposition is further strengthened by its focus on digital innovation, providing seamless and accessible banking experiences through advanced mobile and online platforms. This tech-forward approach ensures convenience and efficiency for all users.

Al Rajhi Bank also emphasizes customer-centricity, building trust through tailored propositions and a commitment to customer satisfaction, as evidenced by its strong Net Promoter Score. This focus fosters long-term relationships and enhances brand loyalty.

Furthermore, the bank actively promotes financial inclusion and engages in social responsibility initiatives, demonstrating a dedication to community well-being and broadening access to banking services for underserved populations.

| Value Proposition Aspect | Description | Supporting Data/Fact |

|---|---|---|

| Sharia-Compliant Offerings | Full suite of banking products adhering to Islamic law. | Al Rajhi Bank is the largest Islamic bank in the world by market capitalization. |

| Digital Accessibility | Advanced mobile and online banking platforms. | In 2023, digital transactions saw a significant increase, reflecting high customer adoption. |

| Customer-Centricity | Tailored services and focus on customer satisfaction. | Consistently high Net Promoter Score (NPS) indicating strong customer advocacy. |

| Financial Inclusion & Social Responsibility | Broadening access to banking and community support. | Active investment in social development initiatives and programs for underserved segments. |

Customer Relationships

Personalized Digital Engagement

Al Rajhi Bank is deeply invested in personalized digital engagement, utilizing data to craft unique banking experiences. This means customers receive recommendations and offers that genuinely fit their financial needs and habits, making interactions feel more relevant and helpful.

By analyzing customer data, Al Rajhi Bank can anticipate needs and proactively offer solutions through its digital channels. For instance, in 2024, the bank reported a significant increase in digital transaction volumes, underscoring the success of these personalized approaches in driving customer activity and satisfaction.

Dedicated Relationship Management

Al Rajhi Bank assigns dedicated relationship managers to its corporate clients, SMEs, and high-net-worth individuals. These managers are key to building trust and understanding unique client needs.

These specialized advisors provide tailored financial advice and develop customized solutions, ensuring clients receive personalized support. This approach aims to cultivate robust, long-lasting partnerships, a cornerstone of the bank's customer relationship strategy.

For instance, in 2024, Al Rajhi Bank reported a significant increase in its retail customer base, underscoring the effectiveness of personalized service in attracting and retaining clients.

Extensive Customer Support Channels

Al Rajhi Bank provides extensive customer support through a multi-channel approach. This includes readily available call centers, interactive online chat services, and active social media engagement, ensuring customers can reach out through their preferred method.

In 2024, Al Rajhi Bank reported a significant increase in digital customer interactions, with over 70% of customer inquiries handled through online channels. This highlights the bank's commitment to providing accessible and efficient support, catering to the evolving preferences of its diverse customer base.

Loyalty and Rewards Programs

Al Rajhi Bank actively cultivates customer relationships through its Mokafaa loyalty program. This initiative rewards customers for their engagement across various banking activities, fostering a sense of value and encouraging continued patronage. By offering personalized incentives and a broad network of partner benefits, Mokafaa aims to deepen customer loyalty and drive repeat business.

The Mokafaa program is designed to be a key differentiator for Al Rajhi Bank, directly impacting customer retention. For instance, in 2024, the program continued to see significant uptake, with millions of active members earning points on everyday transactions. This strategic focus on rewarding loyalty not only enhances customer satisfaction but also provides a measurable return on investment through increased transaction volumes and reduced churn.

- Mokafaa Program Growth: Al Rajhi Bank's Mokafaa loyalty program saw a substantial increase in member participation throughout 2024, reflecting its effectiveness in driving customer engagement.

- Partner Network Expansion: The program's value proposition is amplified by an expanding network of partners, offering members diverse redemption opportunities and enhancing the perceived benefits of banking with Al Rajhi.

- Customer Retention Impact: Loyalty programs like Mokafaa are crucial for Al Rajhi Bank in fostering long-term customer relationships and encouraging repeat business, directly contributing to market share stability.

Community Engagement and Social Initiatives

Al Rajhi Bank actively cultivates customer relationships by deeply embedding itself within the community. This is achieved through robust social responsibility programs, showcasing a genuine commitment to societal well-being.

A prime example is their support for educational orphan care programs. These initiatives not only provide essential resources but also foster a sense of trust and build a positive public image for the bank.

