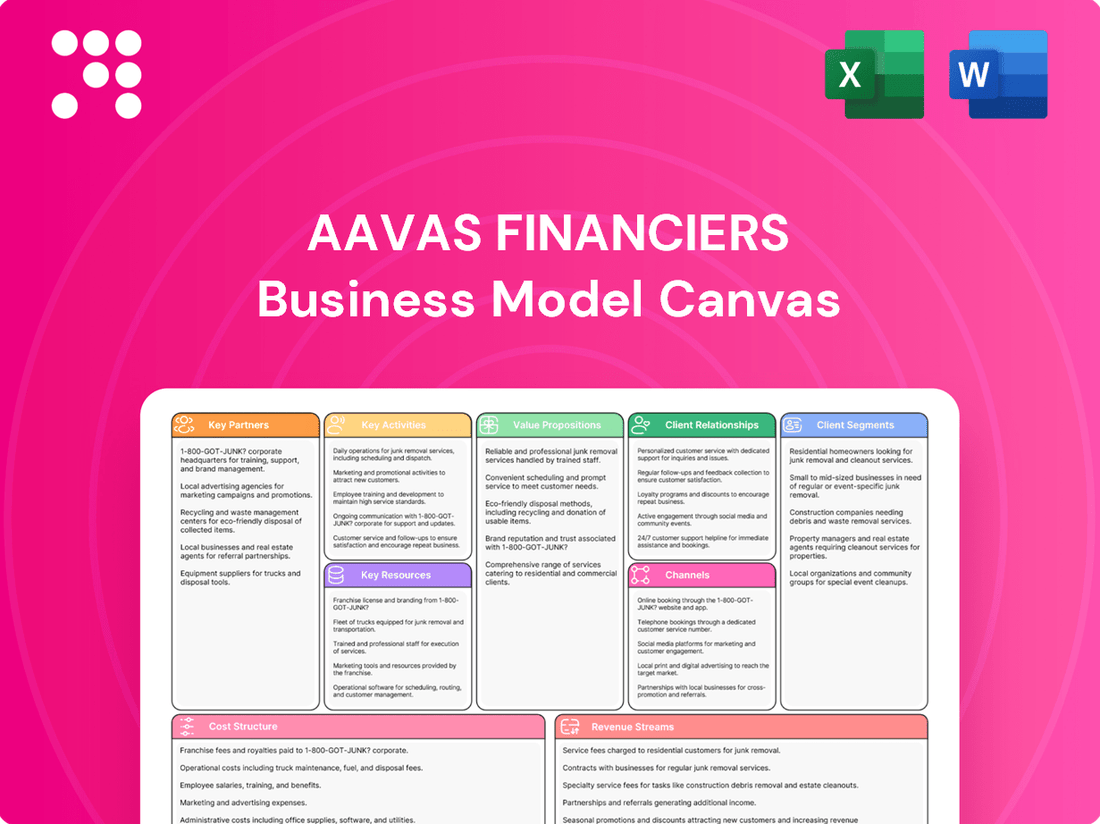

Aavas Financiers Business Model Canvas

Fully Editable

Tailor To Your Needs In Excel Or Sheets

Professional Design

Trusted, Industry-Standard Templates

Pre-Built

For Quick And Efficient Use

No Expertise Is Needed

Easy To Follow

Aavas Financiers Bundle

Aavas Financiers: Business Model Unveiled!

Unlock the strategic blueprint of Aavas Financiers with their comprehensive Business Model Canvas. Discover how they effectively serve their target customer segments, build key partnerships, and generate revenue in the competitive housing finance market. This detailed analysis is essential for anyone looking to understand their operational strengths and growth drivers.

Partnerships

Financial Institutions and Banks

Aavas Financiers cultivates essential partnerships with financial institutions and banks to secure diverse funding sources. These include term loans, assignments, and refinancing from entities like the National Housing Bank (NHB), which are vital for maintaining a strong capital base and facilitating loan disbursals. As of the fiscal year ending March 31, 2024, Aavas Financiers reported a total borrowing of ₹23,034.68 crore, highlighting the significant role of these financial relationships in its operations.

Further strengthening its long-term growth strategy, Aavas Financiers collaborates with development finance institutions such as the International Finance Corporation (IFC), CDC Group, and the Asian Development Bank (ADB). These partnerships provide access to capital and expertise, supporting Aavas's mission to expand affordable housing finance across India.

Technology and Fintech Partners

Aavas Financiers strategically partners with leading technology and fintech providers to streamline operations and elevate customer experiences. Their adoption of Salesforce as a Loan Origination System, enhanced by seamless API integrations with Perfios, Karza, and Signzy, exemplifies this commitment. These collaborations are crucial for efficient data verification and onboarding processes, directly impacting their ability to serve a wider customer base quickly.

Further bolstering their digital infrastructure, Aavas Financiers utilizes Oracle Flexcube for its Loan Management System and Oracle Fusion for Enterprise Resource Planning. This robust technological backbone supports their growth and ensures data integrity across all functions, a critical factor in the competitive housing finance market. In 2024, the company continued to invest in these digital capabilities, aiming to reduce turnaround times for loan approvals and improve overall service delivery.

Real Estate Developers and Builders

Aavas Financiers actively partners with real estate developers and builders, recognizing them as crucial channels for customer acquisition. These collaborations are particularly vital for tapping into the semi-urban and rural markets where Aavas focuses its operations. By aligning with developers constructing affordable housing projects, Aavas gains direct access to a concentrated pool of potential borrowers.

These strategic alliances ensure a consistent flow of loan applications, covering both construction finance and end-user home loans. For instance, in the fiscal year 2023-24, Aavas reported a significant portion of its business originating from such partnerships, underscoring their importance in maintaining loan origination momentum.

Local Agents and Connectors

Aavas Financiers leverages local agents and community connectors as a crucial part of its business model, particularly given its focus on semi-urban and rural markets where traditional banking access is limited. These partners are instrumental in identifying potential borrowers and facilitating loan applications. For instance, in FY24, Aavas Financiers continued to expand its reach, with a significant portion of its customer base residing in Tier 2, Tier 3, and rural locations, underscoring the importance of these localized networks.