- Community Programs: Al Rajhi Bank's dedication to social impact is evident in its ongoing community engagement.

- Orphan Care Support: The bank directly contributes to educational orphan care programs, demonstrating a commitment to nurturing future generations.

- Trust and Perception: These social initiatives are instrumental in building strong customer loyalty and enhancing the bank's reputation.

Customer-Centric Digital Banking Fuels Growth and Loyalty

Al Rajhi Bank prioritizes personalized digital experiences, using data to tailor services and offers, which led to a significant increase in digital transactions in 2024. Dedicated relationship managers are assigned to key client segments, fostering trust and customized solutions, contributing to a growing retail customer base in 2024.

The bank offers multi-channel support, with over 70% of inquiries handled digitally in 2024, demonstrating efficient and accessible customer service. Its Mokafaa loyalty program, with millions of active members in 2024, rewards engagement and drives repeat business, enhancing customer retention.

| Customer Relationship Aspect | Key Initiatives | 2024 Impact/Data |

|---|---|---|

| Personalized Digital Engagement | Data-driven recommendations, proactive solutions | Significant increase in digital transaction volumes |

| Dedicated Relationship Management | Tailored advice for corporate, SME, HNW clients | Growth in retail customer base |

| Multi-Channel Customer Support | Call centers, online chat, social media | Over 70% of inquiries handled via digital channels |

| Loyalty Program (Mokafaa) | Rewards for engagement, partner benefits | Millions of active members, increased member participation |

| Community Engagement | Social responsibility programs, orphan care support | Enhanced trust and positive public perception |

Channels

Physical Branch Network

Al Rajhi Bank maintains a substantial physical branch network across Saudi Arabia, acting as vital hubs for customer engagement and service delivery. These branches facilitate everything from account openings to more intricate financial transactions, underscoring their importance for customers seeking personal interaction.

As of early 2024, Al Rajhi Bank boasted over 250 branches within Saudi Arabia, a testament to its commitment to a strong physical presence. This extensive network ensures broad accessibility for its customer base, catering to diverse banking needs through face-to-face service.

Automated Teller Machines (ATMs)

Al Rajhi Bank's extensive ATM network, featuring thousands of machines across Saudi Arabia, serves as a critical customer channel. These ATMs provide 24/7 access to essential banking services like cash withdrawals and deposits, significantly enhancing customer convenience and accessibility beyond traditional branch hours.

In 2024, Al Rajhi Bank continued to leverage its ATM infrastructure to facilitate a wide range of self-service transactions, including bill payments and fund transfers. This widespread deployment allows the bank to efficiently serve a large customer base, extending its operational reach and reinforcing its commitment to digital convenience.

Digital Banking Platforms (Mobile App & Online Banking)

Al Rajhi Bank's digital banking platforms, including the MY alrajhi mobile app and online banking portal, are the core of its customer interaction and service delivery. These platforms provide 24/7 access to a wide array of banking functions such as account management, fund transfers, and bill payments, significantly enhancing customer convenience and accessibility.

In 2024, Al Rajhi Bank continued to see robust adoption of its digital channels. For instance, as of the first quarter of 2024, over 90% of the bank's retail transactions were conducted through digital channels, underscoring the critical role these platforms play in the bank's operational efficiency and customer engagement strategy.

Point-of-Sale (POS) Terminals

Al Rajhi Bank deploys a substantial network of Point-of-Sale (POS) terminals to merchants, acting as a crucial conduit for electronic payments. This extensive reach underpins the bank's strategy to foster a cashless economy and deepen its integration within the retail sector.

These POS terminals are instrumental in enabling seamless transactions for a wide array of goods and services, thereby enhancing customer convenience and merchant efficiency. By facilitating digital payments, Al Rajhi Bank not only supports the growth of its merchant base but also contributes to the broader digital transformation of commerce in Saudi Arabia.

- Merchant Reach: Al Rajhi Bank actively expands its POS terminal network, aiming to onboard a significant percentage of the Kingdom's retail businesses.

- Transaction Volume: In 2024, POS terminals facilitated billions of transactions, showcasing their pivotal role in daily commerce.

- Digital Adoption: The increasing deployment of POS terminals directly correlates with a rise in cashless transactions, reflecting a growing consumer preference for digital payment methods.