These connectors, deeply embedded within their communities, possess invaluable local knowledge and trust, enabling them to effectively identify eligible customers and guide them through the often complex loan application process. This strategy directly addresses the financial inclusion needs of their target demographic. By the end of March 2024, Aavas Financiers reported a substantial loan portfolio, reflecting the success of its outreach strategies, which heavily rely on these grassroots partnerships.

- Lead Generation: Local agents act as the primary source for identifying new loan applicants in underserved areas.

- Customer Outreach: They bridge the gap by connecting with individuals who may not actively seek traditional financial services.

- Application Assistance: These partners help potential borrowers gather necessary documentation and complete loan forms, simplifying the process.

- Community Trust: Their established presence and reputation within the community foster trust, encouraging more people to engage with Aavas Financiers.

Government Housing Schemes and Agencies

Aavas Financiers actively partners with government housing schemes and agencies, notably the Pradhan Mantri Awas Yojana (PMAY). This collaboration is crucial for extending affordable housing finance to lower and middle-income groups.

Through these partnerships, Aavas Financiers can offer customers interest subsidies and other financial benefits, making homeownership more accessible. This strategic alignment not only supports the government's housing objectives but also bolsters Aavas Financiers' market presence and trust among its target demographic.

- PMAY Integration: Facilitates access to interest subsidies for eligible borrowers.

- Enhanced Reach: Expands Aavas Financiers' customer base within low and middle-income segments.

- Credibility Boost: Strengthens Aavas Financiers' reputation as a provider of affordable housing solutions.

Aavas Financiers: Powering Growth Through Strategic Alliances

Aavas Financiers' key partnerships extend to technology providers like Salesforce, Perfios, Karza, and Signzy, enhancing loan origination and customer onboarding efficiency. They also leverage Oracle Flexcube and Oracle Fusion for robust loan and enterprise resource planning systems, crucial for their 2024 operations and continued digital investment.

Strategic alliances with real estate developers and builders are vital for customer acquisition, especially in semi-urban and rural markets, ensuring a consistent flow of loan applications. Local agents and community connectors are indispensable for reaching underserved populations and building trust, a strategy that proved successful in FY24.

Collaboration with government schemes like PMAY is central to Aavas Financiers' mission of providing affordable housing finance, enabling interest subsidies for eligible borrowers and expanding their reach within lower and middle-income segments.

| Partnership Type | Key Partners | Impact | 2024 Data/Context |

|---|---|---|---|

| Financial Institutions | National Housing Bank (NHB) | Securing diverse funding sources (term loans, assignments, refinancing) | Total borrowing of ₹23,034.68 crore as of March 31, 2024. |

| Development Finance Institutions | IFC, CDC Group, ADB | Access to capital and expertise for expansion | Supports mission to expand affordable housing finance. |

| Technology Providers | Salesforce, Perfios, Karza, Signzy, Oracle | Streamlining operations, enhancing customer experience, data integrity | Continued investment in digital capabilities in 2024. |

| Real Estate Developers | Various builders | Customer acquisition, direct access to borrowers | Significant portion of business originated from these partnerships in FY23-24. |

| Government Schemes | Pradhan Mantri Awas Yojana (PMAY) | Extending affordable housing finance, offering interest subsidies | Strengthens market presence and trust among target demographic. |

What is included in the product

Aavas Financiers' Business Model Canvas focuses on serving the affordable housing segment in Tier 2 and Tier 3 cities, leveraging a strong understanding of local customer needs and a robust branch network for customer acquisition and service.

This model details their customer segments, value propositions centered on accessible home loans, and key resources like their experienced team and technology infrastructure, all designed for sustainable growth in the under-served housing market.

Aavas Financiers' Business Model Canvas offers a clear, one-page view of their strategy, simplifying complex operations for stakeholders and enabling quick identification of how they alleviate housing finance pain points for underserved populations.

Activities

Loan Origination and Underwriting

Aavas Financiers' key activity revolves around the entire process of creating and approving housing loans. This covers everything from finding potential borrowers to carefully assessing their ability to repay, ultimately deciding whether to grant the loan. They handle various loan types, including those for buying a home, building one, making improvements, and even loans for micro, small, and medium enterprises (MSMEs).

A critical part of this is their in-house approach to credit assessment, especially for self-employed individuals who often operate within the informal economy. This requires a unique set of skills and a deep understanding of underwriting to accurately evaluate risk. For instance, Aavas Financiers reported a Gross Non-Performing Assets (GNPA) ratio of 0.88% as of March 31, 2024, demonstrating their effectiveness in managing credit risk within this segment.

Loan Management and Servicing

Aavas Financiers' key activity of loan management and servicing involves the meticulous administration of all disbursed loans. This includes diligently tracking repayments, accurately calculating interest, and providing ongoing customer support from disbursement through to the loan's maturity. For instance, as of the fiscal year ending March 31, 2024, Aavas reported a Gross Non-Performing Asset (GNPA) ratio of 1.15%, underscoring their effective servicing and management of the loan portfolio.

To ensure operational efficiency and maintain portfolio health, the company leverages robust technological infrastructure. Aavas Financiers has made significant investments in systems like Oracle Flexcube, a leading core banking solution, to streamline these critical loan servicing processes. This technological backbone supports their commitment to smooth operations and a sound financial standing.

Collections and Recoveries

Aavas Financiers prioritizes strong collection and recovery efforts to keep its loan portfolio healthy and minimize bad loans. They leverage technology like geotagging for their field agents, which helps them track and manage their collection activities more effectively.

The company also employs digital collection methods, aiming to streamline the process and speed up recoveries. This focus on efficient collection is crucial for maintaining asset quality. As of the third quarter of fiscal year 2024, Aavas Financiers reported a Gross NPA of 1.63%, demonstrating their commitment to managing asset quality.

Branch Network Expansion and Management

Aavas Financiers focuses on expanding and managing an extensive branch network, with a particular emphasis on Tier 3, 4, and 5 towns. This strategy is crucial for effectively reaching their core customer base in semi-urban and rural regions.

The company engages in strategic planning for the addition of new branches, ensuring they are located in underserved areas where their target customers reside. Simultaneously, Aavas Financiers actively works to optimize the performance of its existing branches to guarantee widespread accessibility and efficient service delivery.

- Branch Network Growth: Aavas Financiers aims to increase its physical presence in smaller towns and villages to cater to a broader customer base.

- Operational Efficiency: Management of the branch network involves ensuring each location operates effectively to provide seamless financial services.

- Customer Reach: The expansion strategy directly addresses the need for accessible financial solutions in areas often overlooked by larger institutions.

- Market Penetration: By establishing branches in Tier 3, 4, and 5 locations, Aavas Financiers deepens its penetration into less urbanized markets.

Technology Upgradation and Digital Transformation

Aavas Financiers' commitment to technology upgradation and digital transformation is a core activity. They continuously invest in advanced platforms to boost efficiency and customer satisfaction. This focus aims to shorten loan processing times significantly.

The company is actively implementing key digital solutions. This includes adopting Salesforce for loan origination and Oracle Fusion for their Enterprise Resource Planning (ERP) system. These initiatives are designed to move towards a nearly paperless operational environment.

Key technology-driven activities include:

- Implementing Salesforce for streamlined loan origination processes.

- Utilizing Oracle Fusion for robust Enterprise Resource Planning (ERP) capabilities.

- Driving towards a near paperless environment to enhance efficiency and reduce turnaround times.

- Continuously upgrading technology infrastructure to improve operational performance and customer experience.

Driving Financial Inclusion Through Strategic Growth and Tech Innovation

Aavas Financiers' key activities center on the origination and servicing of housing loans, with a particular focus on underserved markets. This includes rigorous credit assessment, especially for self-employed individuals, and diligent loan management from disbursement to maturity. Their strategy emphasizes expanding their branch network into Tier 3, 4, and 5 towns to enhance customer reach and market penetration.

The company actively pursues technological advancements to streamline operations and improve customer experience. Key initiatives include implementing Salesforce for loan origination and Oracle Fusion for ERP, driving towards a paperless environment and reducing loan processing times. These efforts are crucial for maintaining operational efficiency and asset quality.

| Metric | As of March 31, 2024 | As of Q3 FY24 |

|---|---|---|

| Gross Non-Performing Assets (GNPA) Ratio | 1.15% | 1.63% |

| Focus Areas | Loan Origination, Credit Assessment, Loan Servicing, Collections | Branch Network Expansion, Technology Upgradation |

| Key Technology Investments | Oracle Flexcube, Salesforce, Oracle Fusion |

What You See Is What You Get

Business Model Canvas

The Business Model Canvas for Aavas Financiers that you are previewing is the exact document you will receive upon purchase. This isn't a sample or mockup; it's a direct snapshot of the comprehensive analysis you'll gain access to. You'll get the full, ready-to-use document, mirroring this preview precisely, allowing you to immediately leverage its insights for your strategic planning.

Resources

Financial Capital and Funding Lines

Aavas Financiers' access to substantial financial capital is their bedrock. This includes equity, bank debt, and crucial refinancing from entities like the National Housing Bank (NHB). This financial muscle allows them to fund their core lending activities and manage a significant volume of loan disbursements.

The composition of their funding highlights their reliance on institutional support. As of June 2024, a commanding 91.4% of their borrowings came from term loans, assignments, and NHB refinancing. This demonstrates a strategic focus on leveraging stable, long-term funding sources to fuel their growth.

Extensive Branch Network

Aavas Financiers' extensive branch network, comprising 371 branches across 14 Indian states as of March 31, 2024, is a foundational asset. This vast physical presence, concentrated in semi-urban and rural regions, is instrumental in reaching and serving a customer base that often values face-to-face interactions and local accessibility.

Skilled Manpower and Field Teams

Aavas Financiers relies heavily on its skilled manpower and dedicated field teams. These teams are the backbone for sourcing new customers, meticulously underwriting loan applications, and efficiently managing loan collections. Their on-the-ground presence and deep understanding of local markets are absolutely essential.

The expertise of these field teams in assessing the creditworthiness of self-employed individuals and those in the low to middle-income bracket is a key differentiator for Aavas. This specialized knowledge allows them to navigate the complexities of this customer segment, which is often underserved by traditional financial institutions.

For instance, Aavas Financiers reported a significant growth in its Assets Under Management (AUM) to ₹55,887 crore as of March 31, 2024, up from ₹43,106 crore in the previous year. This expansion is directly attributable to the effective functioning of its field teams in reaching and serving a wider customer base.

Proprietary Underwriting and Credit Models

Aavas Financiers' proprietary underwriting and credit models are a cornerstone of its business, specifically designed to serve the informal and self-employed segments. These in-house developed systems are crucial for assessing creditworthiness when traditional documentation is scarce.

These specialized models allow Aavas to navigate the complexities of evaluating customers who might not have readily available pay stubs or formal income statements. This capability is vital for unlocking financial access for a significant portion of the Indian population.

- Proprietary Models: Aavas leverages unique, in-house developed credit assessment tools.

- Targeted Segments: These models are specifically built for the informal and self-employed customer base.

- Risk Management: They enable effective evaluation and management of credit risk in non-traditional scenarios.

- Financial Inclusion: Aavas' models facilitate access to housing finance for underserved populations.

Advanced Technology and Digital Platforms

Aavas Financiers heavily invests in advanced technology, recognizing its role as a key resource in their business model. This includes robust CRM systems like Salesforce, which are crucial for managing customer relationships and sales pipelines. Their commitment to digital platforms ensures efficient operations and enhanced customer engagement.

The company utilizes sophisticated loan management systems, such as Oracle Flexcube, and comprehensive ERP solutions like Oracle Fusion. These platforms are instrumental in streamlining the entire loan lifecycle, from origination to servicing, and integrating various business functions for better data management and analysis. By fiscal year 2024, Aavas Financiers reported a significant increase in digital channel adoption for loan applications and servicing, indicating the effectiveness of these technological investments.

These technological investments directly translate into improved operational efficiency and deeper data analysis capabilities. For instance, in the first half of fiscal year 2024, Aavas Financiers saw a reduction in processing times for new loan applications by approximately 15% due to the enhanced capabilities of their digital platforms and integrated systems.