Remittance Centers

Al Rajhi Bank's business model includes dedicated remittance centers, a crucial channel for expatriate communities to send money internationally. These specialized locations cater directly to the high demand for efficient and accessible cross-border transactions. In 2023, the global remittance market was valued at approximately $831 billion, highlighting the significant economic activity these centers facilitate.

These remittance centers offer a focused service, ensuring that the specific needs of customers sending money abroad are met with expertise. This specialization helps build trust and loyalty within the expatriate segment. For instance, in Saudi Arabia, remittances by expatriates are a substantial part of the economy, with outflows reaching tens of billions of dollars annually, underscoring the importance of such dedicated channels.

- Specialized Service: Dedicated centers provide focused expertise for international money transfers.

- Expatriate Focus: These centers are vital for expatriate communities needing to send funds home.

- Market Significance: The global remittance market's substantial size, exceeding $800 billion in 2023, validates this business segment.

- Economic Contribution: Facilitating remittances supports economies in both sending and receiving countries.

Comprehensive Banking Channels: Reaching Customers Everywhere

Al Rajhi Bank utilizes a multi-channel approach to reach its customers, encompassing both physical and digital touchpoints. This strategy ensures broad accessibility and caters to diverse customer preferences for banking interactions.

The bank's extensive branch network and ATM infrastructure provide essential in-person and self-service options, while its robust digital platforms, including the MY alrajhi mobile app, handle the majority of retail transactions, demonstrating a strong shift towards digital engagement.

Furthermore, Al Rajhi Bank's widespread POS terminal network facilitates seamless electronic payments, supporting a cashless economy and enhancing merchant services. Dedicated remittance centers also serve a significant expatriate customer base, highlighting specialized channel offerings.

| Channel | Description | 2024 Data/Focus |

|---|---|---|

| Physical Branches | In-person service and complex transactions | Over 250 branches across Saudi Arabia |

| ATMs | 24/7 self-service banking | Thousands of machines nationwide, supporting bill payments and transfers |

| Digital Platforms (App/Online) | Account management, transfers, payments | Over 90% of retail transactions conducted digitally (Q1 2024) |

| POS Terminals | Electronic payment facilitation for merchants | Billions of transactions processed in 2024, driving cashless adoption |

| Remittance Centers | Specialized international money transfers | Catering to expatriate communities, supporting significant remittance flows |

Customer Segments

Individual Retail Customers

Al Rajhi Bank's individual retail customers form a vast and diverse group, encompassing a wide range of demographics. These individuals rely on the bank for essential personal banking needs, including savings and current accounts, personal financing, mortgages, and credit cards.

As of early 2024, Al Rajhi Bank proudly serves a rapidly expanding customer base exceeding 18.5 million individuals. This significant number underscores the bank's broad reach and its ability to cater to the financial requirements of a substantial portion of the population.

Small and Medium Enterprises (SMEs)

Al Rajhi Bank strategically targets Small and Medium Enterprises (SMEs) by offering a suite of specialized financial solutions designed to foster their growth and operational efficiency. These offerings include vital business financing options, flexible working capital solutions to manage day-to-day operations, and comprehensive trade finance services to facilitate international commerce.

Recognizing the pivotal role SMEs play in driving economic development, Al Rajhi Bank is demonstrably committed to expanding its presence within this segment. For instance, in 2023, the Saudi Central Bank reported that SME financing grew by 14% year-on-year, highlighting the increasing demand for such services and Al Rajhi Bank's proactive engagement in meeting it.

Large Corporations and Institutions

Large corporations and institutions represent a core customer segment for Al Rajhi Bank, encompassing major businesses, government bodies, and institutional investors. These clients typically require sophisticated financial solutions, including corporate financing for expansion and operations, comprehensive investment banking services for mergers and acquisitions or capital raising, and advanced treasury solutions for managing liquidity and risk.

Al Rajhi Bank's ambition to be a leading corporate bank means it actively caters to the complex needs of this segment. For instance, in 2023, Saudi Arabia's Vision 2030 continued to drive significant corporate activity, with large projects requiring substantial financing. Al Rajhi Bank's engagement in this space is demonstrated by its participation in syndicated loans and its provision of trade finance solutions to major industrial and commercial enterprises.

Sharia-Conscious Customers

Sharia-conscious customers represent a core segment for Al Rajhi Bank, deeply valuing financial products and services that strictly adhere to Islamic Sharia principles. This segment actively seeks ethical and compliant solutions, aligning with the bank's foundational identity as a leading Islamic financial institution.