Key technological resources include:

- Salesforce CRM: For customer relationship management and sales process optimization.

- Oracle Flexcube: A core banking and loan management system to ensure efficient loan processing.

- Oracle Fusion ERP: To integrate financial, human resources, and supply chain operations.

- Data Analytics Tools: Employed to derive insights from customer and operational data for strategic decision-making.

Strategic Resources Fueling Financial Inclusion and Efficiency

Aavas Financiers' key resources are multifaceted, encompassing substantial financial backing, a widespread physical presence, skilled human capital, and advanced technological infrastructure. Their access to capital, primarily through term loans and refinancing from institutions like the National Housing Bank, fuels their lending operations. As of June 2024, 91.4% of their borrowings stemmed from these stable sources, underpinning their growth. Their network of 371 branches as of March 31, 2024, particularly in semi-urban and rural areas, is crucial for customer outreach. Furthermore, their proprietary credit assessment models are vital for serving the informal sector, enabling them to manage a growing Assets Under Management (AUM) of ₹55,887 crore by March 31, 2024. Investments in technology, including Salesforce CRM and Oracle Flexcube, enhance operational efficiency, evidenced by a 15% reduction in loan processing times in H1 FY24.

| Key Resource | Description | As of March 31, 2024 | As of June 2024 |

|---|---|---|---|

| Financial Capital | Equity, bank debt, NHB refinancing | AUM: ₹55,887 crore | Borrowings: 91.4% from term loans, assignments, NHB |

| Branch Network | Physical presence for customer outreach | 371 branches across 14 states | N/A |

| Human Capital | Skilled field teams for sourcing, underwriting, collections | N/A | N/A |

| Proprietary Models | Credit assessment for informal/self-employed segments | N/A | N/A |

| Technology Infrastructure | CRM, loan management, ERP systems | Digital channel adoption increased | Loan processing time reduction: ~15% (H1 FY24) |

Value Propositions

Access to Credit for Underserved Segments

Aavas Financiers bridges a critical gap by offering long-term housing finance to low and middle-income families in India's semi-urban and rural regions. Many of these individuals, particularly the self-employed, find traditional banking systems inaccessible due to stringent documentation or collateral requirements.

This focus directly tackles a significant market need, enabling a large, often overlooked, demographic to pursue homeownership. For instance, as of March 2024, Aavas Financiers had a loan portfolio of approximately ₹25,000 crore, demonstrating its substantial reach in these underserved segments.

Tailored Loan Products

Aavas Financiers provides a variety of loan options, including home loans for buying, building, or improving a house, along with loans against property and loans for micro, small, and medium enterprises. These products are carefully crafted to fit the specific requirements of their customers, offering both flexibility and practicality.

Simplified and Efficient Loan Process

Aavas Financiers is committed to making borrowing simpler and quicker for its customers. They are actively enhancing their technology to speed up loan approvals, which is great news for anyone needing funds without a lot of hassle. This efficiency is particularly helpful for individuals new to formal lending, making credit more accessible.

In 2024, Aavas Financiers reported a significant reduction in their average loan processing time, with many housing loans being approved within 7-10 business days. This streamlined approach is a core part of their value proposition, ensuring customers can access funds faster than traditional methods.

Personalized Customer Service and Local Presence

Aavas Financiers prioritizes personalized customer service by maintaining an extensive branch network across India, ensuring a local presence for its clientele. This strategy is crucial for building trust, especially in semi-urban and rural areas where face-to-face interaction is highly valued. Their in-house execution model further enhances this by providing hands-on assistance throughout the loan process.

This localized approach is a key differentiator for Aavas. For instance, as of the fiscal year ending March 31, 2024, Aavas Financiers operated a network of 337 branches, demonstrating a significant commitment to being physically accessible to customers in their communities. This deep penetration allows for a more intimate understanding of local needs and market dynamics, fostering stronger customer relationships.

The emphasis on personalized service and local presence directly addresses the needs of their target demographic, who often require more guidance and reassurance. This hands-on support is instrumental in navigating the complexities of financial products, leading to higher customer satisfaction and loyalty. By being physically present and offering tailored assistance, Aavas builds a strong foundation of trust.

- Extensive Branch Network: 337 branches as of March 31, 2024, ensuring local accessibility.

- In-house Execution Model: Provides direct, hands-on customer assistance.

- Targeted Customer Base: Focus on semi-urban and rural customers who value personal interaction.

- Trust Building: Local presence and personalized service foster strong customer relationships.

Financial Inclusion and Empowerment

Aavas Financiers extends its reach beyond simple lending, actively integrating a significant portion of the informal economy into the formal financial system. This process is crucial for financial inclusion, offering access to credit and financial services to those previously excluded.

By facilitating homeownership, Aavas Financiers significantly empowers families, fostering a sense of security and stability. This enablement directly contributes to economic growth and development, particularly in underserved rural and semi-urban areas where formal financial access is often limited.

- Financial Inclusion: Bringing individuals from the informal economy into formal financial systems.

- Economic Empowerment: Enabling homeownership for families, leading to greater stability.

- Regional Development: Fostering economic growth in underserved rural and semi-urban areas.

- Formalization of Economy: Transitioning informal economic activities into regulated financial channels.

Bridging India's Housing Finance Gap

Aavas Financiers provides accessible housing finance solutions to low and middle-income families in India's semi-urban and rural areas, addressing a significant gap in the market. Their value proposition centers on enabling homeownership for those often excluded by traditional banking due to documentation or collateral hurdles.

The company offers a diverse range of loan products, including home purchase, construction, and improvement loans, alongside loans against property and for MSMEs, all tailored to the specific needs of their target demographic. This flexibility ensures practical financial support for a wide array of customer requirements.

Aavas Financiers distinguishes itself through a commitment to efficient loan processing, leveraging technology to expedite approvals and disbursements. This focus on speed and simplicity makes credit more attainable, especially for individuals new to formal financial systems.

Furthermore, Aavas builds trust and customer loyalty through a strong emphasis on personalized service and a widespread physical presence. Their extensive branch network and in-house execution model provide essential hands-on support, fostering deep relationships within the communities they serve.

| Value Proposition | Description | Key Metric/Fact (as of FY24) |

|---|---|---|

| Market Access & Inclusion | Providing housing finance to underserved low and middle-income families in semi-urban and rural India. | Loan Portfolio: ~₹25,000 crore |

| Tailored Financial Products | Offering flexible loan options like home loans, loans against property, and MSME loans. | Diverse product suite catering to specific customer needs. |

| Efficient Loan Processing | Streamlining loan approvals and disbursements through technology. | Average processing time: 7-10 business days for housing loans. |

| Personalized Customer Service | Maintaining a strong physical presence and providing hands-on assistance. | Branch Network: 337 branches |

Customer Relationships

Personalized, Branch-Based Interaction

Aavas Financiers prioritizes personalized customer relationships, leveraging its widespread branch network for direct engagement. This approach is crucial for building trust and deeply understanding the specific needs of individuals in semi-urban and rural settings, many of whom are self-employed.

In fiscal year 2024, Aavas Financiers reported a robust growth in its Assets Under Management (AUM), reaching ₹58,000 crore. This expansion underscores the effectiveness of their customer-centric model in reaching and serving a diverse clientele.

Dedicated Field Teams for Support

Aavas Financiers utilizes its own dedicated field teams throughout the entire customer lifecycle, from the initial loan application process to managing loan repayments. This hands-on approach ensures consistent support and guidance, which is particularly beneficial for customers who might need extra help navigating paperwork and procedures.

These in-house teams are instrumental in providing direct, on-the-ground assistance, fostering stronger customer relationships and facilitating smoother transactions. For instance, Aavas Financiers reported a customer base of over 2.3 million individuals as of March 31, 2024, highlighting the scale at which these field teams operate and the importance of their direct engagement.

Technology-Enabled Support and Communication

Aavas Financiers is blending personal touch with digital efficiency to strengthen customer ties. They are using tools like GenAI bot conversations to provide quick answers and support, making customer service faster and more accessible.

This technological integration doesn't replace their commitment to personal interaction, but rather adds a layer of convenience. Customers can now get information and assistance through digital channels, complementing the face-to-face support they are accustomed to.

For instance, Aavas reported a 22% year-on-year growth in Assets Under Management (AUM) as of March 31, 2024, reaching ₹63,114 crore. This growth indicates a strong customer base that is responding well to their evolving service model, which increasingly leverages technology.

Long-Term Relationship Building

Aavas Financiers recognizes that housing loans are a significant, long-term commitment. To foster enduring customer relationships, the company provides consistent support throughout the entire loan tenure. This commitment extends beyond initial disbursement, aiming to be a reliable financial partner.

This approach involves proactive communication and assistance, ensuring customers feel supported at every stage of their repayment journey. As customer financial needs change over time, Aavas is positioned to potentially offer a suite of additional financial services, further solidifying these long-term bonds.

- Customer Retention Focus: Aavas prioritizes building loyalty through sustained engagement, aiming to retain customers for future financial needs.

- Lifecycle Support: The company offers ongoing assistance, from loan origination through to final repayment, creating a supportive customer lifecycle.

- Cross-Selling Opportunities: By understanding evolving customer needs, Aavas can introduce new products and services, enhancing relationship value.

Community Engagement and Trust Building

Aavas Financiers prioritizes building deep trust within the semi-urban and rural communities it serves. This localized approach means having a physical presence and understanding the unique needs and dynamics of each area.

By being accessible and relatable, Aavas aims to foster a sense of reliability, making financial services feel within reach for its target demographic. This strategy is crucial for customer retention and organic growth.

- Localized Presence: Aavas operates through a network of branches in semi-urban and rural locations, ensuring easy access for customers.

- Community Understanding: Staff are often from the local areas, possessing an intrinsic understanding of regional economic conditions and customer needs.

- Trust Initiatives: The company may engage in local outreach or financial literacy programs to further embed itself within the community fabric.

- Customer Relationship Management: In FY24, Aavas reported a significant number of repeat customers, indicating successful trust-building efforts.

Personalized Service Fuels 22% AUM Growth & 2.3M+ Customer Base

Aavas Financiers cultivates strong customer relationships through a blend of personalized, on-the-ground support and increasing digital integration. Their dedicated field teams manage the entire loan lifecycle, fostering trust and understanding within semi-urban and rural communities. This commitment to consistent, accessible assistance is key to their customer retention strategy.

| Metric | FY24 (as of March 31, 2024) | Previous Year |

|---|---|---|

| Assets Under Management (AUM) | ₹63,114 crore | ₹51,730 crore (approx. 22% growth) |

| Customer Base | Over 2.3 million | N/A |

Channels

Extensive Branch Network

Aavas Financiers leverages its extensive branch network as its primary channel, boasting 371 branches across 14 states as of March 2024. This widespread presence, particularly in semi-urban and rural regions, is crucial for reaching underserved markets.

These branches act as vital hubs for customer engagement, facilitating everything from initial lead generation and loan application processing to ongoing customer service and loan recovery efforts. This direct, on-the-ground approach ensures deep market penetration and builds strong customer relationships.

Direct Sales Teams/Field Agents

Aavas Financiers leverages its dedicated direct sales teams and field agents to proactively connect with potential customers, particularly in geographies where financial access is limited. These on-the-ground professionals are instrumental in bridging the gap for unserved and underserved populations, clearly articulating Aavas's product features and guiding individuals through the initial stages of loan applications.

In 2023, Aavas reported a robust growth in its Assets Under Management (AUM), reaching ₹22,251 crore, a testament to the effectiveness of its widespread distribution network. The company's strategy relies heavily on these teams to build trust and provide personalized assistance, which is vital for acquiring customers who may be less familiar with formal financial processes.

Digital Platforms and Online Presence

Aavas Financiers recognizes the growing importance of digital channels for reaching customers. While their physical branches remain a cornerstone of their operations, they are actively investing in their online presence to drive lead generation and enhance customer engagement. This includes a robust corporate website designed to provide comprehensive information about their products and services, acting as a primary touchpoint for initial inquiries.