Al Rajhi Bank's commitment to Sharia compliance is a primary draw for these customers. For instance, in 2023, the bank reported a significant portion of its customer base actively engaging with its Sharia-compliant offerings, reflecting a strong market demand for such products.

- Islamic Finance Focus: Customers prioritize investments and banking that avoid interest (riba) and engage in ethical business practices.

- Ethical Investment Demand: There's a growing preference for Sharia-compliant funds and wealth management services.

- Trust and Compliance: Adherence to Sharia principles builds significant trust, encouraging long-term relationships.

International Customers and Expatriates

Al Rajhi Bank extends its services to international customers and expatriates, leveraging its presence in key markets such as Jordan, Kuwait, and Malaysia. This strategic footprint, combined with robust remittance services, caters to individuals needing seamless cross-border financial transactions and money transfers.

The bank facilitates international banking needs for a diverse clientele, including expatriates working in Saudi Arabia and individuals with global financial interests. These customers often require specialized services for managing funds, making payments, and transferring money across borders efficiently and securely.

For instance, Al Rajhi Bank’s remittance services are crucial for expatriates sending money back to their home countries. In 2023, the total value of remittances from Saudi Arabia was estimated to be around SAR 150 billion, highlighting the significant demand for such services. Al Rajhi Bank aims to capture a substantial portion of this market by offering competitive rates and user-friendly platforms.

- Global Reach: Operations in Jordan, Kuwait, and Malaysia enable Al Rajhi Bank to serve a wider international customer base.

- Remittance Focus: Specialized services for money transfers cater to expatriates and individuals with international financial obligations.

- Market Demand: The significant volume of remittances from Saudi Arabia underscores the importance of these services for the bank's international customer segment.

Comprehensive Banking: Serving a Diverse Client Spectrum

Al Rajhi Bank serves a broad spectrum of customer segments, from individual retail clients needing everyday banking to large corporations requiring complex financial solutions. The bank also places significant emphasis on catering to Small and Medium Enterprises (SMEs) and individuals who specifically seek Sharia-compliant financial products.

Furthermore, Al Rajhi Bank actively engages with international customers and expatriates, recognizing the importance of facilitating cross-border transactions and remittances. This diverse customer base highlights the bank's comprehensive approach to financial services, aiming to meet varied needs across different demographic and business profiles.

| Customer Segment | Key Needs | 2023/2024 Data Points |

|---|---|---|

| Retail Customers | Savings, loans, mortgages, credit cards | Over 18.5 million individuals served (early 2024) |

| SMEs | Business financing, working capital, trade finance | 14% year-on-year growth in SME financing (2023) |

| Large Corporations & Institutions | Corporate finance, investment banking, treasury solutions | Active participation in syndicated loans and trade finance for major enterprises |

| Sharia-Conscious Customers | Islamic finance, ethical investments, wealth management | Strong engagement with Sharia-compliant offerings |

| International & Expatriates | Remittances, cross-border transactions | Facilitating remittances amidst an estimated SAR 150 billion market (2023) |

Cost Structure

Operating Expenses (Salaries and Benefits)

Al Rajhi Bank's operating expenses, particularly salaries and benefits, represent a substantial part of its cost structure. This reflects the significant human capital needed to manage its widespread branch network and deliver a broad range of financial services to its customers. The bank invested heavily in its workforce, with employee-related costs seeing an increase in 2024.

In 2023, Al Rajhi Bank reported employee expenses of SAR 7,041 million. This figure underscores the considerable expenditure dedicated to attracting, retaining, and developing its staff, which is crucial for maintaining its market leadership and service quality.

Technology and Digital Infrastructure Costs

Al Rajhi Bank dedicates significant resources to its technology and digital infrastructure. These investments are crucial for its ongoing digital transformation, encompassing the development, maintenance, and upgrades of its IT systems and digital platforms. For instance, in 2023, the bank continued to heavily invest in enhancing its digital capabilities and cybersecurity measures to ensure a seamless and secure customer experience.

Branch and ATM Network Maintenance

Al Rajhi Bank incurs significant costs in maintaining its extensive physical footprint. This includes expenses for rent on its numerous branches, electricity and water for these locations, security personnel and systems, and ongoing repairs to ensure functionality and customer safety.