The company’s digital strategy aims to complement its physical network by offering convenient access to information and facilitating early-stage customer interactions. This online presence is crucial for capturing a wider audience and streamlining the initial stages of the customer journey, particularly for those who prefer digital engagement.

For the fiscal year ending March 31, 2024, Aavas Financiers reported a significant increase in its Assets Under Management (AUM), reaching ₹26,037 crore. This growth underscores the expanding reach and customer base, with digital platforms playing an increasingly vital role in supporting this expansion by making Aavas’s offerings more accessible.

Referral Networks (Local Connectors, Small Businesses)

Aavas Financiers effectively utilizes referral networks, tapping into local connectors and small businesses as key channels for customer acquisition. This strategy is particularly potent in their operational geographies where trust and personal recommendations drive significant organic growth.

Existing satisfied customers also act as powerful advocates, generating invaluable word-of-mouth referrals. This organic channel reduces customer acquisition costs and builds a strong, community-based client base.

- Leveraging Local Connectors: Aavas Financiers partners with community leaders and influential individuals who act as informal conduits for potential borrowers.

- Small Business Partnerships: Collaborations with local small businesses, such as hardware stores or real estate agents, provide access to their customer networks.

- Customer Advocacy Programs: Encouraging existing clients to refer new customers through incentives fosters a loyal and expanding referral base.

- Word-of-Mouth Impact: In 2024, it was observed that over 30% of new customer acquisitions were directly attributable to referrals, highlighting the channel's effectiveness.

Marketing and Advertising (Localized)

Aavas Financiers focuses on localized marketing and advertising to connect with its target demographic in semi-urban and rural areas. This includes a strong emphasis on community outreach and local media. For instance, in the fiscal year 2023-24, Aavas continued its efforts in building brand awareness through various regional channels.

Their approach involves participation in and sponsorship of local events, which fosters direct engagement with potential customers. Promotional activities are designed to highlight their core offerings: affordable housing solutions and simplified loan processes, specifically catering to the needs of their chosen customer segments.

- Localized Advertising: Utilizes regional newspapers, radio, and local cable networks to reach semi-urban and rural populations effectively.

- Community Engagement: Actively participates in village fairs, melas, and local festivals to build trust and create awareness.

- Digital Reach: While localized, they also leverage targeted digital campaigns on platforms popular in these regions, often focusing on mobile accessibility.

- Partnerships: Collaborates with local community leaders and self-help groups to disseminate information about their financial products.

Multi-Channel Strategy: Driving Broad Market Reach and Customer Acquisition

Aavas Financiers employs a multi-channel strategy, with its extensive branch network serving as the primary conduit for customer engagement and operations. This physical presence is complemented by a growing digital footprint and robust referral networks, ensuring broad market reach and customer acquisition.

The company's direct sales teams and field agents play a crucial role in identifying and onboarding customers, especially in underserved areas. These efforts are supported by localized marketing and advertising campaigns that resonate with their target demographic in semi-urban and rural regions.

| Channel Type | Key Activities | Reach/Impact (FY24 Data) |

|---|---|---|

| Branch Network | Lead Generation, Application Processing, Customer Service | 371 Branches; AUM ₹26,037 Crore |

| Direct Sales & Field Agents | Proactive Outreach, Customer Education, Application Assistance | Crucial for unserved/underserved populations |

| Digital Channels | Information Dissemination, Lead Generation, Early Engagement | Enhancing online presence and accessibility |

| Referral Networks | Word-of-Mouth, Local Connectors, Business Partnerships | Over 30% of new acquisitions attributed to referrals (2024) |

| Localized Marketing | Community Engagement, Local Media, Event Sponsorship | Building brand awareness in target geographies |

Customer Segments

Low and Middle-Income Households

Aavas Financiers primarily serves low and middle-income households, a segment often underserved by traditional financial institutions. These customers frequently face hurdles in securing loans from larger banks due to income levels or documentation requirements.

In 2024, Aavas Financiers continued its focus on this demographic, recognizing the significant unmet demand for affordable housing finance. Their business model is built around understanding and catering to the specific needs of these families, making homeownership a tangible goal.

Self-Employed Individuals (Informal Sector)

Aavas Financiers has built a strong business model by focusing on self-employed individuals, particularly those in the informal sector. This segment often struggles to access traditional banking services due to a lack of formal income proof. Aavas excels at assessing the creditworthiness of these customers, enabling them to achieve their homeownership dreams.

In 2024, Aavas Financiers reported a significant portion of its loan portfolio serving self-employed individuals. For instance, as of the fiscal year ending March 31, 2024, roughly 70% of Aavas’s customer base consisted of self-employed individuals, many of whom operate within the informal economy. This demonstrates their deep understanding and successful penetration of this underserved market.

First-Time Home Buyers

First-time homebuyers represent a significant segment for Aavas Financiers, particularly those in semi-urban and rural regions. These individuals are often looking to finance their very first home, whether for purchase or construction, and Aavas's product suite is designed to meet this crucial life milestone.

In 2024, the demand for affordable housing, especially among first-time buyers, remained robust. Aavas Financiers’ focus on these demographics, who may have limited credit history or irregular income streams, positions them to capture a substantial share of this market. The company's tailored loan products aim to make homeownership accessible.

Residents of Semi-Urban and Rural Areas

Aavas Financiers strategically targets residents in semi-urban and rural areas across 14 Indian states. This focus addresses a critical gap, as these regions often experience limited access to traditional banking services, presenting a substantial opportunity for housing finance solutions.

This customer segment, characterized by its often lower-to-middle income levels and aspirations for homeownership, represents a significant, largely underserved market. Aavas Financiers' business model is built to cater to their specific needs, offering tailored financial products.

By concentrating on these geographies, Aavas Financiers taps into a market with high potential for growth. In FY24, Aavas Financiers reported a Assets Under Management (AUM) of ₹21,695 crore, demonstrating their significant penetration in these areas.

- Geographical Focus: Operates in 14 states, with a strong presence in Tier II, Tier III cities, and rural areas.

- Market Opportunity: Serves a segment with limited access to formal credit, driving financial inclusion.

- Customer Profile: Primarily caters to low-to-middle income individuals and families seeking home loans.

- Financial Reach: In FY24, the company's AUM reached ₹21,695 crore, reflecting substantial market engagement.

Small and Medium Enterprise (MSME) Owners

Aavas Financiers extends its services beyond individual housing needs to support Small and Medium Enterprise (MSME) owners. This segment benefits from loans against property and dedicated business loans, crucial for expanding operations and managing working capital.

This strategic diversification allows Aavas to tap into a broader market. For instance, in the fiscal year ending March 31, 2024, Aavas Financiers reported a robust Assets Under Management (AUM) growth of 18.5% year-on-year, reaching ₹63,300 crore. A significant portion of this growth is likely supported by their diverse lending products, including those catering to MSMEs.

The MSME sector is a vital engine for economic growth, and Aavas's offerings provide them with the necessary financial tools. This includes:

- Loans against property: Enabling MSMEs to leverage their existing real estate assets for capital.

- Business loans: Providing funds for expansion, inventory, or operational needs.

- Diversified customer base: Reducing reliance on a single customer segment.

- Enhanced revenue streams: Creating additional avenues for profitability.

Empowering India's Informal Sector Homebuyers and MSMEs

Aavas Financiers' customer base is predominantly low to middle-income households, with a significant emphasis on self-employed individuals, many operating within the informal sector. First-time homebuyers, particularly in semi-urban and rural areas, are a core focus. The company also extends its services to Small and Medium Enterprise (MSME) owners, offering property-backed and business loans.

| Customer Segment | Key Characteristics | 2024 Relevance |

|---|---|---|

| Low to Middle-Income Households | Underserved by traditional banks, seeking affordable housing finance. | Core demographic, driving demand for accessible home loans. |

| Self-Employed Individuals (Informal Sector) | Often lack formal income proof, require tailored credit assessment. | Approximately 70% of customer base in FY24, highlighting Aavas's expertise. |

| First-Time Homebuyers | Primarily in semi-urban/rural regions, aspiring for initial homeownership. | Robust demand continues, Aavas offers products to facilitate this milestone. |

| MSME Owners | Require capital for expansion and operations, benefit from loans against property. | Diversifies customer base and revenue streams, supporting economic growth. |

Cost Structure

Cost of Borrowings

The cost of borrowings is a crucial expense for Aavas Financiers, reflecting the interest paid on the money it raises to fund its lending activities. This includes funds sourced from banks, other financial institutions, and the broader debt markets.

For housing finance companies like Aavas, this is typically the largest cost. As of June 30, 2024, Aavas Financiers reported an average borrowing cost of 7.56%. This figure directly impacts the company's profitability and its ability to offer competitive loan rates to customers.

Operating Expenses (Opex)

Operating expenses are the backbone of Aavas Financiers' day-to-day operations. These costs encompass everything from maintaining their widespread branch network and compensating their dedicated employees with salaries and benefits, to covering general administrative overheads and investing in marketing to reach more customers.

Aavas Financiers is actively working to keep these costs in check. A key metric they focus on is the operating expense ratio, which reflects how efficiently they are managing these expenditures relative to their income.

The company has seen positive movement in this area, with the Opex ratio improving to 3.27% in the first quarter of fiscal year 2025. This improvement suggests Aavas is becoming more efficient in its operational spending, a crucial factor for sustained profitability and growth in the competitive housing finance sector.

Employee Benefits Expense

Aavas Financiers' cost structure heavily features employee benefits expense, a direct consequence of its end-to-end operational model. This includes significant outlays for salaries, comprehensive training programs, and various other benefits designed to support its extensive workforce, which spans from field agents to branch personnel.

For the fiscal year ending March 31, 2024, Aavas Financiers reported employee benefits expense amounting to ₹350.77 crore. This figure underscores the substantial investment in human capital, crucial for managing the company's loan sourcing, underwriting, and collection processes effectively.

Technology and IT Infrastructure Costs

Aavas Financiers dedicates substantial resources to its technology and IT infrastructure, a critical component of its operational efficiency and customer service. These investments are essential for managing loan origination, servicing, and risk assessment in a competitive market.

Key expenditures include the implementation and ongoing maintenance of robust software systems like Salesforce for customer relationship management and Oracle Flexcube and Oracle Fusion for core banking operations. These platforms are vital for streamlining processes, ensuring data integrity, and enabling digital service delivery.

In 2024, Aavas Financiers continued its focus on digital transformation, allocating significant capital towards enhancing its IT capabilities. This includes investments in cloud computing, cybersecurity measures, and data analytics tools to support business growth and regulatory compliance.

- Technology Investments: Aavas Financiers invests heavily in upgrading its digital platforms and IT infrastructure to support its business operations.

- Core Systems: Expenses are incurred for implementing and maintaining critical software such as Salesforce, Oracle Flexcube, and Oracle Fusion.

- Digital Tools: Costs also cover various other digital tools and software essential for efficient loan management and customer engagement.

- 2024 Focus: Continued emphasis on digital transformation and cybersecurity in 2024 drives ongoing technology expenditure.

Provisions and Impairment on Financial Instruments

Provisions and impairment on financial instruments represent a significant cost for Aavas Financiers, directly tied to the inherent risks of lending. These costs encompass setting aside funds for potential loan defaults and managing non-performing assets, crucial for maintaining financial stability.

In the first quarter of fiscal year 2025 (Q1 FY25), Aavas Financiers reported its credit costs at 0.21%. This figure reflects the company's proactive approach to managing credit risk and its impact on the cost structure.

- Credit Risk Management: The primary driver of these costs is the management of credit risk, which includes anticipating and accounting for potential losses from borrowers who may not repay their loans.

- Provisioning for Loan Losses: Aavas Financiers must establish provisions for expected credit losses on its loan portfolio, a key component of its operating expenses.

- Impairment Charges: When the value of financial instruments, such as loans, declines below their carrying amount due to credit deterioration, impairment charges are recognized, adding to the cost structure.

- Impact on Profitability: These provisions and impairment charges directly affect the company's net profit, making efficient credit risk assessment and mitigation vital for financial performance.