In 2024, the cost of maintaining such a large network is a critical component of the bank's operational expenditure. While specific figures for branch and ATM network maintenance are often embedded within broader operating expense categories, the sheer scale of Al Rajhi Bank's presence across Saudi Arabia necessitates substantial investment in this area to ensure seamless customer access and service delivery.

Marketing and Brand Building Expenses

Al Rajhi Bank dedicates significant resources to marketing and brand building to solidify its market position. These expenditures cover a range of activities, from digital advertising to broader brand awareness campaigns. The bank's commitment to this area is evident in its substantial investment in outreach and engagement initiatives.

In 2024, Al Rajhi Bank implemented several major marketing campaigns designed to resonate with its diverse customer base. These efforts are crucial for maintaining and growing its brand equity in a competitive financial landscape. The bank aims to connect with customers on multiple levels, reinforcing its reputation for service and innovation.

- Digital Marketing: Significant investment in online advertising, social media engagement, and content marketing.

- Brand Campaigns: Large-scale advertising initiatives across various media platforms to enhance brand visibility and recall.

- Sponsorships and Events: Participation in community events and sponsorships to foster brand association and goodwill.

- Customer Relationship Management: Marketing efforts are integrated with CRM strategies to personalize communication and build loyalty.

Regulatory Compliance and Risk Management Costs

Al Rajhi Bank incurs significant costs to maintain strict adherence to banking regulations and robust risk management practices. This includes expenses associated with Sharia compliance, ensuring all operations align with Islamic financial principles, and implementing comprehensive risk mitigation frameworks. These are essential for maintaining trust and operational integrity.

A key component of this cost structure involves provisions for expected credit losses. For instance, in 2024, Al Rajhi Bank's provisions for credit losses saw an increase, reflecting a proactive approach to potential economic headwinds and a commitment to financial stability. This proactive provisioning is a critical element in managing the bank's overall financial health.

- Regulatory Compliance: Costs associated with meeting national and international banking regulations.

- Sharia Compliance: Expenses for ensuring adherence to Islamic Sharia principles in all financial dealings.

- Risk Management: Investments in systems and personnel for identifying, assessing, and mitigating financial and operational risks.

- Credit Loss Provisions: Funds set aside to cover potential losses from loans and advances, with an observed increase in 2024.

Bank's 2023 Costs: Focus on Workforce, Digital, and Risk Management

Al Rajhi Bank's cost structure is heavily influenced by its substantial investment in human capital, with employee expenses forming a significant portion. In 2023, these costs amounted to SAR 7,041 million, reflecting the bank's commitment to its large workforce. The bank also allocates considerable resources to its extensive physical branch network and advanced digital infrastructure, crucial for maintaining its market presence and delivering innovative services.

Maintaining regulatory compliance and robust risk management practices, including Sharia compliance and provisions for credit losses, are also key cost drivers. The bank's proactive approach to potential economic challenges in 2024 led to an increase in its provisions for credit losses, underscoring its focus on financial stability.

| Cost Category | 2023 (SAR Million) | Key Activities |

|---|---|---|

| Employee Expenses | 7,041 | Salaries, benefits, training, and development for a large workforce. |

| Technology & Digital Infrastructure | Not specified separately, but significant investment ongoing | Development, maintenance, and upgrades of IT systems and digital platforms, cybersecurity. |

| Branch Network Operations | Not specified separately, but substantial | Rent, utilities, security, maintenance for extensive branch and ATM network. |

| Marketing & Brand Building | Not specified separately, but significant | Digital marketing, brand campaigns, sponsorships, and CRM initiatives. |

| Compliance & Risk Management | Not specified separately, but integral | Sharia compliance, regulatory adherence, risk mitigation frameworks, credit loss provisions. |

Revenue Streams

Net Financing and Investment Income

Net financing and investment income is Al Rajhi Bank's main engine for making money. It comes from the spread between what they earn on loans and investments and what they pay out for customer deposits. This crucial income stream experienced robust growth in 2024, reflecting strong market demand and effective asset-liability management.

In 2024, Al Rajhi Bank reported a notable increase in its net financing and investment income. This growth was driven by a combination of expanding financing portfolios and a favorable interest rate environment. For example, the bank's net special commission income, a key component of this revenue stream, reached SAR 21.3 billion in the first nine months of 2024, up from SAR 17.5 billion in the same period of 2023, showcasing a significant year-on-year improvement.

Fees from Banking Services

Al Rajhi Bank generates revenue through a diverse array of banking service fees. This includes income from account maintenance, transaction processing, credit and debit card issuance, and foreign exchange operations.

In 2024, the bank saw significant growth in its non-yield income, which is largely comprised of these various fees. This segment expanded substantially, contributing positively to the bank's overall financial performance.

Corporate and SME Financing Income

Al Rajhi Bank generates substantial revenue from its corporate and SME financing activities. This income stems from providing a range of financing solutions, including large syndicated loans and customized business financing packages, to both major corporations and small to medium-sized enterprises.

In 2024, this crucial segment of Al Rajhi Bank's operations experienced robust growth. For instance, Saudi Arabia's banking sector, which Al Rajhi Bank is a major player in, saw a notable increase in corporate lending throughout the year, reflecting a healthy demand for business expansion capital.

Investment Banking and Sukuk Issuance

Al Rajhi Bank generates revenue through its investment banking division, which offers advisory services for mergers, acquisitions, and capital raising. A significant portion of this revenue comes from the issuance of Sukuk, Sharia-compliant bonds. The bank has been particularly active in this space, facilitating numerous Sukuk issuances throughout 2024 and projecting continued activity into 2025, catering to both corporate and governmental clients seeking Sharia-compliant financing solutions.

The bank's involvement in Sukuk issuance is a key revenue driver, reflecting its expertise in Islamic finance. For instance, in 2024, Al Rajhi Bank played a pivotal role in several large-scale Sukuk programs, contributing substantially to its fee and commission income. This strategic focus on Sukuk issuance positions Al Rajhi Bank as a leader in the Islamic capital markets, attracting a broad client base.

- Advisory Services: Revenue from advising on corporate finance transactions, including M&A and capital structuring.

- Sukuk Issuance Fees: Income earned from underwriting and managing the issuance of Sharia-compliant Sukuk.

- Capital Markets Facilitation: Fees generated from assisting clients in accessing capital markets through various Sharia-compliant instruments.

- Underwriting and Distribution: Revenue from the bank's role in purchasing and reselling Sukuk to investors.

Digital Payment Services

Al Rajhi Bank's digital payment services are a significant revenue generator. As the bank broadens its reach in this area, income flows from transaction fees, merchant services, and a suite of other digital payment solutions. This growth is bolstered by the ongoing shift towards cashless transactions within Saudi Arabia.

The bank's commitment to digital transformation is evident in its expanding digital payment offerings. This focus is particularly relevant given the Kingdom's Vision 2030, which aims to increase non-cash transactions. In 2023, for instance, the total value of digital payments in Saudi Arabia saw substantial growth, indicating a strong market for these services.

- Transaction Fees: Al Rajhi Bank earns revenue from fees charged on various digital transactions processed through its platforms.

- Merchant Services: Income is derived from providing digital payment processing solutions to businesses, enabling them to accept a wider range of payments.

- Digital Payment Solutions: This encompasses revenue from innovative products and services designed to facilitate seamless digital transactions for both consumers and businesses.

Bank's Diverse Revenue: Financing, Fees, and Digital Growth

Al Rajhi Bank's revenue streams are diverse, with net financing and investment income forming the primary source. This is supplemented by fees from a wide range of banking services and robust income from corporate and SME financing. The bank also leverages its expertise in Islamic finance through its investment banking division, particularly in Sukuk issuance, and is capitalizing on the growing digital payment landscape.

| Revenue Stream | Description | 2024 Highlight |

|---|---|---|

| Net Financing & Investment Income | Spread on loans, investments, and deposits. | SAR 21.3 billion net special commission income (9M 2024). |

| Banking Service Fees | Account maintenance, transactions, cards, FX. | Significant growth in non-yield income. |

| Corporate & SME Financing | Loans and financing solutions for businesses. | Reflects strong demand in Saudi banking sector. |

| Investment Banking (Sukuk) | Advisory, Sukuk issuance, capital markets. | Pivotal role in large-scale Sukuk programs. |

| Digital Payment Services | Transaction fees, merchant services, digital solutions. | Bolstered by cashless transaction trend in KSA. |

Business Model Canvas Data Sources

Al Rajhi Bank's Business Model Canvas is informed by a blend of internal financial reports, customer transaction data, and extensive market research. This multifaceted approach ensures each component of the canvas accurately reflects the bank's operational realities and strategic objectives.