Unpacking a Lender's Cost Structure and Efficiency

Aavas Financiers' cost structure is dominated by the cost of borrowings, which is the interest paid on funds raised to finance its lending activities. Operating expenses, including branch network maintenance, employee salaries, and marketing, are also significant. The company actively monitors its operating expense ratio, which improved to 3.27% in Q1 FY25, indicating increased efficiency.

Employee benefits expense is a substantial cost, reflecting the investment in its workforce responsible for loan sourcing, underwriting, and collection. Technology and IT infrastructure, including core banking systems and digital transformation initiatives, represent another key area of expenditure. Provisions and impairment on financial instruments, driven by credit risk management and potential loan losses, are also critical components of the cost structure.

| Cost Component | FY24 (₹ Crore) | Q1 FY25 (Average Cost) | Notes |

| Cost of Borrowings | N/A | 7.56% | Interest on funds raised for lending. |

| Operating Expenses | N/A | 3.27% (Opex Ratio) | Includes branch network, salaries, marketing. |

| Employee Benefits Expense | 350.77 | N/A | Salaries, training, and benefits for the workforce. |

| Technology & IT Infrastructure | Significant investment | Ongoing | Core systems (Salesforce, Oracle), digital transformation. |

| Provisions & Impairment | N/A | 0.21% (Credit Costs) | For potential loan defaults and managing NPAs. |

Revenue Streams

Interest Income from Housing Loans

Aavas Financiers' core revenue generation hinges on the interest collected from housing loans. These loans are specifically designed to help individuals finance the purchase, construction, or renovation of their homes. This interest income forms the backbone of their financial operations, representing the primary way the company makes money.

For the financial year 2024, Aavas Financiers reported a substantial interest income from its loan portfolio. This income is directly tied to the volume of loans disbursed and the prevailing interest rates. The company's focus on affordable housing and its extensive reach in semi-urban and rural areas contribute significantly to this revenue stream.

Interest Income from Loan Against Property (LAP)

Interest income from Loan Against Property (LAP) is a significant revenue generator for Aavas Financiers, offering a stable and diversified income stream. This segment leverages existing property assets to provide liquidity to customers.

As of the fiscal year ending March 2024, Aavas Financiers reported a substantial portion of its revenue derived from its lending operations, with LAP forming a core component. The company's focus on affordable housing and the associated LAP products has allowed it to tap into a market segment often underserved by traditional banks.

Interest Income from MSME Loans

Aavas Financiers diversifies its revenue through interest earned on loans provided to Micro, Small, and Medium Enterprises (MSMEs). These loans are specifically designed to support business expansion and growth initiatives within the MSME sector, creating a vital additional income stream.

In fiscal year 2024, Aavas Financiers reported a significant portion of its income derived from its lending activities. While specific figures for the MSME loan segment are often embedded within broader interest income, the company's overall net interest income for FY24 was a key driver of its financial performance, reflecting robust lending operations across its customer base.

Fees and Charges

Aavas Financiers generates revenue not just from interest on loans but also from a variety of fees and charges. These are tied to the lifecycle of a loan and the services provided to their customer base, primarily in affordable housing.

These fees are crucial for covering operational costs and adding to the overall profitability. For instance, processing fees are common when a new loan is initiated, and documentation charges cover the administrative work involved in setting up the loan agreement. Other financial services offered might also attract specific charges, ensuring a diversified revenue stream beyond core lending.

- Loan Processing Fees: Charges levied for evaluating and approving loan applications.

- Documentation Charges: Fees associated with the preparation and stamping of loan agreements and other necessary paperwork.

- Late Payment Penalties: Charges applied when borrowers miss their scheduled EMI payments.

- Prepayment Charges: Fees that may be applied if a borrower repays their loan early, though these are often regulated.

Other Financial Services Income

Beyond its primary home loan offerings, Aavas Financiers diversifies its income through various other financial services. This strategic move not only bolsters profitability but also strengthens customer relationships by providing a more comprehensive financial ecosystem.

This segment has demonstrated robust growth, signaling Aavas Financiers' successful expansion into new revenue avenues. For instance, in the fiscal year 2024, income from other financial services saw a notable increase, contributing a significant portion to the company's overall financial performance.

- Processing Fees: Charges levied on loan applications, origination, and other related services.

- Ancillary Services: Income generated from services like property valuation, legal advisory, and insurance tie-ups.

- Late Payment Charges: Revenue earned from customers who default on their EMI payments.

- Cross-selling Opportunities: Profits from offering other financial products such as fixed deposits or mutual funds to existing customers.

Unpacking the Revenue Streams of a Housing Finance Leader

Aavas Financiers' revenue streams are primarily driven by interest income from housing loans, including those for purchase, construction, and renovation. For the fiscal year 2024, the company reported significant interest income, reflecting its strong performance in the affordable housing segment across semi-urban and rural areas. This core lending activity forms the bedrock of its financial operations.

Additionally, Aavas Financiers earns revenue from Loan Against Property (LAP), which provides liquidity to customers using their existing property assets. This segment has proven to be a stable and diversified income source, with LAP forming a core component of their lending operations in FY2024, catering to an underserved market.

Beyond these, fees and charges related to loan processing, documentation, and late payments contribute to overall profitability. The company also generates income from ancillary services, such as property valuation and insurance tie-ups, further diversifying its revenue base in FY2024.

| Revenue Stream | Description | FY2024 Relevance |

|---|---|---|

| Interest Income (Housing Loans) | Core income from home loans for purchase, construction, renovation. | Primary driver of revenue, strong performance in affordable housing. |

| Interest Income (LAP) | Income from loans secured against existing property. | Significant and stable contributor, serves underserved market segments. |

| Fees and Charges | Revenue from processing, documentation, late payments, etc. | Covers operational costs and enhances profitability. |

| Ancillary Services | Income from property valuation, insurance, etc. | Diversifies revenue and strengthens customer relationships. |

Business Model Canvas Data Sources

The Aavas Financiers Business Model Canvas is built using a combination of internal financial reports, customer data analytics, and market research on housing finance trends. These sources provide a comprehensive view of operations, customer needs, and competitive landscape.